Videos

Nike: Somewhere between a Swoosh and a Slam Dunk

Nike, Inc.’s principal business activity involves the design, development, and worldwide marketing of high-quality footwear, apparel, equipment, and accessory products for serious and recreational athletes. Almost 25,000 employees work for the firm as of 2009. Nike boasts the largest worldwide market share in the athletic footwear industry and a leading market share in sports and athletic apparel.

This case uses Nike’s financial statements and excerpts from its notes to review important concepts underlying the three principal financial statements (

Industry Economics

Product Lines

Industry analysts debate whether the athletic footwear and apparel industry is a performancedriven industry or a fashion-driven industry. Proponents of the performance view point to Nike’s dominant market position, which results in part from continual innovation in product development. Proponents of the fashion view point to the difficulty of protecting technological improvements from competitor imitation, the large portion of total expenses comprising advertising, the role of sports and other personalities in promoting athletic shoes, and the fact that a high percentage of athletic footwear and apparel consumers use the products for casual wear rather than the intended athletic purposes (such as playing basketball or running).

Growth

There are only modest growth opportunities for footwear and apparel in the United States. Concern exists with respect to volume increases (how many pairs of athletic shoes will consumers tolerate in their closets) and price increases (will consumers continue to pay prices for innovative athletic footwear that is often twice as costly as other footwear).

Athletic footwear companies have diversified their revenue sources in two directions in recent years. One direction involves increased emphasis on international sales. With dress codes becoming more casual in Europe and East Asia and interest in American sports such as basketball becoming more widespread, industry analysts view international markets as the major growth markets during the next several years. Increased emphasis on soccer (European football) in the United States aids companies such as Adidas that have reputations for quality soccer footwear.

The second direction for diversification is sports and athletic apparel. The three leading athletic footwear companies capitalize on their brand name recognition and distribution channels to create a line of sportswear that coordinates with their footwear. Team uniforms and matching apparel for coaching staffs and fans have become a major growth avenue. For example, to complement Nike’s footwear sales, Nike acquired Umbro, a major brand-name line of jerseys, shorts, jackets, and other apparel in the soccer market.

Production

Essentially all athletic footwear and most apparel are produced in factories in Asia, primarily China (40%), Indonesia (31%), Vietnam, South Korea, Taiwan, and Thailand. The footwear companies do not own any of these manufacturing facilities. They typically hire manufacturing representatives to source and oversee the manufacturing process, helping to ensure quality control and serving as a link between the design and the manufacture of products. The manufacturing process is labor-intensive, with sewing machines used as the primary equipment. Footwear companies typically price their purchases from these factories in U.S. dollars.

Marketing

Athletic footwear and sportswear companies sell their products to consumers through various independent department, specialty, and discount stores. Their sales forces educate retailers on new product innovations, store display design, and similar activities. The market shares of Nike and the other major brand-name producers dominate retailers’ shelf space, and slower growth in sales makes it increasingly difficult for the remaining athletic footwear companies to gain market share. The slower growth also has led the major companies to increase significantly their advertising and payments for celebrity endorsements. Many footwear companies, including Nike, have opened their own retail stores, as well as factory outlet stores for discounted sales of excess inventory.

Athletic footwear and sportswear companies have typically used independent distributors to market their products in other countries. With increasing brand recognition and anticipated growth in international sales, these companies have recently acquired an increasing number of their distributors to capture more of the profits generated in other countries and maintain better control of international marketing.

Financing

Compared to other apparel firms, the athletic footwear firms generate higher profit margins and

Nike Strategy

Nike targets the serious athlete with performance-driven footwear and athletic wear, as well as the recreational athlete. The firm has steadily expanded the scope of its product portfolio from its primary products of high-quality athletic footwear for running, training, basketball, soccer, and casual wear to encompass related product lines such as sports apparel, bags, equipment, balls, eyewear, timepieces, and other athletic accessories. In addition, Nike has expanded its scope of sports, now offering products for swimming, baseball, cheerleading, football, golf, lacrosse, tennis, volleyball, skateboarding, and other leisure activities. In recent years, the firm has emphasized growth outside the United States. Nike also has grown by acquiring other apparel companies, including Cole Haan (dress and casual footwear), Converse (athletic and casual footwear and apparel), Hurley (apparel for action sports such as surfing, skateboarding, and snowboarding), and Umbro (footwear, apparel, and equipment for soccer). The firm sums up the company’s philosophy and driving force behind its success as follows:

Nike designs, develops, and markets high quality footwear, apparel, equipment and accessory products worldwide. We are the largest seller of athletic footwear and apparel in the world. Our strategy is to achieve long-term revenue growth by creating innovative, “must-have” products; building deep, personal consumer connections with our brands; and delivering compelling retail presentation and experiences.

To maintain its technological edge, Nike engages in extensive research at its research facilities in Beaverton, Oregon. It continually alters its product line to introduce new footwear, apparel, equipment, and evolutionary improvements in existing products.

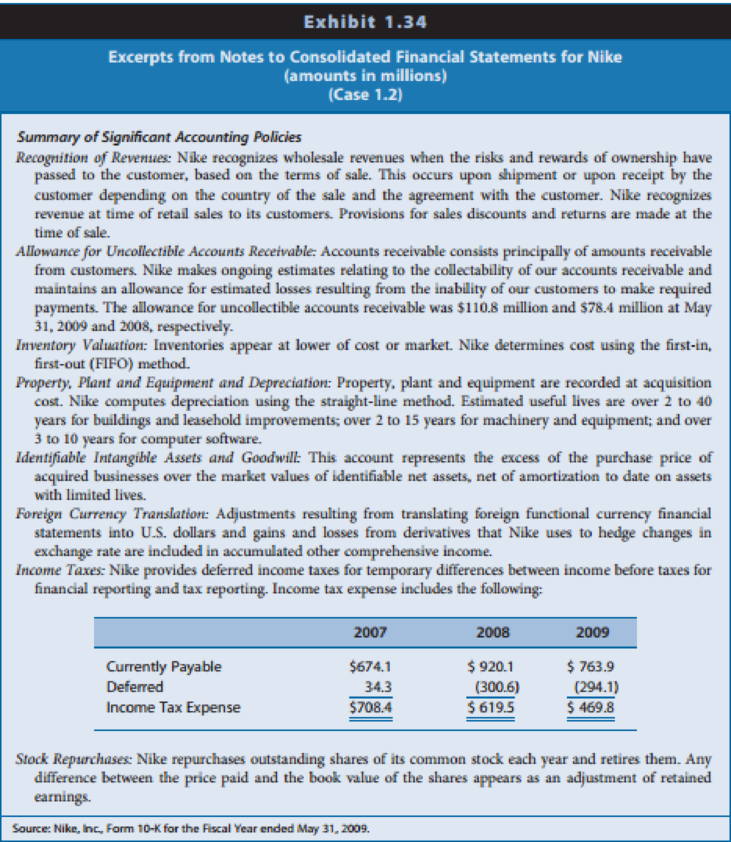

Nike maintains a reputation for timely delivery of footwear products to its customers, primarily as a result of its “Futures” ordering program. Under this program, retailers book orders five to six months in advance. Nike guarantees delivery of the order within a set time period at the agreed price at the time of ordering. Approximately 89% of the U.S. footwear orders received by Nike during 2009 came through its Futures program. This program allows the company to improve production scheduling, thereby reducing inventory risk. However, the program locks in selling prices and increases Nike’s risk of increased raw materials and labor costs. Independent contractors manufacture virtually all of Nike’s products. Nike sources all of its footwear and approximately 95% of its apparel from other countries.

The following exhibits present information for Nike:

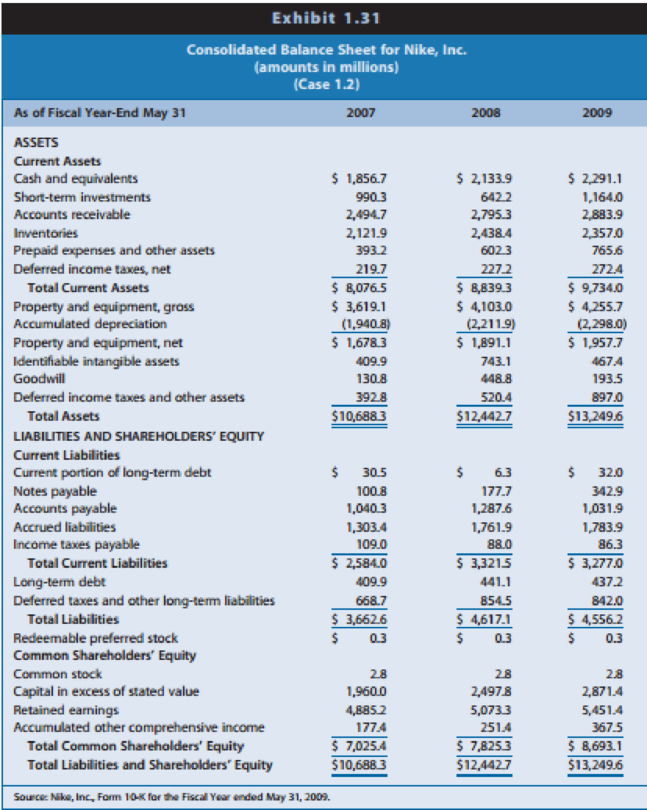

Exhibit 1.31: Consolidated balance sheets for 2007, 2008, and 2009

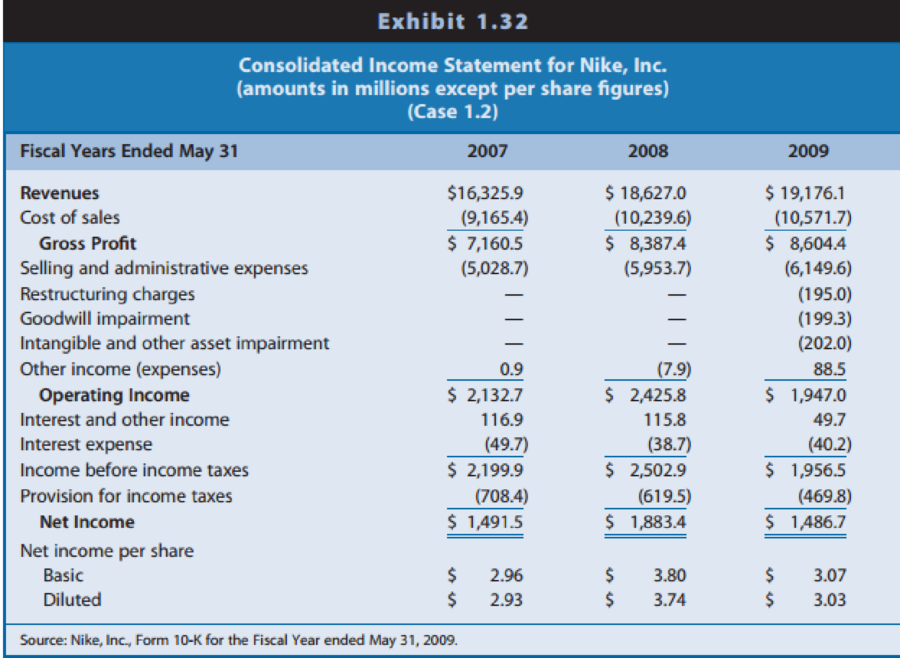

Exhibit 1.32: Consolidated income statements for 2007,2008, and 2009

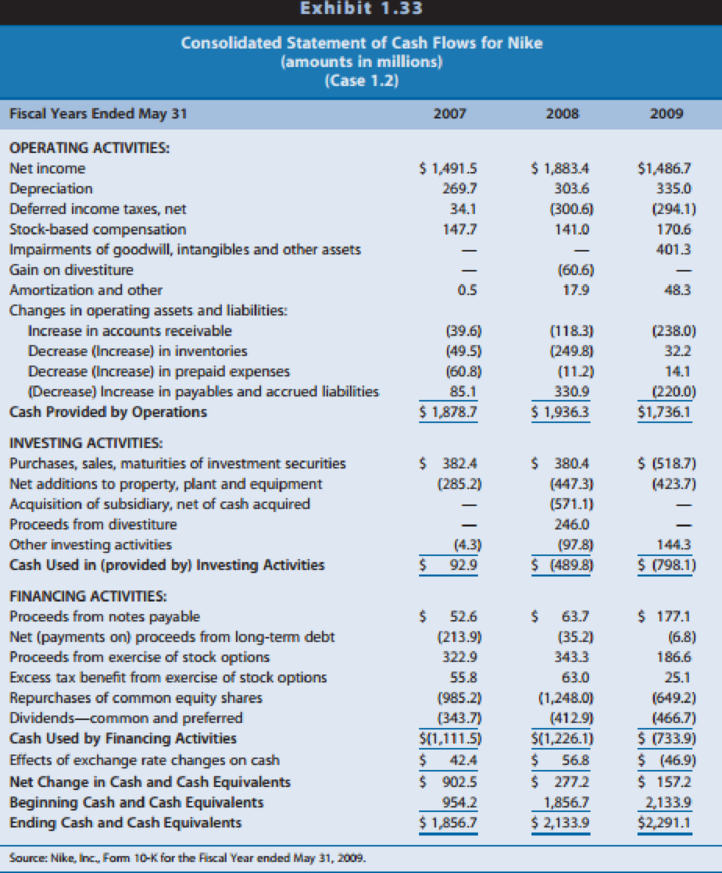

Exhibit 1.33: Consolidated statements of cash flows 2007, 2008, and 2009

Exhibit 1.34: Excerpts from the notes to Nike’s financial statements

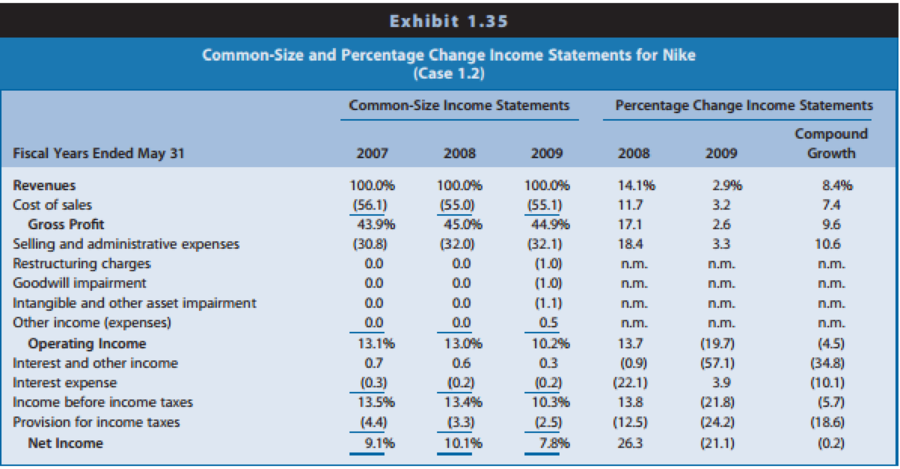

Exhibit 1.35: Common-size and percentage change income statements

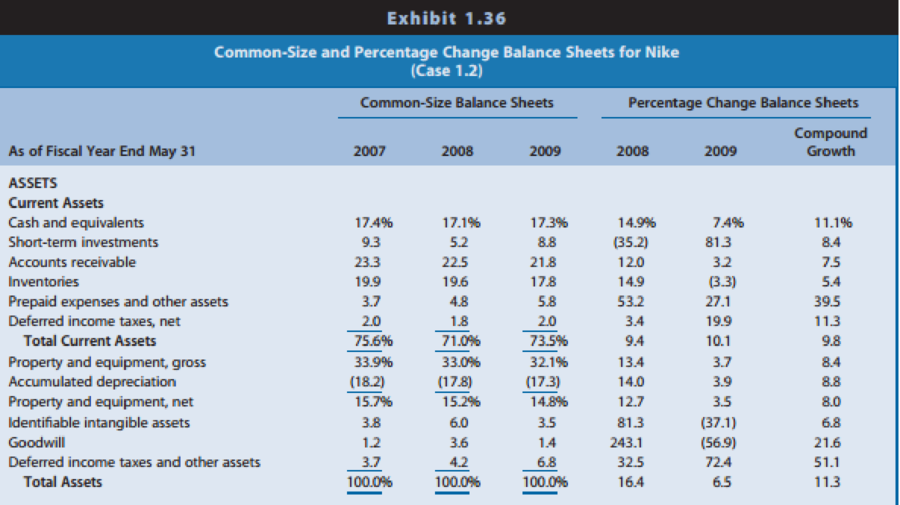

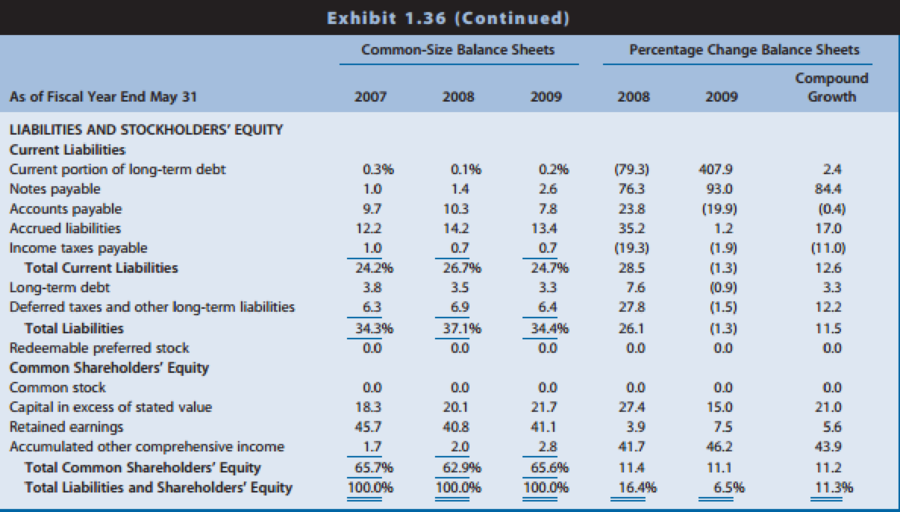

Exhibit 1.36: Common-size and percentage change balance sheets

Identify the time at which Nike recognizes revenues. Does this timing of revenue recognition seem appropriate? Explain.

REQUIRED

Study the financial statements and notes for Nike and respond to the following questions.

What are the likely reasons for the increase in the selling and administrative expenses to sales percentages between 2007 and 2009?

What is the likely explanation for the relatively small percentages for notes payable and long-term debt?

Want to see the full answer?

Check out a sample textbook solution

Chapter 1 Solutions

EBK FINANCIAL REPORTING, FINANCIAL STAT

- If data is unclear or blurr then comment i will write it. please don't use AI i will unhelpfularrow_forwardYou are considering an option to purchase or rent a single residential property. You can rent it for $5,000 per month and the owner would be responsible for maintenance, property insurance, and property taxes. Alternatively, you can purchase this property for $204,500 and finance it with an 80 percent mortgage loan at 4 percent interest that will fully amortize over a 30-year period. The loan can be prepaid at any time with no penalty. You have done research in the market area and found that (1) properties have historically appreciated at an annual rate of 2 percent per year, and rents on similar properties have also increased at 2 percent annually; (2) maintenance and insurance are currently $1,545.00 each per year and they have been increasing at a rate of 3 percent per year; (3) you are in a 24 percent marginal tax rate and plan to occupy the property as your principal residence for at least four years; (4) the capital gains exclusion would apply when you sell the property; (5)…arrow_forwardIf data is unclear or blurr then comment i will write it.arrow_forward

- I need answer typing clear urjent no chatgpt used pls i will give 5 Upvotes.arrow_forwardcorrect an If image is blurr or data is unclear then plz comment i will write values or upload a new image. i will give unhelpful if you will use incorrect data.arrow_forwardWhat are the five management assertions that serve as basis for financial statements audit programs?arrow_forward

- PROBLEM 2 On July 1, 2022, LTU Contracting, Inc. purchased a new Peiner SK575 Tower Crane for a total cost of $875,000. The crane has an estimated useful life of five (5) years. For financial reporting (book) purposes, the company utilizes straight line depreciation. For tax purposes, the equipment is depreciated over five years utilizing the 200% declining balance method. A. Prepare a table that computes the book and tax depreciation for each year of the useful life and determine the difference in book value between each method at the end of each year. B. On July 1st, 2025, the company is considering selling the crane for $500,000. Compute what the gain or loss would have been at that time for both book and tax purposes.arrow_forwardBrightwoodę Furniture provides the following financial data for a given enod: Sales Aount ($) Per Unit ($) 150,000 13 Less Variable E - L96,000 13 Contribwaon Margin c 1C Less Fixed Expenses $5,000 et Income 125,000 a. What is the company's CM ratio? b. If quarterly sales increase by $5,200 and there is no change in fixed expenses, by how much would you expect quarterly net operating income to increase?arrow_forwardPlease give correct answer dont use chatgpt . if image is blurr or any data is unclear then please comment i will write values , dont give answer without sure that data in image is showing properly.arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Auditing: A Risk Based-Approach to Conducting a Q...AccountingISBN:9781305080577Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:South-Western College PubPrinciples of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Auditing: A Risk Based-Approach to Conducting a Q...AccountingISBN:9781305080577Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:South-Western College PubPrinciples of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub