Inventory Valuation You are engaged in an audit of Roche Mfg. Company for the year ended December 31, 2019. To reduce the workload at year-end, Roche took its annual physical inventory under your observation on November 30, 2019. Roche’s inventory account, which includes raw materials and work in process, is on a perpetual basis, and it uses the first-in, first-out method of pricing. It has no finished goods inventory. The company’s physical inventory revealed that the book inventory of $60,570 was understated by $3,000. To avoid distorting the interim financial statements, Roche decided not to adjust the book inventory until year-end except for obsolete inventory items. Your audit revealed this information about the November 30 inventory: Pricing tests showed that the physical inventory was overpriced by $2,200. Footing and extension errors resulted in a $150 understatement of the physical inventory. Direct labor included in the physical inventory amounted to $10,000. Overhead was included at the rate of 200% of direct labor. You determined that the amount of direct labor was correct and the overhead rate was proper. The physical inventory included obsolete materials recorded at $250. During December, these materials were removed from the inventory account by a charge to cost of sales. Your audit also disclosed the following information about the December 31, 2019, inventory. Total debits to certain accounts during December are: The cost of sales of $68,600 included direct labor of $13,800. Normal scrap loss on established product lines is negligible. However, a special order started and completed during December had excessive scrap loss of $800 which was charged to Manufacturing Overhead Expense. Required: 1. Compute the correct amount of the physical inventory at November 30, 2019. 2. Without prejudice to your solution to Requirement 1, assume that the correct amount of the inventory at November 30, 2019, was $57,700. Compute the amount of the inventory at December 31,2019.

Inventory Valuation You are engaged in an audit of Roche Mfg. Company for the year ended December 31, 2019. To reduce the workload at year-end, Roche took its annual physical inventory under your observation on November 30, 2019. Roche’s inventory account, which includes raw materials and work in process, is on a perpetual basis, and it uses the first-in, first-out method of pricing. It has no finished goods inventory. The company’s physical inventory revealed that the book inventory of $60,570 was understated by $3,000. To avoid distorting the interim financial statements, Roche decided not to adjust the book inventory until year-end except for obsolete inventory items. Your audit revealed this information about the November 30 inventory: Pricing tests showed that the physical inventory was overpriced by $2,200. Footing and extension errors resulted in a $150 understatement of the physical inventory. Direct labor included in the physical inventory amounted to $10,000. Overhead was included at the rate of 200% of direct labor. You determined that the amount of direct labor was correct and the overhead rate was proper. The physical inventory included obsolete materials recorded at $250. During December, these materials were removed from the inventory account by a charge to cost of sales. Your audit also disclosed the following information about the December 31, 2019, inventory. Total debits to certain accounts during December are: The cost of sales of $68,600 included direct labor of $13,800. Normal scrap loss on established product lines is negligible. However, a special order started and completed during December had excessive scrap loss of $800 which was charged to Manufacturing Overhead Expense. Required: 1. Compute the correct amount of the physical inventory at November 30, 2019. 2. Without prejudice to your solution to Requirement 1, assume that the correct amount of the inventory at November 30, 2019, was $57,700. Compute the amount of the inventory at December 31,2019.

Solution Summary: The author calculates the correct amount of inventory on November 30, 2019 based on Company RM's First-in-First-Out method.

Inventory Valuation You are engaged in an audit of Roche Mfg. Company for the year ended December 31, 2019. To reduce the workload at year-end, Roche took its annual physical inventory under your observation on November 30, 2019. Roche’s inventory account, which includes raw materials and work in process, is on a perpetual basis, and it uses the first-in, first-out method of pricing. It has no finished goods inventory. The company’s physical inventory revealed that the book inventory of $60,570 was understated by $3,000. To avoid distorting the interim financial statements, Roche decided not to adjust the book inventory until year-end except for obsolete inventory items. Your audit revealed this information about the November 30 inventory:

Pricing tests showed that the physical inventory was overpriced by $2,200.

Footing and extension errors resulted in a $150 understatement of the physical inventory.

Direct labor included in the physical inventory amounted to $10,000. Overhead was included at the rate of 200% of direct labor. You determined that the amount of direct labor was correct and the overhead rate was proper.

The physical inventory included obsolete materials recorded at $250. During December, these materials were removed from the inventory account by a charge to cost of sales.

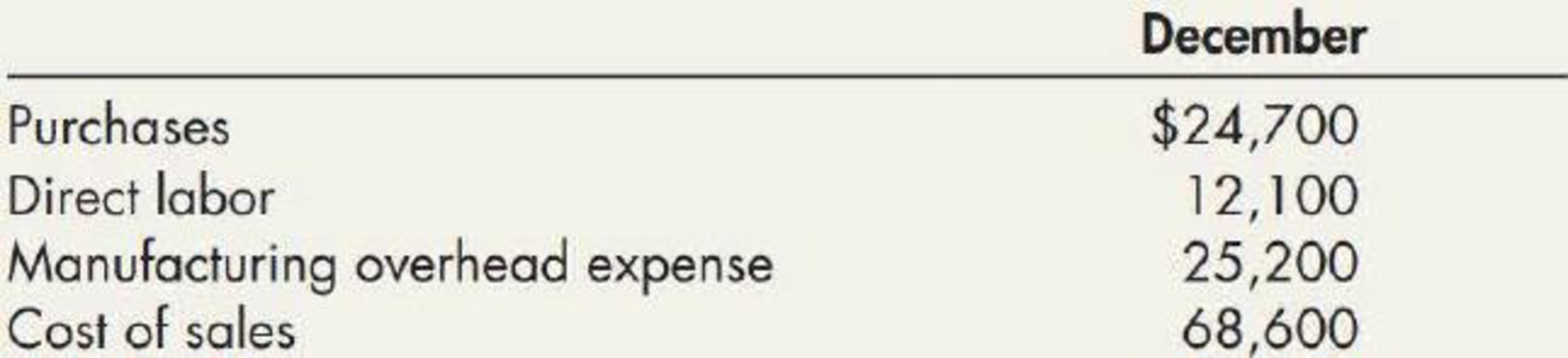

Your audit also disclosed the following information about the December 31, 2019, inventory.

Total debits to certain accounts during December are:

The cost of sales of $68,600 included direct labor of $13,800.

Normal scrap loss on established product lines is negligible. However, a special order started and completed during December had excessive scrap loss of $800 which was charged to Manufacturing Overhead Expense.

Required:

1. Compute the correct amount of the physical inventory at November 30, 2019.

2. Without prejudice to your solution to Requirement 1, assume that the correct amount of the inventory at November 30, 2019, was $57,700. Compute the amount of the inventory at December 31,2019.

Definition Definition Accounting practice that allows a business to determine the monetary value of any unsold inventory.

What is the plant wide overhead rate on these financial accounting question?

prepare an income statement for delray manufacturing (a manufacturer)assume that its cost of goods manufactured is $1,247,000

On 10/6/2024, company A sells goods to Customer C for €20,000 with an agreed credit of two months. On 31/12/2024, in the context of investigating the collectability of its receivables, the company estimates that it will only collect €10,000 from customer C and forms a provision for doubtful debts for the remaining amount. Finally, on 30/3/2025, company A receives from customer C the amount of: a. €9,000 b. €11,000.

You are requested to comment on the impact of the above collection cases a. 9000 b. 11,000 on the income statement for fiscal year 2025, justifying your position.

Chapter 7 Solutions

Intermediate Accounting: Reporting and Analysis - With Access

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning

Auditing: A Risk Based-Approach (MindTap Course L...AccountingISBN:9781337619455Author:Karla M Johnstone, Audrey A. Gramling, Larry E. RittenbergPublisher:Cengage Learning