Concept explainers

Videos

MacGyver Corporation manufactures a product called Miracle Goo, which comes in handy for just about anything. The thick tarry substance is sold in six-gallon drums. Two raw materials are used; these are referred to by people in the business as A and B. Two types of labor are required also. These are mixers (labor class I) and packers (labor class II). You were recently hired by the company president, Pete Thorn, to be the controller. You soon learned that MacGyver uses a standard-costing system. Variances are computed and closed into Cost of Goods Sold monthly. After your first month on the job, you gathered the necessary data to compute the month’s variances for direct material and direct labor. You finished everything up by 5:00 p.m. on the 31st, including the credit to Cost of Goods Sold for the sum of the variances. You decided to take all your notes home to review them prior to your formal presentation to Thorn first thing in the morning. As an afterthought, you grabbed a drum of Miracle Goo as well, thinking it could prove useful in some unanticipated way.

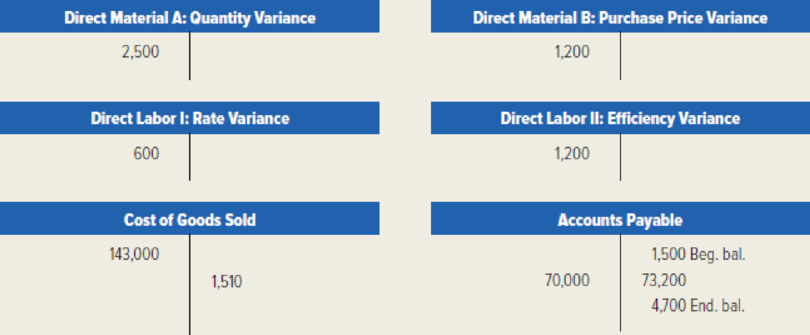

You spent the evening boning up on the data for your report and were ready to call it a night. As luck would have it though, you knocked over the Miracle Goo as you rose from the kitchen table. The stuff splattered everywhere, and, most unfortunately, obliterated most of your notes. All that remained legible is the following information.

Other assorted data gleaned from your notes:

- The standards for each drum of Miracle Goo include 10 pounds of material A at a standard price of $5 per pound.

- The standard cost of material B is $15 for each drum of Miracle Goo.

- Purchases of material A were 12,000 pounds at $4.50 per pound.

- Given the actual output for the month, the standard allowed quantity of material A was 10,000 pounds. The standard allowed quantity of material B was 5,000 gallons.

- Although 6,000 gallons of B were purchased, only 4,800 gallons were used.

- The standard wage rate for mixers is $15 per hour. The standard labor cost per drum of product for mixers is $30 per drum.

- The standards allow 4 hours of direct labor II (packers) per drum of Miracle Goo. The standard labor cost per drum of product for packers is $48 per drum.

- Packers were paid $11.90 per hour during the month.

You happened to remember two additional facts. There were no beginning or ending inventories of either work in process or finished goods for the month. The increase in accounts payable relates to direct-material purchases only.

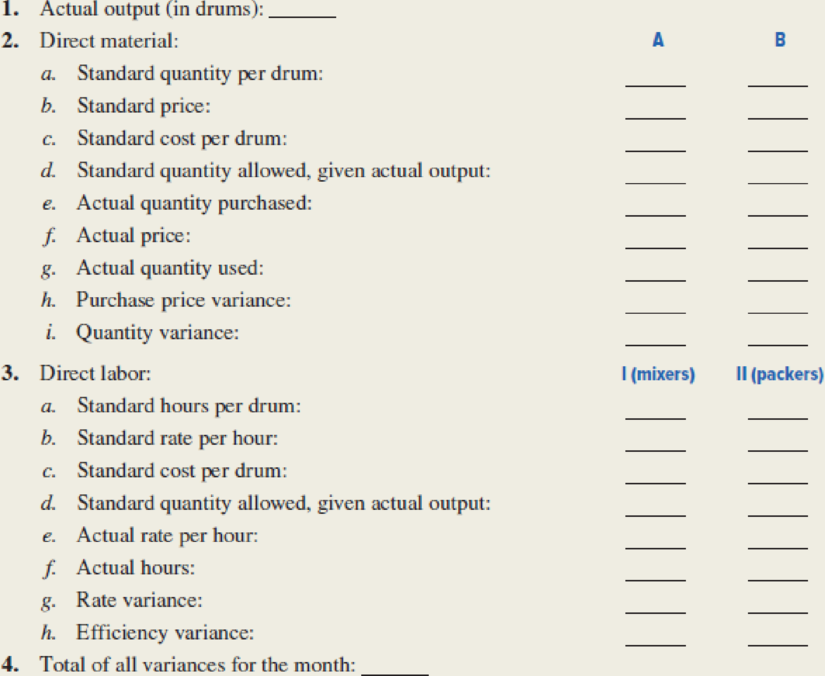

Required: Now you’ve got a major problem. Somehow you’ve got to reconstruct all the missing data in order to be ready for your meeting with the president. You start by making the following list of the facts you want to use in your presentation. Before getting down to business, you need a brief walk to clear your head. Out to the trash you go, and toss the remaining Miracle Goo.

Fill in the missing amounts in the list, using the available facts.

Calculate the missing amount of Company M.

Explanation of Solution

Variance: Variance refers to the difference level in the actual cost incurred and standard cost. The total cost variance is subdivided into separate cost variances; this cost variance indicates that the amount of variance that is attributable to specific casual factors.

Calculate the missing amount of Company M as follows:

| Particulars | Amount in $ | |

| 1. Actual output (in drums) (1) | 1,000 drums | |

| 2. Direct materials: | A | B |

| a. Standard quantity per drum (2) | 10 lb | 5 gal |

| b. Standard price (3) | $5.00/lb | $3.00/gal. |

| c. Standard cost per drum (4) | $ 50.00 | $ 15.00 |

| d. Standard quantity allowed, given actual output (5) | 10,000 lb | 5,000 gal |

| e. Actual quantity purchased (6) | 12,000 lb | 6,000 gal |

| f. Actual price (7) | $4.50/lb | $3.20/gal. |

| g. Actual quantity used (8) | 10,500 lb | 4,800 gal |

| h. Purchase price variance(9) | $6,000 F | $1,200 U |

| i. Quantity variance (10) | $2,500 U | $600 F |

| 3. Direct labor: |

I (mixers) | II (packers) |

| a. Standard hours per drum (11) | 2 hr. | 4 hr. |

| b. standard rate per hour (12) | $ 15.00 | $ 12.00 |

| c. Standard cost per drum (13) | $ 30.00 | $ 48.00 |

| d. Standard quantity allowed, given actual output (14) | 2,000 hr. | 4,000 hr. |

| e. Actual rate per hour (15) | $ 15.30 | $ 11.90 |

| f. Actual hours(16) | 2,000 hr. | 4,100 hr. |

| g. Rate variance (17) | $600 U | $410 F |

| h. Efficiency variance (18) | 0 | $1,200 U |

| 4. Total of all variance for the month (19) | $1,510 F | |

Table (1)

Working note (1):

Calculate (1) the actual output of Company M.

Working note (2):

Calculate the (2. a.) standard quantity of direct material per drum:

Material A:

The standard quantity of direct material per drum of material A is 10 lb. (given).

Material B:

Note: 10,000 pound = 10lb.

Working note (3):

Calculate the (2. b.) the standard price of direct material:

Material A:

The standard price of direct material A is $5.00/lb. (given).

Material B:

Working note (4):

Calculate the (2. c.) the standard cost per drum:

Material A:

Material B:

Standard cost of direct material B is $15 (given).

Working note (5):

Calculate the (2. d.) the standard quantity allowed for actual output:

The standard quantity allowed for actual output of Material A is 10,000 lb. (given).

The standard quantity allowed for actual output of Material B is 5,000 gal. (given).

Working note (6):

Calculate the (2. e.) the actual quantity purchased:

The actual quantity purchased for Material A is 12,000 lb. (given).

The actual quantity purchased for Material B is 6,000 gal (given).

Working note (7):

Calculate the (2. f.) the actual price of direct material:

Material A:

The actual price of direct material A is $4.50/lb. (given).

Material B:

Working note (8):

Calculate the (2. g.) the actual quantity used during the month:

Material A:

Material B:

The actual quantity of material B used during the month is 4,800 gal (given).

Working note (9):

Calculate the (2. h.) the price variance for direct material:

Material A:

Material B:

The price variance of material B is $1,200 Unfavorable (given).

Working note (10):

Calculate the (2. i.) the quantity variance for direct material:

Material A:

The quantity variance of direct material A is $2,500 Unfavorable (given).

Material B:

Note: Debit side of variance account indicates the unfavorable variance, and credit side of variance account indicates the favorable variance.

Working note (11):

Calculate the (3. a.) the standard direct labor hours per drum:

Mixers:

Packers:

The standard direct labor hour per drum is 4 hours (given).

Working note (12):

Calculate the (3. b.) the standard rate per hour:

Mixers:

The standard rate per hour for mixers is $15.00 (given).

Packers:

Working note (13):

Calculate the (3. c.) the standard cost per drum:

The standard cost per drum for Mixers (type-I labor) is $30.00 (given).

The standard cost per drum for Packers (type-II labor) is $48.00 (given).

Working note (14):

Calculate the (3. d.) the standard quantity allowed for actual output:

Mixers:

Packers:

Working note (15):

Calculate the (3. e.) the actual rate per hour:

Mixers:

Packers:

The actual rate per hour for packers (type-II labor) is $11.90 (given).

Working note (16):

Calculate the (3. f.) the actual direct labor hours:

Mixers:

In this case, there is no efficiency variance for type I labors. Hence standard hours are equal to actual hours. Therefore, the actual direct labor hours for type I labors is 2,000 hours (given).

Packers:

Working note (17):

Calculate the (3. g.) the direct labor rate variance:

Mixers:

The direct labor rate variance for type-I labor is $600 Unfavorable (given).

Packers:

Working note (18):

Calculate the (3. h.) the direct labor efficiency variance:

The direct labor efficiency variance of mixtures (type-I labor) is $0 (given).

The direct labor efficiency variance of packers (type-II labor) is $1,200 Unfavorable (given).

Working note (19):

Calculate the (4) the total of all variances for the month:

| Particulars | Amount in $ |

| Direct-material variances: | |

| Price variance of material A (9) | 6,000 F |

| Quantity variance of material A (10) | -2,500 U |

| Price variance of material B (9) | -1,200 U |

| Quantity variance of material B (10) | 600 F |

| Direct-labor variances: | |

| Rate variance of type I labor (17) | -600 U |

| Efficiency variance of type I labor (18) | 0 |

| Rate variance of type II labor (17) | 410 F |

| Efficiency variance of type II labor (18) | -1,200 U |

| Total of all variances | 1,510 F |

Table (2)

Want to see more full solutions like this?

Chapter 10 Solutions

Managerial Accounting: Creating Value in a Dynamic Business Environment

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education