Concept explainers

Videos

Entries for

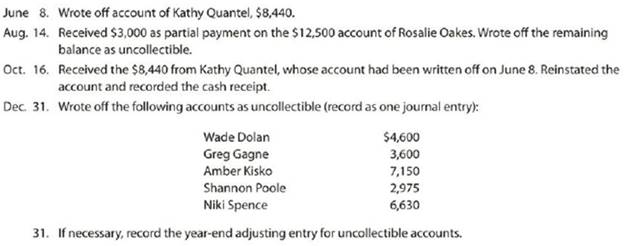

The following selected transactions were taken from the records of Rustic Tables Company for the year ending December 31:

- A. Journalize the transactions under the direct write-off method.

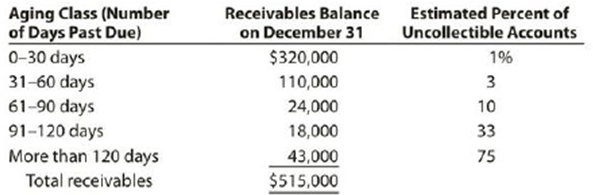

- B. Journalize the transactions under the allowance method, assuming that the allowance account had a beginning balance of $36,000 at the beginning of the year and the company uses the analysis of receivables method. Rustic Tables Company prepared the following aging schedule for its

accounts receivable :

- C. How much higher (lower) would Rustic Tables’ net income have been under the direct write-off method than under the allowance method?

A.

Accounts receivable

Accounts receivable refers to the amounts to be received within a short period from customers upon the sale of goods and services on account. In other words, accounts receivable are amounts customers owe to the business. Accounts receivable is an asset of a business.

Bad debt expense:

Bad debt expense is an expense account. The amounts of loss incurred from extending credit to the customers are recorded as bad debt expense. In other words, the estimated uncollectible accounts receivable are known as bad debt expense.

Direct write-off method:

This method does not make allowance or estimation for uncollectible accounts, instead this method directly write-off the actual uncollectible accounts by debiting bad debt expense and by crediting accounts receivable. Under this method, accounts would be written off only when the receivables from a customer remain uncollectible.

Allowance method:

It is a method for accounting bad debt expense, where amount of uncollectible accounts receivables are estimated and recorded at the end of particular period. Under this method, bad debts expenses are estimated and recorded prior to the occurrence of actual bad debt, in compliance with matching principle by using the allowance for doubtful account.

Two methods to estimate uncollectible accounts under allowance method are:

- Percentage of sales method, and

- Analysis of receivables method.

Analysis of receivables method:

A method of determining the estimated uncollectible receivables based on the age of individual accounts receivable is known as analysis of receivables method. This method is otherwise known as aging of receivables method. Under analysis of receivables method, estimated bad debts would be treated as the desired adjusted balance for allowance for doubtful accounts.

To journalize: The transactions under direct write off method.

Answer to Problem 8.14EX

Journalize the transactions of Company S under direct write off method.

| Date | Particulars | Debit | Credit |

| June 8 | Bad debt expense | $8,440 | |

| Account receivable – Person KQ | $8,440 | ||

| (To record the write-off of uncollectible account receivable ) | |||

| August 14 | Cash | $3,000 | |

| Bad debt expense | $9,500 | ||

| Account receivable – Person RO | $12,500 | ||

| (To record the cash collection and write-off of remaining uncollectible account receivable ) | |||

| October 16 | Accounts receivable – Person KQ | $8,440 | |

| Bad debt expense | $8,440 | ||

| (The reinstate the account of Person KQ) | |||

| October 16 | Cash | $8,440 | |

| Accounts receivable – Person KQ | $8,440 | ||

| (To record collection of cash on account) | |||

| December 31 | Bad debt expense | $24,995 | |

| Account receivable – Person WD | $4,600 | ||

| Account receivable – Person GG | $3,600 | ||

| Account receivable – Person AK | $7,150 | ||

| Account receivable – Person SP | $2,975 | ||

| Account receivable – Person NS | $6,630 | ||

| (To record the write-off of uncollectible account receivable ) | |||

| December 31 | No entry is required | ||

Table (1)

Explanation of Solution

For June 8:

To record this write-off of uncollectible receivables under direct write-off method, bad debt expense must be recognized as well as increased, and accounts receivable must be decreased by $8,440. Hence,

- An increase in bad debt expense (decreases the stockholders’ equity accounts) is debited with $8,440, and

- A decrease in accounts receivable (asset account) is credited with $8,440.

For August 14:

To record the collection of cash on account, cash account must be increased and accounts receivable must be decreased by $3,000.

To record this write-off of uncollectible receivables under direct write-off method, bad debt expense must be recognized as well as increased, and accounts receivable must be decreased by $9,500. Hence,

- An increase in cash (asset account) is debited with $3,000

- An increase in bad debt expense (decreases the stockholders’ equity accounts) is debited with $9,500, and

- A decrease in accounts receivable (asset account) is credited with

For October 16:

On October 16, the company has recovered $8,440 from Person KQ in full, whose account is previously written off as uncollectible. Hence, company required reversing the entry, which is previously written off as uncollectible receivables. Hence,

- Accounts receivable (asset account) is debited to increase its balance by $8,440, and

- Bad debt expense (stockholders’ equity) is credited to decrease its balance by $8,440.

Now, the collection of cash on account, increases cash and decreases accounts receivable by $8,440, as company has collected its receivables. Hence,

- An increase in cash (asset account) is debited with $8,440, and

- A decrease in accounts receivable (asset account) is credited with $8,440.

For December 31:

To record this write-off of uncollectible receivables under direct write-off method, bad debt expense must be recognized as well as increased, and accounts receivable must be decreased. Hence,

- An increase in bad debt expense (decreases the stockholders’ equity accounts) is debited, and

- A decrease in accounts receivable (asset account) is credited.

Adjusting entry is not required under direct write off method, since this method used to write off the accounts receivable accounts only when it is determined to be worthless.

B.

To journalize: The transactions under allowance method (Aging analysis method).

Answer to Problem 8.14EX

Journalize the transactions of Company RT under allowance method.

| Date | Particulars | Debit | Credit |

| June 8 | Allowance for doubtful accounts | $8,440 | |

| Account receivable – Person KQ | $8,440 | ||

| (To record the write-off of uncollectible account receivable ) | |||

| August 14 | Cash | $3,000 | |

| Allowance for doubtful accounts | $9,500 | ||

| Account receivable – Person RO | $12,500 | ||

| (To record the cash collection and write-off of remaining uncollectible account receivable ) | |||

| October 16 | Accounts receivable – Person KQ | $8,440 | |

| Allowance for doubtful accounts | $8,440 | ||

| (The reinstate the account of Person S) | |||

| October 16 | Cash | $8,440 | |

| Accounts receivable – Person KQ | $8,440 | ||

| (To record collection of cash on account) | |||

| December 31 | Allowance for doubtful accounts | $24,955 | |

| Account receivable – Person WD | $4,600 | ||

| Account receivable – Person GG | $3,600 | ||

| Account receivable – Person AK | $7,150 | ||

| Account receivable – Person SP | $2,975 | ||

| Account receivable – Person NS | $6,630 | ||

| (To record the write-off of uncollectible account receivable ) | |||

| December 31 | Bad debt expense (1) | $45,545 | |

| Allowance for doubtful accounts | $45,545 | ||

| (To adjust the allowance for doubtful accounts) | |||

Table (2)

Explanation of Solution

Working note:

Estimate the balance of the allowance for doubtful accounts as of December 31 using aging schedule.

| Age interval | Balance | Estimated uncollectible accounts | |

| Percent | Amount | ||

| 1-30 days past due | $320,000 | 1% | $3,200 |

| 31-60 days past due | $110,000 | 3% | $3,300 |

| 61-90 days past due | $24,000 | 10% | $2,400 |

| 91-120 days past due | $18,000 | 33% | $5,940 |

| More than 120 days | $43,000 | 75% | $32,250 |

| Total | $515,000 | $47,090 | |

Table (3)

The aging of accounts receivable indicates that the total estimated allowance for doubtful accounts as of December 31 is $47,090.

Prepare T-account for allowance for doubtful accounts to determine the unadjusted balance of allowance account.

| Allowance for doubtful accounts | |||||

| Date | Particulars | Debit | Date | Particulars | Credit |

| June 8 | Accounts receivable | $8,440 | January 1 | Beginning balance | $36,000 |

| August 14 | Accounts receivable | $9,500 | October 16 | Accounts receivable | $8,440 |

| December 31 | Accounts receivable | $24,955 | |||

| Total | $42,895 | Total | $44,440 | ||

| Ending balance | $1,545 | ||||

Table (4)

Now, calculate the amount of bad debt expense to be recorded in adjusting entry.

For June 8:

To record this write-off of uncollectible receivables under allowance method, both allowance for doubtful accounts and accounts receivable must be decreased by $8,440. Hence,

- A decrease in Allowance for doubtful accounts (contra-asset accounts) is debited with $8,440.

- A decrease in accounts receivable (asset account) is credited with $8,440.

For August 14:

To record the collection of cash on account, cash account must be increased and accounts receivable must be decreased by $3,000.

To record this write-off of uncollectible receivables under allowance method, both allowance for doubtful accounts and accounts receivable must be decreased by $9,500. Hence,

- An increase in cash (asset account) is debited with $3,000,

- A decrease in Allowance for doubtful accounts (contra-asset accounts) is debited with $9,500, and

- A decrease in accounts receivable (asset account) is credited with

For October 16:

On October 16, Company RT has recovered $8,440 from Person KQ in full, whose account is previously written off as uncollectible. Hence, company should reverse the entry, which is previously written off as uncollectible receivables. Hence,

- Accounts receivable (asset account) is debited to increase its balance by $8,440, and

- Allowance for doubtful accounts (contra-asset account) is credited to increase its balance by $8,440.

Now, the collection of cash on account, increases cash and decreases accounts receivable by $8,440, as company has collected its receivables. Hence,

- An increase in cash (asset account) is debited with $8,440, and

- A decrease in accounts receivable (asset account) is credited with $8,440.

For December 31:

To record this write-off of uncollectible receivables under allowance method, both allowance for doubtful accounts and accounts receivable must be decreased.

- A decrease in Allowance for doubtful accounts (contra-asset accounts) is debited and,

- A decrease in accounts receivable (asset account) is credited.

Adjusting entry is required at the end of the year, under allowance method. Aging receivables method is followed; hence estimated bad debts would be treated as ending balance of allowance account. Allowance for doubtful accounts (contra asset account) normal balance is a credit balance, it is calculated and determined that the unadjusted balance of Allowance for doubtful accounts as of December 31 is a credit of $1,545. It is calculated that total estimated allowance for doubtful accounts as of December 31 is $47,090. Hence, to bring the allowance for doubtful account balance from a credit of $1,545 to a credit of $47,090, it is required to increase bad debt expense and allowance for doubtful accounts by $45,545.

Hence, an increase in bad debt expense (decrease in stockholders’ equity account) is debited with $45,545 and an increase in allowance for doubtful accounts (contra asset account) is credited with $$45,545.

C.

Answer to Problem 8.14EX

Determine whether net income of Company RT is higher or lower under the direct-write off method than allowance method.

| Bad debt expense under: | Amount |

| Allowance method (1) | $45,545 |

| Direct-write off method | $34,445 |

| Difference | $11,090 |

Table (5)

Bad debt expense under allowance method is higher than direct write-off method. Increase in expense decreases the net income. Hence, Company RT’s net income would have been higher under the direct write off method than the allowance method by $11,090.

Explanation of Solution

Working note:

Prepare T-account for bad debt expense account (for direct write off method).

| Bad debt expense account | |||||

| Date | Particulars | Debit | Date | Particulars | Credit |

| June 8 | Accounts receivable | $8,840 | October 16 | Accounts receivable | $8,440 |

| August 14 | Accounts receivable | $9,500 | |||

| December 31 | Accounts receivable | $24,955 | |||

| Total | $42,895 | Total | $8,440 | ||

| Ending balance | $34,445 | ||||

Table (6)

Want to see more full solutions like this?

Chapter 8 Solutions

Bundle: Financial & Managerial Accounting, 14th + Working Papers for Warren/Reeve/Duchac's Corporate Financial Accounting, 14th + Working Papers, ... & Managerial Accounting, 14th + CengageNOWv2,

Additional Business Textbook Solutions

Operations Management: Processes and Supply Chains (12th Edition) (What's New in Operations Management)

Financial Accounting, Student Value Edition (5th Edition)

Intermediate Accounting (2nd Edition)

Understanding Business

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Principles of Operations Management: Sustainability and Supply Chain Management (10th Edition)

- What is the interest expensearrow_forwardWant solution to this financial accounting questionarrow_forwardOn January 1, 2011 we started a new business by investing cash of $10,000 and equipment of $9,000. During the year, we withdraw $2,000. When we prepare of Statement of Owners Equity, we note a final balance of $21,000. Based on this information, what was out net income or loss for the year? a. $4,000 net loss b. $2,000 net income c. $2,000 net loss d. $4,000 net incomearrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning