Videos

1.

To prepare:

A table and to allocate the cost.

1.

Explanation of Solution

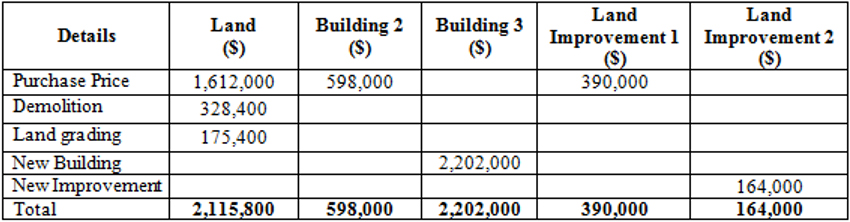

Prepare table to show allocation of cost:

Table (1)

Working Notes:

Computation of total appraised value:

Total appraised value is $2,800,000.

Land

Computation of percentage of land of the total appraised value:

Percentage of land is 62%.

Apportioned cost

Computation of apportioned cost:

Apportioned cost of land is $1,612,000.

Building

Computation of percentage of building of the total appraised value:

Percentage of building is 23%.

Apportioned cost

Apportioned cost of building is $598,000.

Land Improvements 1

Computation of percentage of land improvements 1 of the total appraised value:

Percentage of land improvement 1 is 15%.

Apportioned cost

Computation of apportioned cost:

Apportioned cost of land improvement 1 is $390,000.

2.

To prepare:

2.

Explanation of Solution

Record the entry for purchase of assets.

| Date | Account Title and Explanation | Post ref | Debit ($) |

Credit ($) |

|---|---|---|---|---|

| Jan1 | Land | 2,115,800 | ||

| Building 2 | 598,000 | |||

| Building 3 | 2,202,000 | |||

| Land improvements 1 | 390,000 | |||

| Land improvements 2 | 164,000 | |||

| Cash | 5,469,800 | |||

| (To record the purchase of assets) |

Table (2)

• Building is an asset account. Building account increases as the new building has been purchased. Hence, the Building account is debited.

• Land is an asset account. Land account increases as a new land is purchased and all the assets are debited as a new asset is purchased or if its value increases.

• Vehicle account is an asset account. Vehicles account increases as a new vehicle is purchased and all the assets are debited as a new asset is purchased or if its value increases.

• Land improvements are an asset account. Land improvement account increases as some improvements have been done on land to increase its useful life and all the assets are debited as their value increases.

• Cash account is an asset account. Cash account decreases as the amount paid for the purchase of all assets are made in cash and all the assets are credited as their values decreases.

3.

To prepare:

3.

Explanation of Solution

Building 2

Record

| Date | Account Title and Explanation | Post ref | Debit ($) |

Credit ($) |

|---|---|---|---|---|

| Depreciation | 26,900 | |||

| 26,900 | ||||

| (To record the depreciation) |

Table (3)

• Depreciation is an expense account. Depreciation account increases the balance of expense account and all the losses and expenses accounts are debited.

• Accumulated Depreciation account is a contra asset account. Accumulated depreciation has a credit balance and is increasing as the depreciation is transferred to this account. This is the reason it is credited.

Working Notes:

Computation of depreciation:

Depreciation that will charge to building is $26,900.

Building 3

Record entry for depreciation on building 3

| Date | Account Title and Explanation | Post ref | Debit ($) |

Credit ($) |

|---|---|---|---|---|

| Depreciation | 72,400 | |||

| Accumulated Depreciation | 72,400 | |||

| (To record the depreciation) |

Table (4)

• Depreciation is an expense account. Depreciation account increases the balance of expense account and all the losses and expenses accounts are debited.

• Accumulated Depreciation account is a contra asset account. Accumulated depreciation has a credit balance and is increasing as the depreciation is transferred to this account. This is the reason it is credited.

Working Notes:

Computation of depreciation:

Depreciation that will charge to building 3 is $72,400.

Land improvement 1

To record entry for depreciation on Land improvement 1,

| Date | Account Title and Explanation | Post ref | Debit ($) |

Credit ($) |

|---|---|---|---|---|

| Depreciation | 32,500 | |||

| Accumulated Depreciation | 32,500 | |||

| (To record the depreciation) |

Table (5)

• Depreciation is an expense account. Depreciation account increases the balance of expense account and all the losses and expenses accounts are debited.

• Accumulated Depreciation account is a contra asset account. Accumulated depreciation has a credit balance and is increasing as the depreciation is transferred to this account. This is the reason it is credited.

Working Notes:

Computation of depreciation:

Depreciation charged to improvement 1 $32,500.

Land improvement 2

To record entry for depreciation on Land improvement 2,

| Date | Account Title and Explanation | Post ref | Debit ($) |

Credit ($) |

|---|---|---|---|---|

| Depreciation | 8,200 | |||

| Accumulated Depreciation | 8,200 | |||

| (To record the depreciation) |

Table (6)

• Depreciation is an expense account. Depreciation account increases the balance of expense account and all the losses and expenses accounts are debited.

• Accumulated Depreciation account is a contra asset account. Accumulated depreciation has a credit balance and is increasing as the depreciation is transferred to this account. This is the reason it is credited.

Working Notes:

Computation of depreciation:

Depreciation that will charge to improvement 2 is $8200.

Want to see more full solutions like this?

Chapter 8 Solutions

Connect 2 Semester Access Card for Financial and Managerial Accounting

- Novak Company has the following stockholders' equity accounts at December 31, 2025. Common Stock ($100 par value, authorized 7,600 shares) $459,100 Retained Earnings 266,700 a. Prepare entries in journal form to record the following transactions, which took place during 2026 1. 290 shares of outstanding stock were purchased at $97 per share. (These are to be accounted for using the cost method.) 2. A $22 per share cash dividend was declared. 3. The dividend declared in (2) above was paid. 4. The treasury shares purchased in (1) above were resold at $101 per share. 5. 500 shares of outstanding stock were purchased at $103 per share. 6. 380 of the shares purchased in (5) above were resold at $96 per share. b. Prepare the stockholders' equity section of Novak Company's balance sheet after giving effect to these transactions, assuming that the net income for 2026 was $86,300. State law requires restriction of retained earnings for the amount of treasury stock.arrow_forwardResearch and Explain the current academic qualifications and relevant experience requirements, for tax agents to be to be registered under the Tax Agent Services Regulations 2009. (150 words)arrow_forwardDon't use aiarrow_forward

- What characterizes the faithful representation principle in accounting ?arrow_forwardNovak Company has the following stockholders' equity accounts at December 31, 2025. Common Stock ($100 par value, authorized 7,600 shares) $459,100 Retained Earnings 266,700 a. Prepare entries in journal form to record the following transactions, which took place during 2026 1. 290 shares of outstanding stock were purchased at $97 per share. (These are to be accounted for using the cost method.) 2. A $22 per share cash dividend was declared. 3. The dividend declared in (2) above was paid. 4. The treasury shares purchased in (1) above were resold at $101 per share. 5. 500 shares of outstanding stock were purchased at $103 per share. 6. 380 of the shares purchased in (5) above were resold at $96 per share. b. Prepare the stockholders' equity section of Novak Company's balance sheet after giving effect to these transactions, assuming that the net income for 2026 was $86,300. State law requires restriction of retained earnings for the amount of treasury stock.arrow_forwardAssignment Financial Accountingarrow_forward

- Sub: financial accountingarrow_forwardCalculate the present value of the lease .arrow_forwardQuestion 1. Pearl Leasing Company agrees to lease equipment to Martinez Corporation on January 1, 2025. The following information relates to the lease agreement. 1. The term of the lease is 7 years with no renewal option, and the machinery has an estimated economic life of 9 years. 2 The cost of the machinery is $541,000, and the fair value of the asset on January 1, 2025, is $760,000. 3. At the end of the lease term, the asset reverts to the lessor and has a guaranteed residual value of $45,000, Martinez estimates that the expected residual value at the end of the lease term will be $45,000. Martinez amortizes all of its leased equipment on a straight-line basis. 4. The lease agreement requires equal annual rental payments, beginning on January 1, 2025. 5. The collectibility of the lease payments is probable. 6. Pearl desires a 10% rate of return on its investments. Martinez's incremental borrowing rate is 11%, and the lessor's implicit rate is unknown. Annual rental payment is…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education