Videos

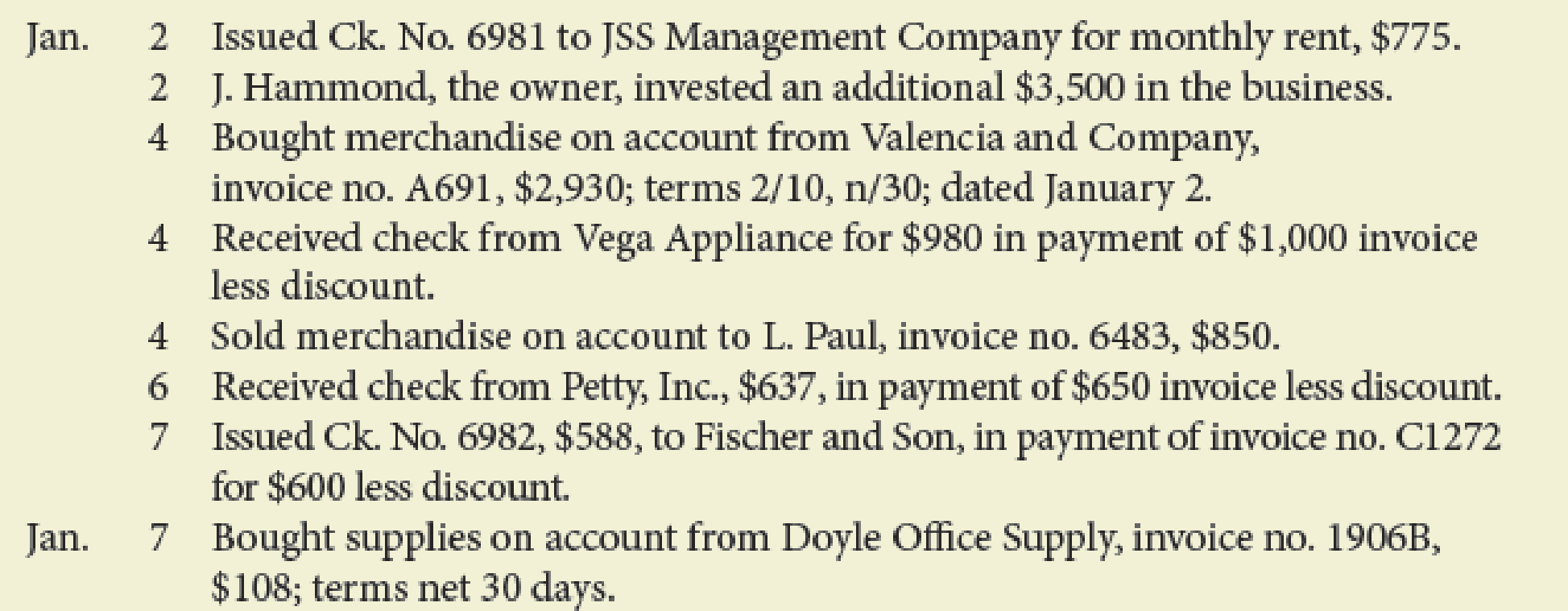

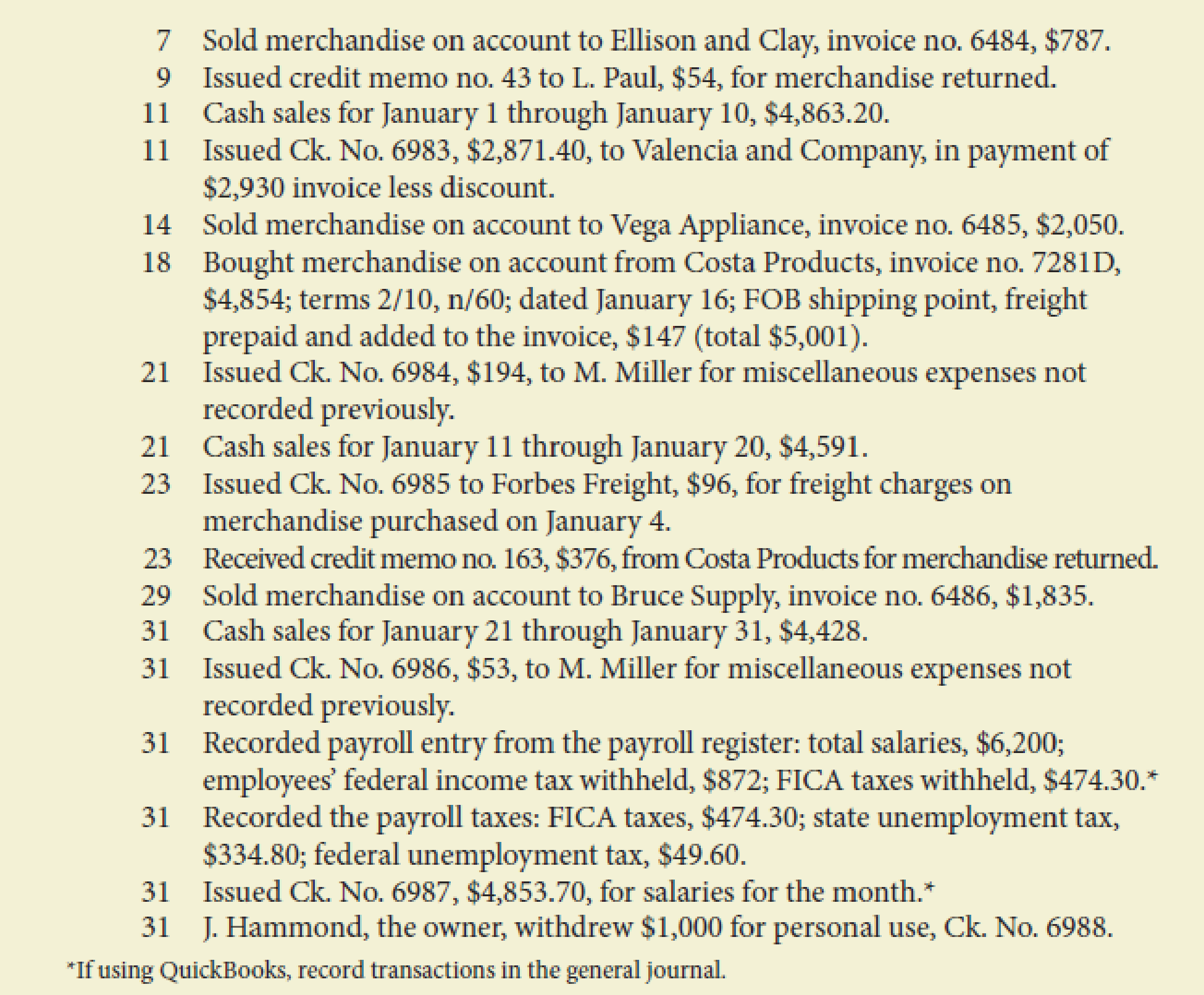

The following transactions were completed by Hammond Auto Supply during January, which is the first month of this fiscal year. Terms of sale are 2/10, n/30. The balances of the accounts as of January 1 have been recorded in the general ledger in your Working Papers or in CengageNow. Hammond Auto Supply does not track cash sales by customer. If you are using the form-based approach with QuickBooks or general ledger, select “Cash Sales” as the customer for all cash sales transactions.

Required

- 1. Record the transactions for January using a general journal, page 1. Assume the periodic inventory method is used.*

* If using QuickBooks, record transactions using either the

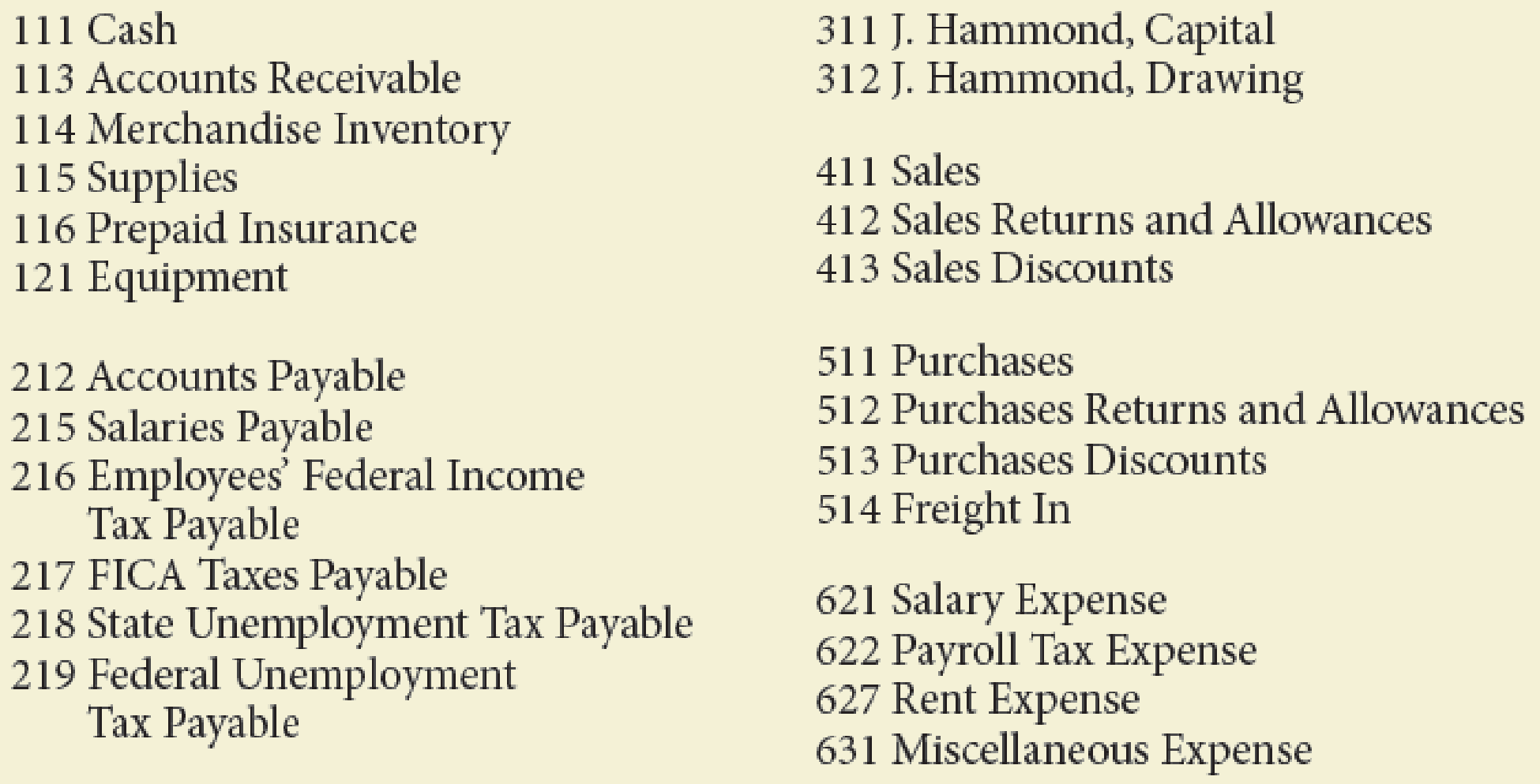

The chart of accounts is as follows:

- 2.

Post daily all entries involving customer accounts to theaccounts receivable ledger.* - 3. Post daily all entries involving creditor accounts to the accounts payable ledger.*

- 4. Post daily the general journal entries to the general ledger. Write the owner’s name in the Capital and Drawing accounts.*

*If using QuickBooks or general ledger, ignore Steps 2, 3, and 4.

- 5. Prepare a

trial balance . - 6. Prepare a schedule of accounts receivable (A/R Aging Detail report in QuickBooks) and a schedule of accounts payable (A/P Summary Detail report in QuickBooks). Do the totals equal the balances of the related controlling accounts?

1.

Journalize the transactions in the general journal using the periodic inventory method.

Explanation of Solution

General journal is a record of financial transaction. The transactions are recorded in the journal prior to posting them to the accounts in the general ledger.

Periodic inventory system: The method or system of recording the transactions related to inventory occasionally or periodically are referred to as periodic inventory system.

Journalize the transactions in the general journal.

| GENERAL JOURNAL PAGES 1 | ||||||||||

| Date | Description | Post Ref. | Debit ($) | Credit ($) | ||||||

| 20-- | ||||||||||

| Jan | 2 | Rent Expense | 627 | 775 | ||||||

| Cash | 111 | 775 | ||||||||

| (Record the paid month rent, Ck.No.6981) | ||||||||||

| 2 | Cash | 111 | 3,500 | |||||||

| Mr. H, Capital | 311 | 3,500 | ||||||||

| (Record the additional capital invested by the owner) | ||||||||||

| 4 | Purchases | 511 | 2,930 | |||||||

| Accounts Payable, V Company | 212/ | 2,930 | ||||||||

| (Purchased merchandise from V Company, invoice no.A691,invoice dated January 2,terms 2/10, n/30) | ||||||||||

| 4 | Cash | 111 | 980 | |||||||

| Sales Discount | 413 | 20 | ||||||||

| Accounts Receivable | 113/ | 1,000 | ||||||||

| (Payment of invoice less discount) | ||||||||||

| 4 | Accounts Receivable Mr. P | 113/ | 850 | |||||||

| Sales | 411 | 850 | ||||||||

| (Record the sale of merchandise to Mr. P, invoice no.6483) | ||||||||||

| 6 | Cash | 111 | 637 | |||||||

| Sales Discount | 413 | 13 | ||||||||

| Accounts Receivable, Petty, Inc. | 113/ | 650 | ||||||||

| (Record the payment of invoice less discount) | ||||||||||

| 7 | Accounts Payable, F Company | 212/ | 600 | |||||||

| Purchase Discount | 513 | 12 | ||||||||

| Cash | 111 | 588 | ||||||||

| (Record the paid invoice no.C1272, Ck.No.6982) | ||||||||||

| 7 | Supplies | 625 | 108 | |||||||

| Accounts Payable, D Company | 212/ | 108 | ||||||||

| (Record the office supply, Invoice no. 1906B,term net 30) | ||||||||||

| GENERAL JOURNAL PAGES 2 | ||||||

| 7 | Accounts Receivable, Mr. E & C | 113/ | 787 | |||

| sales | 411 | 787 | ||||

| (Record the sale of merchandise to Mr. E & C invoice no.6484) | ||||||

| 9 | Sales Return and Allowance | 412 | 54 | |||

| Accounts Receivable, Mr. P | 113/ | 54 | ||||

| (Record the issued credit memo no.43) | ||||||

| 11 | Cash | 111 | 4,863.20 | |||

| Sales | 411 | 4,863.20 | ||||

| (Record the cash sales, January 1-10) | ||||||

| 11 | Accounts Payable, V Company | 212/ | 2,930 | |||

| Cash | 111 | 2,871.40 | ||||

| Purchase Discount | 513 | 58.6 | ||||

| (Record the invoice paid n.A691 less discount, Ck. No. 6983) | ||||||

| 14 | Accounts Receivable, V Company | 113/ | 2,050 | |||

| Sales | 411 | 2,050 | ||||

| (Record the sale of merchandise to V Company, invoice no. 6485) | ||||||

| 18 | Purchases | 511 | 4,854 | |||

| Freight In | 514 | 147 | ||||

| Accounts Payable, Mr. C | 212/ | 5,001 | ||||

| (Record the purchase of merchandise from C Company, invoice dated January 16) | ||||||

| 21 | Miscellaneous Expense | 631 | 194 | |||

| Cash | 111 | 194 | ||||

| (Record the cash paid to Mr. M,Ck.No.6985) | ||||||

| 21 | Cash | 111 | 4,591 | |||

| Sales | 411 | 4,591 | ||||

| (Record the cash sales, January 11-20) | ||||||

| 23 | Freight In | 514 | 96 | |||

| Cash | 111 | 96 | ||||

| (Record the freight charge, Ck. No. 6985) | ||||||

| GENERAL JOURNAL PAGE 3 | ||||||

| 23 | Accounts Payable, C Company | 212/ | 376 | |||

| Purchase Return and Allowance | 512 | 376 | ||||

| (Record return on merchandise credit memo.163) | ||||||

| 29 | Accounts Receivable, B Company | 113/ | 1,835 | |||

| Sales | 411 | 1,835 | ||||

| (Record the sale of merchandise to B Company invoice no.6486) | ||||||

| 31 | Cash | 111 | 4,428 | |||

| Sales | 411 | 4,428 | ||||

| (Record cash sales on january21-31) | ||||||

| 31 | Miscellaneous Expenses | 631 | 53 | |||

| Cash | 111 | 53 | ||||

| (Paid to Mr. M CK.NO.6986) | ||||||

| 31 | Salary Expenses | 621 | 6,200 | |||

| Employees' Federal Income Tax Payable | 216 | 872 | ||||

| FICA Tax Payable | 217 | 474.30 | ||||

| Salaries Payable | 215 | 4,853.70 | ||||

| (Record the salaries for the month) | ||||||

| 31 | Payroll Tax Expense | 622 | 846.3 | |||

| FICA Tax Payable | 217 | 474.30 | ||||

| State Unemployment Tax Payable | 218 | 334.8 | ||||

| Federal Unemployment Tax Payable | 219 | 49.60 | ||||

| (Record the employer’s share of FICA taxes and employer's state and federal unemployment taxes for the month) | ||||||

| 31 | Salaries Payable | 215 | 4,853.70 | |||

| Cash | 111 | 4,853.70 | ||||

| (Record the payroll, Ck.No.6987) | ||||||

| 31 | Mr. H, Drawing | 312 | 1,000 | |||

| Cash | 111 | 1,000 | ||||

| (Record the withdrawal for personal use,Ck.No.6988) | ||||||

Table (1)

2.

Record the entries from customer accounts to the accounts receivable ledger.

Explanation of Solution

Account receivable: The amount of money to be received by a company for the sale of goods and services to the customers is referred to as account receivable.

T-account: The condensed form of a ledger is referred to as T-account. The left-hand side of this account is known as debit, and the right hand side is known as credit.

Entries from customer accounts to the accounts receivable ledger:

| Accounts receivable ledger | ||||||

| Name: B company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| Jan | 29 | 3 | 1,835 | 1,835 | ||

| Name: E and C company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| Jan | 7 | 2 | 787 | 787 | ||

| Name: L company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| Jan | 4 | 1 | 850 | 850 | ||

| 9 | 2 | 54 | 796 | |||

| Name: P company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| Jan | 1 | Balance | 650 | |||

| 6 | 1 | 650 | 0 | |||

| Name: V company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| Jan | 1 | Balance | 1,000 | |||

| 4 | 1 | 1,000 | 0 | |||

| 14 | 2 | 2,050 | 2,050 | |||

Table (2)

3.

Record the entries from customer accounts to the accounts payable ledger.

Explanation of Solution

Account payable: The amount of money to be paid by a company for the purchase of goods and services from the seller is referred to as account payable.

Entries from customer accounts to the accounts payable ledger:

| Accounts payable ledger | ||||||

| Name: C company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| Jan | 18 | 2 | 5,001 | 5,001 | ||

| 23 | 3 | 376 | 4,625 | |||

| Name: D company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| Jan | 7 | 1 | 108 | 108 | ||

| Name: F and sons | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| Jan | 1 | Balance | 600 | |||

| 7 | 1 | 600 | 0 | |||

| Name: V company | ||||||

| Address: | ||||||

| Date | Items | Post ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| Jan | 4 | 1 | 2,930 | 2,930 | ||

| 11 | 2 | 2,930 | 0 | |||

Table (3)

4.

Record the journal entries to the general ledger.

Explanation of Solution

General ledger: General ledger is a record of all accounts of assets, liabilities, and stockholders’ equity, necessary to prepare financial statements.

Journal entries to the general ledger:

| Account: Cash | Account No:111 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 1 | Balance | 8,740 | |||||

| 2 | 1 | 775 | 7,965 | |||||

| 2 | 1 | 3,500 | 11,465 | |||||

| 4 | 1 | 980 | 12,445 | |||||

| 6 | 1 | 637 | 13,082 | |||||

| 7 | 1 | 588 | 12,494 | |||||

| 11 | 2 | 4,863.2 | 17,357.2 | |||||

| 11 | 2 | 2,871.4 | 14,485.8 | |||||

| 21 | 2 | 194 | 14,291.8 | |||||

| 21 | 2 | 4,591 | 18,882.8 | |||||

| 23 | 2 | 96 | 18,786.8 | |||||

| 31 | 3 | 4,428 | 23,214.8 | |||||

| 31 | 3 | 53 | 23,161.8 | |||||

| 31 | 3 | 4,853.7 | 18,308 | |||||

| 31 | 3 | 1,000 | 17,308.1 | |||||

| Account: Accounts receivable | Account No:113 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 1 | Balance | 1,650 | |||||

| 4 | 1 | 1,000 | 650 | |||||

| 4 | 1 | 850.00 | 1,500 | |||||

| 6 | 1 | 650.00 | 850 | |||||

| 7 | 2 | 787 | 1,637 | |||||

| 9 | 2 | 54 | 1,583 | |||||

| 14 | 2 | 2,050 | 3,633 | |||||

| 29 | 3 | 1,835 | 5,468 | |||||

| Account: Merchandise inventory | Account No:114 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 1 | Balance | 20,584 | |||||

| Account: Suppliers | Account No:115 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 1 | Balance | 592 | |||||

| 7 | Purchase | 1 | 108 | 700 | ||||

| Account: Prepaid insurance | Account No:116 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 1 | Balance | 390 | |||||

| Account: Equipment | Account No:121 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 1 | Balance | 3,644 | |||||

| Account: Accounts payable | Account No:212 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 1 | Balance | 600 | |||||

| 4 | 1 | 2,930 | 3,530 | |||||

| 7 | 1 | 600 | 2,930 | |||||

| 7 | 1 | 108 | 3,038 | |||||

| 11 | 2 | 2,930 | 108 | |||||

| 18 | 2 | 5,001 | 5,109 | |||||

| 23 | 3 | 376 | 4,733 | |||||

| Account: Salaries payable | Account No:215 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 31 | 3 | 4,853.70 | 4,853.70 | ||||

| 31 | 3 | 4,853.70 | ||||||

| Account: Employees federal income tax payable | Account No:216 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 31 | 3 | 872 | 872 | ||||

| Account: FICA tax payable | Account No:217 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 31 | 3 | 474.30 | 474.30 | ||||

| 31 | 3 | 474.30 | 948.60 | |||||

| Account: State unemployment tax payable | Account No:218 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 31 | 3 | 334.8 | 334.8 | ||||

| Account: Federal unemployment tax payable | Account No:219 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 31 | 3 | 49.60 | 49.60 | ||||

| Account: Mr. H Capital | Account No:311 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 1 | 35,000 | ||||||

| 2 | 1 | 3,500 | 38,500 | |||||

| Account: Mr. H Drawing | Account No:312 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 31 | 3 | 1,000 | 1,000 | ||||

| Account: Sales | Account No:411 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 4 | 1 | 850 | 850 | ||||

| 7 | 2 | 787 | 1,637 | |||||

| 11 | 2 | 4,863.2 | 6,500.2 | |||||

| 14 | 2 | 2,050 | 8,550.2 | |||||

| 21 | 2 | 4,591 | 13,141.2 | |||||

| 29 | 3 | 1,835 | 14,976.2 | |||||

| 31 | 3 | 4,428 | 19,404.2 | |||||

| Account: Sales return and allowance | Account No:412 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 9 | 2 | 54 | 54 | ||||

| Account: Sales discounts | Account No:413 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 4 | 1 | 20 | 20 | ||||

| 6 | 1 | 13 | 33 | |||||

| Account: Purchases | Account No:511 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 4 | 1 | 2,930 | 2,930 | ||||

| 18 | 2 | 4,854 | 7,784 | |||||

| Account: Purchases returns and allowances | Account No:512 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 23 | 3 | 376 | 376 | ||||

| Account: Purchase discounts | Account No:513 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 7 | 1 | 12 | 12 | ||||

| 11 | 2 | 58.6 | 70.6 | |||||

| Account: Freight in | Account No:514 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 18 | 2 | 147 | 147 | ||||

| 23 | 2 | 96 | 243 | |||||

| Account: Salary expense | Account No:621 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 31 | 3 | 6,200 | 6,200 | ||||

| Account: Payroll tax expense | Account No:622 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 31 | 3 | 858.7 | 858.7 | ||||

| Account: Rent expense | Account No:627 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 2 | 1 | 775 | 775 | ||||

| Account: Miscellaneous expense | Account No:631 | |||||||

| Date | Item | Post ref | Debit | Credit | Balance | |||

| 20___ | ($) | ($) | Debit ($) | Credit($) | ||||

| Jan | 21 | 2 | 194 | 194 | ||||

| 31 | 3 | 53 | 247 | |||||

Table (4)

5.

Prepare a trial balance of H Company.

Explanation of Solution

Trial balance: Trial balance is a summary of all the ledger accounts balances presented in a tabular form with two column, debit and credit. It checks the mathematical accuracy of the ledger postings and helps preparing the final accounts.

Prepare a trial balance.

| H company | |||||

| Trail balance | |||||

| January 31, 20__ | |||||

| Account name | Debit ($) | Credit($) | |||

| Cash | 17,308.1 | ||||

| Accounts receivable | 5,468 | ||||

| Merchandise inventory | 20,584 | ||||

| Supplies | 700 | ||||

| Prepaid insurance | 390 | ||||

| Equipment | 3,644 | ||||

| Accounts payable | 4,733 | ||||

| Employee's federal income tax payable | 872 | ||||

| FICA social security tax payable | 948.6 | ||||

| State unemployment tax payable | 334.8 | ||||

| Federal unemployment tax payable | 49.6 | ||||

| Mr. J capital | 38,500 | ||||

| Mr. J drawings | 1,000 | ||||

| Sales | 19,404.2 | ||||

| Sales returns and allowances | 54 | ||||

| Sales discounts | 33 | ||||

| Purchases | 7,784 | ||||

| Purchases returns and allowances | 376 | ||||

| Purchases discounts | 70.6 | ||||

| Freight in | 243 | ||||

| Salary expense | 6,200 | ||||

| Payroll tax expense | 858.7 | ||||

| Rent expense | 775 | ||||

| Miscellaneous expense | 247 | ||||

| 65,288.8 | 65,288.8 | ||||

Table (5)

6.

Prepare a schedule of accounts receivable and accounts payable.

Explanation of Solution

Schedule of accounts receivable:

| H company | |

| Schedule of Accounts Receivable | |

| January 31, 20__ | |

| Particulars | Amount($) |

| B company | 1,835 |

| E and C company | 787 |

| L company | 796 |

| V company | 2,050 |

| Total accounts receivable | 5,468 |

Table (6)

Schedule of accounts payable

| H company | |

| Schedule of Accounts Payable | |

| January 31, 20__ | |

| Particulars | Amount($) |

| C company | 4,625 |

| D company | 108 |

| Total accounts payable | 4,733 |

Table (7)

Want to see more full solutions like this?

Chapter 10 Solutions

College Accounting - With Quickbooks 2015 CD and Access

- Selby Industries has a standard requirement of 4 direct labor hours for each unit produced and pays $12 per hour. During the last month, the company produced 1,200 units of its product and paid a total of $60,480 in direct labor wages. The labor efficiency variance was $720 favorable. What was the direct labor rate variance? Helparrow_forwardGiven true answer general accountingarrow_forwardCompute the correct cost of goods sold for 2022arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub