(a)

Bonds

Bonds are a kind of interest bearing notes payable, usually issued by companies, universities and governmental organizations. It is a debt instrument used for the purpose of raising fund of the corporations or governmental agencies. If selling price of the bond is equal to its face value, it is called as par on bond. If selling price of the bond is lesser than the face value, it is known as discount on bond. If selling price of the bond is greater than the face value, it is known as premium on bond.

Redemption of Bonds

The process of repaying the sale amount of bonds to bondholders at the time of maturity or before the maturity period is called as redemption of bonds. It is otherwise called as retirement of bonds.

To prepare: The

(a)

Answer to Problem 10.4AP

Prepare the journal entry to record the issuance of bonds for Corporation K on October 1as shown below:

| Date | Account title and Explanation | Debit | Credit |

| October 1, 2016 | Cash | $700,000 | |

| Bonds payable | $700,000 | ||

| (To record the issuance of 5% bonds payable at face value for Corporation K) |

Table (1)

Explanation of Solution

- Cash is a current asset and increased. Therefore, debit Cash account for $396,000.

- Bonds payable is a long-term liability and increased. Therefore, credit bonds payable account for $700,000.

(b)

To prepare: The

(b)

Answer to Problem 10.4AP

The adjusting entry to record the accrual of interest for Corporation K on December 31, 2017 as shown below:

| Date | Account title and Explanation | Debit | Credit |

| December 31, 2016 | Interest expense (1) | $8,750 | |

| Interest payable | $8,750 | ||

| (To record the accrual interest expense for Corporation K) |

Table (2)

Working note:

Calculation of Interest expense for Corporation K is shown below:

Explanation of Solution

- Interest expense is a component of stockholders’ equity and decreased it. Therefore, debit interest expense account for $8,750.

- Interest payable is a current liability and increased. Therefore, credit interest payable account for $8,750.

(c)

To prepare: The

(c)

Answer to Problem 10.4AP

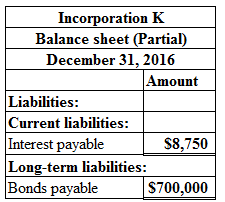

Prepare the balance sheet presentation of bonds payable and bond interest payable of Incorporation K as shown below:

Figure (1)

Explanation of Solution

The balance sheet presentation of interest payable ($8,750) comes under the current liability section and the balance sheet presentation of bonds payable ($700,000) comes under long-term liability section.

(d)

To prepare: The journal entry to record the payment of interest for Corporation K on October 1, 2017.

(d)

Answer to Problem 10.4AP

Prepare the journal entry to record the payment of interest for Corporation K on October 1, 2017 as shown below:

| Date | Account title and Explanation | Debit | Credit |

| October 1, 2017 | Interest expense (1) | $26,250 | |

| Interest payable (3) | $8,750 | ||

| Cash (2) | $35,000 | ||

| (To record the payment of interest expense for Corporation K) |

Table (3)

Working note:

Calculation of interest expense for Corporation K on 1st October 2017 is shown below:

Calculation of cash paid for bonds payable of Corporation K 1st October 2017 is shown below:

Calculation of Interest expense for Corporation K is shown below:

Calculation of Interest payable of Corporation K 1st October 2017 is shown below:

Explanation of Solution

- Interest expense is a stockholders’ equity, and decreased it. Therefore, debit interest expense account for $26,250.

- Interest payable is a current liability and decreased. Therefore, debit interest payable account for $8,750.

- Cash is a current asset account, and decreased. Therefore, cash account for $35,000.

(e)

To prepare: The adjusting entry to record the accrual of interest for Corporation K on December 31, 2017.

(e)

Answer to Problem 10.4AP

The adjusting entry to record the accrual of interest for Corporation K on December 31, 2017 as shown below:

| Date | Account title and Explanation | Debit | Credit |

| December 31, 2017 | Interest expense (1) | $8,750 | |

| Interest payable | $8,750 | ||

| (To record the accrual interest expense for Corporation K) |

Table (4)

Working note:

Calculation of Interest expense for Corporation K is shown below:

Explanation of Solution

- Interest expense is a component of stockholders’ equity and decreased it. Therefore, debit interest expense account for $8,750.

- Interest payable is a current liability and increased. Therefore, credit interest payable account for $8,750.

(f)

To prepare: The journal entry to record the payment of interest for Corporation K on January 1, 2018.

(f)

Answer to Problem 10.4AP

Prepare the journal entry to record the payment of interest for Corporation K on January 1, 2018 as shown below:

| Date | Account title and Explanation | Debit | Credit |

| January 1, 2018 | Interest payable | $8,750 | |

| Cash | $8,750 | ||

| (To record the payment of interest expense for Corporation K) |

Table (5)

Explanation of Solution

Interest payable is a current liability, and decreased. Therefore, interest payable account for $8,750

Cash is a current asset, and decreased. Therefore, cash account for $8,750.

To prepare: The journal entry to record the redemption of bonds for Corporation K on January 1, 2018.

Answer to Problem 10.4AP

Prepare the journal entry to record the redemption of bonds for Corporation K on January 1, 2018 as shown below:

| Date | Account title and Explanation | Debit | Credit |

| January 1, 2018 | Bonds payable | $700,000 | |

| Loss on redemption of bonds (2) | $28,000 | ||

| Cash (1) | $728,000 | ||

| (To record the redemption of bonds before the maturity period for Corporation K) |

Table (6)

Working notes:

Calculation of cash paid for redemption of bonds payable is shown below:

Calculation of loss on redemption of bonds payable is shown below:

Explanation of Solution

Bonds payable is a long-term liability, and decreased. Therefore, debit bonds payable account for $700,000

Loss on redemption of bonds is a component of stockholders’ equity, and decreased. Therefore, debit loss on redemption of bonds for $28,000.

Cash is a current asset, and decreased. Therefore, credit cash account for $728,000

Want to see more full solutions like this?

Chapter 10 Solutions

Financial Accounting, Binder Ready Version: Tools for Business Decision Making

- Marilyn Terrill is the senior auditor for the audit of Uden Supply Company for the year ended December 31, 20X4. In planning the audit, Marilyn is attempting to develop expectations for planning analytical procedures based on the financial information for prior years and her knowledge of the business and the industry, including these: 1. Based on economic conditions, she believes that the increase in sales for the current year should approximate the historical trend in terms of actual dollar increases. 2. Based on her knowledge of industry trends, she believes that the gross profit percentage for 20X4 should be about 2 percent less than the percentage for 20X3. 3. Based on her knowledge of regulations, she is aware that the effective tax rate for the company for 20X4 has been reduced by 5 percent from that in 20X3. 4. Based on her knowledge of economic conditions, she is aware that the effective interest rate on the company's line of credit for 20X4 was approximately 12 percent. The…arrow_forwardAnswer this question general accountingarrow_forwardNeed correct answer general Accountingarrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning