Videos

Addison Parker (Social Security number 123-45-6785), single and age 32, lives at 3218 Columbia Drive, Spokane, WA 99210. She is employed as regional sales manager by VITA Corporation, a manufacturer and distributor of vitamins and food supplements. Addison is paid an annual salary of $83,000 and a separate travel allowance of $28,000. In order to access the travel allowance, VITA requires adequate accounting by Addison.

- Addison participates in VITA’s contributor)* health and § 401(k) plans. During 2019, she paid $4,500 for her share of the medical insurance and contributed $11,000 to the § 401(k) retirement plan.

- Addison uses her automobile 70% for business and 30% for personal. The automobile, a Toyota Avalon, was purchased new on June 30, 2017, for $37,000 (no trade-in was involved).

Depreciation has been claimed using the MACRS 200% declining-balance method, and no § 179 election was made in the year of purchase. (For depreciation information, see the IRS Instructions for Form 4562, Part V.) During 2019, Addison drove 15,000 miles and incurred and paid the following expenses relating to the automobile:

- Because VITA does not have an office in Spokane, the company expects Addison to maintain one in her home. Out of 1.500 square feet of living space in her apartment, Addison has set aside 300 square feet as an office. Expenses for 2019 relating to the office are listed below.

- Addison’s employment-related expenses (except for the trip to Korea) for 2019 are summarized below.

Most of Addison’s business trips involve visits to retail outlets in her region. Store managers and their key employees, as well as some suppliers, were the parties entertained. The business gifts were boxes of candy costing $30 ($25 each plus $5 for wrapping and shipping) sent to 18 store managers at Christmas. The continuing education was a noncredit course dealing with improving management skills that Addison took online.

- In July 2019, Addison traveled to Korea to investigate a new process that is being developed to convert fish parts to a solid consumable tablet form. She spent one week checking out the process and then took a one-week vacation tour of the country. The round-trip airfare was $3,600, and her expenses relating to business were $2,100 for lodging ($300 each night), $1,470 for meals, and $350 for transportation. Upon returning to the United States, Addison sent her findings about the process to her employer. VITA was so pleased with her report that it gave her an employee achievement award of $10,000. The award was sent to Addison in January 2020.

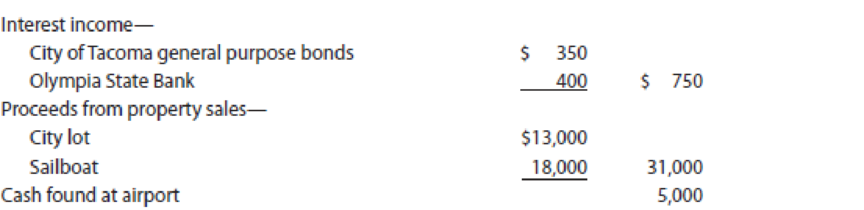

- Besides the items already mentioned, Addison had the following receipts in 2019:

Regarding the city lot (located in Vancouver), Addison purchased the property in 2004 for $16,000 and held it as an investment. Unfortunately, the neighborhood where the lot was located deteriorated, and property values declined. In 2019, Addison decided to cut her losses and sold the property for $13,000. The sailboat was used for pleasure and was purchased in 2015 for $16,500. Addison sold the boat because she purchased a new and larger model (see below). While at the Spokane airport, Addison found an unmarked envelope containing 55,000 in $50 bills. Because no mention of any lost funds was noted in the media, Addison kept the money.

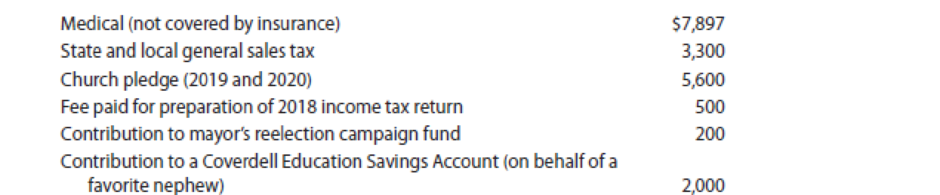

- Addison’s expenditures for 2019 (not previously noted) are summarized below.

Addison keeps careful records regarding sales taxes. In 2019, the sales tax total was unusually high due to the purchase of a new sailboat. In 2019, Addison decided to pay her church pledge for both 2019 and 2020. The insurance premium was on a policy covering her father’s life. (Addison is the designated beneficiary under the policy.)

Addison’s employer withheld $8,600 for Federal income tax purposes, and she applied her $800 overpayment for 2018 toward the 2019 tax liability.

Compute Addison’s Federal income tax payable (or refund) for 2019. In making the calculation, use the ‘Fax Rate Schedule and disregard the application of the alternative minimum tax (AMI*), which is not discussed until Chapter 12.

Calculate the Mrs. C’s federal income tax.

Explanation of Solution

Federal Income Tax: Federal income tax is the tax imposed by the federal government on the income of an individual and business organization. Federal income tax has a standard base for certain level of income.

Calculate the Mrs. C’s federal income tax.

| Particulars | Amount ($) | Amount ($) |

| Salary (Note 1) | 83,000 | |

| Expense allowance (Note 2) | 0 | |

|

Contribution to § 401 (k) retirement plan (Note 3) | (11,000) | |

| Interest income (Note 4) | 400 | |

| Treasure trove (Note 5) | 5,000 | |

| Property transactions (Note 6): | ||

| Loss on sale of lot | (3,000) | |

| Gain on boat | 1,500 | (1,500) |

| Adjusted gross income | 75,900 | |

| Itemized deductions: | ||

| Medical (Note 7) | 4,807 | |

| Sales tax (Note 8) | 3,300 | |

| Charitable contributions (Note 9) | 5,600 | |

| Campaign contribution (Note 10) | 0 | |

| Premium of life insurance (Note 11) | 0 | |

| Contribution to Coverdell education savings account (Note 12) | 0 | (13,707) |

| Taxable income | 62,193 | |

| Tax liability on taxable income of $62,193using the 2019 tax rate schedule for single taxpayers | 9,541 | |

| Less: | ||

| Withholding | 8,600 | |

| Overpayment from 2018 | 800 | (9,400) |

| Net tax due for 2019 | 141 |

Table (1)

Notes:

(1) Since it was not received in 2019, gross income does not include the achievement award $10,000. Mr. A does not recognize income until the year of its receipt, as cash basis taxpayer.

(2) Ms. A is required to provide an adequate accounting to VITA. Ms. A keeps records of her various expenses and submits them to VITA for reimbursement. Employee business expenses are considered as excess expenses.

Compute excess expenses.

| Particulars | Amount ($) | Amount ($) |

| Expense allowance | 28,000 | |

| Expenses: | ||

| Office in the home (Note 13) | 5,920 | |

| Business use of auto (Note 14) | 7,943 | |

| Employee expense (Note 15) | 4,985 | |

| Other employee expenses (Note 16) | 11,480 | |

| Total expenses | 30,328 | |

| Expense allowance used | (28,000) | |

| Excess expenses | 2,328 |

Table (2)

Expense allowance will effectively be offset by $28,000 of for AGI deductions; Since Mr. A provided adequate accounting to her employer. Expense allowance to Ms. A as income will not be reported as VITA. The excess expenses are miscellaneous itemized deductions, since Ms. A’s expenses exceeded her allowance. Congress suspended miscellaneous itemized deductions from 2018 through 2025 so, they are not deductible.

(3) In W–2 submitted by the employer is netted out from salary.

(4) The interest $350 on the City of Tacoma bonds is not subject to tax.

(5) Cash of $5,000 found by Ms. A is income.

(6) Gain on sales is $1,500 because gain on sale of personal use property is taxed. Since, Sale of the ATV is zero because Mr. C paid $14,000 as a result its $5,000 loss. Therefore, it is not deductible in case of personal losses. The result is a net long-term capital loss of $1,500, when offset against a long-term capital loss of $3,000.

(7) Compute medical expense after limitation.

| Particulars | Amount ($) |

| Medical expenses paid | 7,897 |

| Medical insurance premium | 4,500 |

| Total medical expenses | 12,397 |

| Less limitation | (7,590) |

| Medical expense after limitation | 4,807 |

Table (3)

(8) Since, Mr. A could justify a larger amount IRS sales tax tables did not have to be used.

(9) Charitable contributions are subject to deductions.

(10) Deduction is not subject to political contributions

(11) Premiums on personal life insurance policies are not subject to deduction.

(12) Contributions to Coverdell Education Savings Accounts (CESAs) are not subject to deduction. CESAs are subject to deduction from gross income.

(13) Percentage of office in the home business is 20% (300 sq. ft. /1,500 sq. ft.).

- Direct expense is $1,200.

- Indirect expenses are $4,720

(14) Compute the business use of auto.

| Particulars | Amount ($) |

| Gasoline | 3,100 |

| Depreciation | 3,050 |

| Insurance | 2,900 |

| Auto club dues | 240 |

| Interest on car loan | 0 |

| Repairs and maintenance | 1,200 |

| Total (a) | 10,490 |

| Business percentage (b) | 70% |

| Business portion (a x b) | 7,343 |

| Add: Business parking | 600 |

| Total auto deduction | 7,943 |

Table (4)

Traffic fines are not subject to deduction even during business use.

Regular depreciation for automobiles is $7,104 ($37,000 x 19.2%).

(15) Compute employee expenses:

| Particulars | Amount ($) | Amount ($) |

| Airfare | 1,800 | |

| Lodging | 2,100 | |

| Meals | 1,470 | |

| Less: 50% limit | (735) | 735 |

| Transportation | 350 | |

| Total | 4,985 |

Table (5)

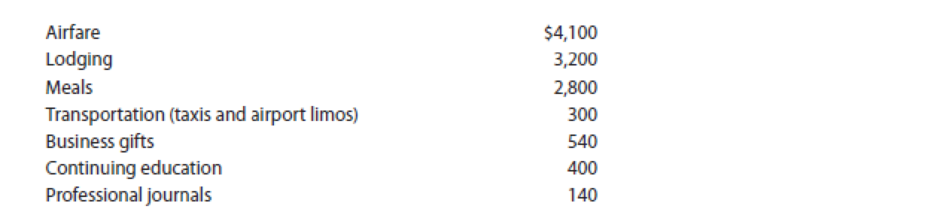

(16) Compute other employee expenses:

| Particulars | Amount ($) |

| Airfare | 4,100 |

| Lodging | 3,200 |

| Meals | 2,800 |

| Transportation | 300 |

| Business gifts | 540 |

| Continuing education | 400 |

| Professional journals | 140 |

| Total | 11,480 |

Table (6)

Gift wrapping and shipping can be added to the $25 maximum allowed, since business gifts are allowed in full.

Want to see more full solutions like this?

Chapter 9 Solutions

Individual Income Taxes

- Please provide the solution to this general accounting question with accurate financial calculations.arrow_forwardI need guidance with this general accounting problem using the right accounting principles.arrow_forwardHow can I solve this financial accounting problem using the appropriate financial process?arrow_forward

- Transactions: Dec. 3 Wrote off Langston Corporation’s past-due account as uncollectible, $645.75. M203. 9 Accepted a 90-day, 8% note from Farris Company for an extension of time on its account, $2,400.00. NR23. 18 Received cash from Storage Solutions for the maturity value of NR19, a 90-day, 9% note for $2,000.00. R455. 21 Coastal Supply dishonored NR21, a 90-day, 8% note, for $3,000.00. M245. 30 Received cash in full payment of Langston Corporation’s account, previously written off as uncollectible, $645.75. M232 and R463. Task 1 Journalize the transactions for Miller Corporation in Questions Assets that were completed during December of the current year. Use page 12 of the general journal and page 12 of the cash receipts journal. Task 2 Post each entry to the general ledger and to the customer accounts in the accounts receivable ledger. You will not need to make entries to the Item columns of the ledgers. Task 3 Continue to…arrow_forwardE-M:11-18 Using payback to make capital investment decisions Consider the following three projects. All three have an initial investment of $600,000. Net Cash Inflows Year Project L Project M Project N Annual Accumulated Annual Accumulated Annual Accumulated 1 $ 150,000 $ 150,000 $ 100,000 $ 100,000 $ 300,000 $300,000 2 150,000 300,000 200,000 300,000 300,000 600,000 3 150,000 450,000 300,000 600,000 4 150,000 600,000 400,000 1,000,000 5 150,000 750,000 500,000 1,500,000 6 150,000 900,000 7 150,000 1,050,000 8 150,000 1,200,000 1. Determine the payback period of each project. Rank the projects from most desirable to least desirable based on payback. 2. Are there other factors that should be considered in addition to the payback period?arrow_forwardKindly help me with this General accounting questions not use chart gpt please fast given solutionarrow_forward

- Horngren's Financial & Managerial Accounting: The Managerial Chapters, 8th Edition E-M:10-12 Making pricing decisions Sufyan Builders builds 1,500-square-foot starter tract homes in the fast-growing suburbs of Atlanta. Competition among developers is fierce. The homes are a standard model, with any upgrades added by the buyer after the sale. Sufyan Builders’ costs per developed sublot are as follows:Land $ 59,000Construction 124,000Landscaping 6,000Variable selling costs 5,000 Sufyan Builders would like to earn a profit of 14% of the variable cost of each home sold. Similar homes offered by competing builders sell for $208,000 each. Assume the company has no fixed costs. Questions:1. Which approach to pricing should Sufyan Builders emphasize? Why? 2. Will Sufyan Builders be able to achieve its target profit levels? 3. Bathrooms and kitchens are typically the most important selling features of a home. Sufyan Builders could…arrow_forwardCan you provide a detailed solution to this financial accounting problem using proper principles?arrow_forwardPlease explain the solution to this general accounting problem with accurate explanations.arrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT