Subpart (a):

Calculate different costs.

Subpart (a):

Explanation of Solution

Total cost (TC) can be obtained by using the following formula.

Total cost at production level 1 unit can be calculated by substituting the respective values in Equation (1).

Total cost is $105.

Average fixed cost (AFC) can be obtained by using the following formula.

Average fixed cost at production level 1 unit can be calculated by substituting the respective values in Equation (2).

Average fixed cost is $60.

Average variable cost at production level 1 unit can be calculated by substituting the respective values in Equation (3).

Average variable cost is $45.

Total average cost (AC) can be obtained by using the following formula.

Total average cost at production level 1 unit can be calculated by substituting the respective values in Equation (4).

Average variable cost is $105.

Marginal cost (MC) can be obtained by using the following formula.

Average variable cost at production level 1 unit can be calculated by substituting the respective values in Equation (5).

Marginal cost is $105.

Table-1 shows the total cost, average fixed cost, average variable cost,

Table -1

| Quantity | Fixed cost | Variable cost | TC | AFC | AVC | AC | MC |

| 0 | 60 | 0 | 60 | ||||

| 1 | 60 | 45 | 105 | 60 | 45.00 | 105.00 | 45 |

| 2 | 60 | 85 | 145 | 30 | 42.50 | 72.50 | 40 |

| 3 | 60 | 120 | 180 | 20 | 40.00 | 60.00 | 35 |

| 4 | 60 | 150 | 210 | 15 | 37.50 | 52.50 | 30 |

| 5 | 60 | 185 | 245 | 12 | 37.00 | 49.00 | 35 |

| 6 | 60 | 225 | 285 | 10 | 37.50 | 47.50 | 40 |

| 7 | 60 | 270 | 330 | 8.57 | 38.57 | 47.14 | 45 |

| 8 | 60 | 325 | 385 | 7.50 | 40.63 | 48.13 | 55 |

| 9 | 60 | 390 | 450 | 6.67 | 43.33 | 50.00 | 65 |

| 10 | 60 | 465 | 525 | 6 | 46.50 | 52.50 | 75 |

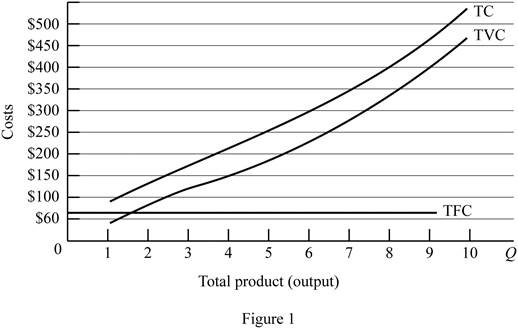

Figure -1 illustrates the shape of total fixed cost, total cost and total variable cost that influencing by the diminishing returns to scale.

In figure -1, horizontal axis measures total output and vertical axis measures cost. The curve TC indicates total cost and the curve TVC indicates total variable cost. TFC curve indicates total fixed cost. Since total fixed cost is remain the same over the different level of production TFC curve parallel to the horizontal axis.

From the output range 1 unit to 4 units, total cost and total variable cost increasing at decreasing rate due to the increasing marginal returns. Thereafter, these two cost curves are increasing at increasing rate due to the diminishing marginal cost.

Concept introduction:

Fixed cost: Fixed costs refer to those costs that remain the same regardless of the level of production.

Variable cost: Variable cost refers to the costs that change due to the changes occurring in the level of production.

Subpart (b):

Calculate different costs.

Subpart (b):

Explanation of Solution

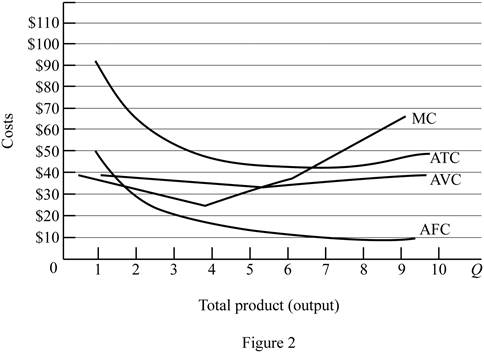

Figure -2 illustrates relationship between marginal cost, average variable cost, average fixed cost and average total cost curve.

In figure -2, horizontal axis measures total output and vertical axis measures cost. The curve TC indicates total cost and the curve TVC indicates total variable cost. TFC curve indicates total fixed cost. Since total fixed cost is remain the same over the different level of production TFC curve parallel to the horizontal axis.

Since the fixed cost is spread over all the output, increasing the level of output leads to reduce the average fixed cost over the increasing production. Marginal cost curve average variable cost curve and average total cost curve are U shaped due to the operation of economies of scale and diseconomies of scale.

Average total cost curve is the vertical summation of average fixed cost and average variable cost. When the marginal cost curve is below to the average total cost curve, then the average total cost falls. When the marginal cost lies above the average total cost curve then the average total cost curve start rises. Thus, marginal cost curve intersects with the average total cost curve at the minimum point.

When the marginal cost curve is below to the average variable cost curve, then the average variable cost falls. When the marginal cost lies above the average variable cost curve then the average variable cost curve start rises. Thus, marginal cost curve intersects with the average variable cost curve at the minimum point.

Concept introduction:

Fixed cost: Fixed costs refer to those costs that remain the same regardless of the level of production.

Variable cost: Variable cost refers to the costs that change due to the changes occurring in the level of production.

Subpart (c):

Fixed cost and variable cost.

Subpart (c):

Explanation of Solution

The increasing fixed cost from $60 to $100 leads to shifts the fixed cost curve upward (By $40). This increasing fixed cost does not affect the marginal cost. Thus, marginal cost curve and average variable cost curve remains the same.

The decrease in variable cost by $10 leads to reduce the marginal cost $10 at first level of output and remains the same for other level of output. Average total cost and average variable cost decreases as a result of decrease in the variable cost. But, average fixed cost remains the same.

Concept introduction:

Fixed cost: Fixed costs refer to those costs that remain the same regardless of the level of production.

Variable cost: Variable cost refers to the costs that change due to the changes occurring in the level of production.

Want to see more full solutions like this?

Chapter 9 Solutions

Economics: Principles, Problems, & Policies (McGraw-Hill Series in Economics) - Standalone book

- 4. Case 3) Electricity demand increases due to increased EV adoption We will continue using the Case 2 supply curve (with the solar plant in operation) for this analysis. Suppose that electricity consumption from electric vehicles (EV) increases significantly. Consequently, electricity demand in the wholesale market increases at every hour. The new demand levels are shown in Table 5 below. The market operator has backup power plants (using natural gas) ready, with a total capacity of 300 MW and a MC of $100/MWh. Table 5: Hourly Demand (selected hours) Hour Demand (MWh) 4 AM 800 10 AM 1000 ... 2 PM 1100 ... 6 PM 1300 (a) Find the market clearing prices and calculate how much electricity each power plant generates in the hourly market (4AM, 10AM, 2PM, and 6PM). Is there a specific hourly market in which the market operator will need to dispatch backup generation? (b) Compare the Case 2 scenario with the Case 3 scenario in terms of CO2 emissions and average electricity price. Based on…arrow_forward2. Case 1) NG price decreases Now, suppose that the price of natural gas decreased substantially, causing the marginal cost of the NG power plant to decrease to MC = $35/MWh. The demand is the same as in Case 0. (a) Draw a new supply curve that reflects the MC change of the NG power plant. (b) Find the market clearing prices and calculate how much electricity each power plant generates in the hourly market (4AM, 10AM, 2PM, and 6PM). (c) What happened to the coal power plant? (d) Do you think the market outcomes (like average price) and the total CO2 emissions have improved under this Case 1 scenario (use the emissions data provided in the lecture slides)?arrow_forward1. Case 0) Baseline case Table 1: Power Plant Capacity and Marginal Cost: Case 0 Plant # Energy Source Capacity (MW) MC (S/MWh) 1 Coal 300 45 2 Oil 100 90 3 4 Natural Gas Nuclear 500 50 600 0 (a) Calculate the capacity mix of this market by energy source. (b) Draw a supply curve of this wholesale generation market. Table 2 below shows the demand levels for selected hours of a representative day. We will consider only these four hourly markets for our analysis. Note that the 6 PM demand is the highest demand level of the day. Table 2: Hourly Demand (selected hours) Hour Demand (MWh) 4 AM 500 10 AM 700 2 PM 800 6 PM 1000 (c) Find the market clearing prices and calculate how much electricity each power plant generates in the hourly market (4AM, 10AM, 2PM, and 6PM). (d) Find the average price of electricity (by taking a simple average of hourly prices; [P(4am) + P(10AM) + P(2PM) + P(6PM)]/4).arrow_forward

- Don't used Ai solutionarrow_forwardHow human recource allocated in an economic?arrow_forwardRespond to B.A. I have chosen Gross Domestic Product (GDP) as the macroeconomic indicator to review and provide a forecast prediction. Based on the current trend I predict a 2% annual GDP growth rate, indicating an unstable economy due to the impact of Donald Trump's tariffs on some countries and other other economic factors. This growth rate is lower than the historical average , indicating a slowdown in economic expansion. Overall, the forecast suggests a modest growth in GDP, but with potential risks and uncertainties ahead. But if he reverse his tariff policies, I think it could possibly result in a strong economic growth. As the removal of tariffs would likely minimize the costs for businesses and consumers and also rise trade and economic activities. Provide feedback/comments this post. You could agreement or disagreement (including why you agree or disagree). Or you could expand on this post by sharing different views and predictions.arrow_forward

- Can you show me how to solve this.arrow_forwardECON 2106: Microeconomics I Fall - 2023 Algoma University Homework # 2 (Due: October 19, 2023) 1. The market demand for cashmere socks is given by Q = 1,000 + 0.5I – 400P + 200P’ Where, Q = Annual demand in number of pairs I = Average income I dollars per year P = Price of one pair of cashmere shocks P’ = Price of one pair of wool shocks Given that I = ECON 2106: Microeconomics I Fall - 2023 Algoma University Homework # 2 (Due: October 19, 2023) 1. The market demand for cashmere socks is given by Q = 1,000 + 0.5I – 400P + 200P’ Where, Q = Annual demand in number of pairs I = Average income I dollars per year P = Price of one pair of cashmere shocks P’ = Price of one pair of wool shocks Given that I = $20,000, P = $10, and P’ = $5, determine ƐQP, ƐQI, and ƐQP’.arrow_forwardWhat bill are they currently sponsoring? Please provide the answer to the question using www.akleg.gov for Senate Bill 30?arrow_forward

- Do they have any specified areas of interest( examples: oil/gas, education, subsistence). Please provide the answer to the question using www.akleg.gov for Senate Bill 30?arrow_forwardA brief synopsis of whether you believe they represent your interest, why or why not? Please provide the answer to this question by using www.akleg for senate bill 30 ?arrow_forwardWhat is their background (degree, career/job, community of origin, anything else you choose to include) Please provide the answers using www.akleg.gov for Senate Bill 30?arrow_forward

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax

Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax