Individual Income Taxes

43rd Edition

ISBN: 9780357109731

Author: Hoffman

Publisher: CENGAGE LEARNING - CONSIGNMENT

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 6, Problem 38P

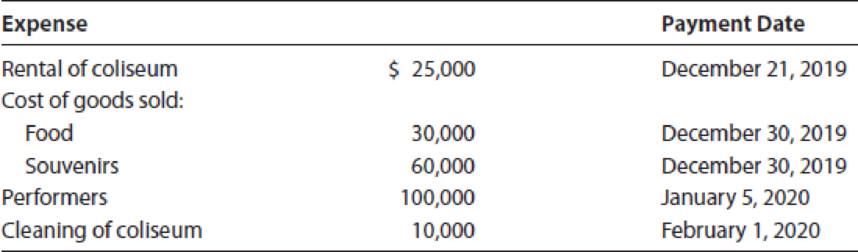

Duck, an accrual basis corporation, sponsored a rock concert on December 29, 2019. Gross receipts were $300,000. The following expenses were incurred and paid as indicated:

Because the coliseum was not scheduled to be used again until January 15, the company with which Duck had contracted did not perform the cleanup until January 8–10, 2020.

- a. Calculate Duck’s net income from the concert for tax purposes for 2019.

- b. Using the present value tables in Appendix H, what is the true cost to Duck if it had to defer the $100,000 deduction for the performers until 2020? Assume a 5% discount rate and a 21% marginal tax rate in 2019 and 2020.

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

What characterizes modified unit attribution in cost structures? (a) Complexity adds no value (b) Cost drivers reflect multi-level operational relationships (c) Attribution remains constant (d) Single drivers explain all costs. MCQ

I need assistance with this general accounting question using appropriate principles.

What is the ending total asset balance?

Chapter 6 Solutions

Individual Income Taxes

Ch. 6 - Prob. 1DQCh. 6 - Prob. 2DQCh. 6 - Classify each of the following expenditures paid...Ch. 6 - Prob. 4DQCh. 6 - Prob. 5DQCh. 6 - Prob. 6DQCh. 6 - Prob. 7DQCh. 6 - Prob. 8DQCh. 6 - Prob. 9DQCh. 6 - Prob. 10DQ

Ch. 6 - Prob. 11DQCh. 6 - Prob. 12DQCh. 6 - Prob. 13DQCh. 6 - Prob. 14DQCh. 6 - Linda operates an illegal gambling operation....Ch. 6 - Prob. 16DQCh. 6 - Melissa, the owner of a sole proprietorship, does...Ch. 6 - Prob. 18DQCh. 6 - Blaze operates a restaurant in Cleveland. He...Ch. 6 - Prob. 20DQCh. 6 - Prob. 21DQCh. 6 - Ray loses his job as a result of a corporate...Ch. 6 - Lavinia incurs various legal fees in obtaining a...Ch. 6 - Prob. 24DQCh. 6 - Prob. 25DQCh. 6 - Shanna, a calendar year and cash basis taxpayer,...Ch. 6 - Prob. 27CECh. 6 - Maud, a calendar year taxpayer, is the owner of a...Ch. 6 - Vella owns and operates an illegal gambling...Ch. 6 - Printer Company pays a 25,000 annual membership...Ch. 6 - Stanford owns and operates two dry cleaning...Ch. 6 - Tobias has a brokerage account and buys on the...Ch. 6 - Prob. 33PCh. 6 - Prob. 34PCh. 6 - Janice, age 32, earns 50,000 working in 2019. She...Ch. 6 - Prob. 36PCh. 6 - Prob. 37PCh. 6 - Duck, an accrual basis corporation, sponsored a...Ch. 6 - Prob. 39PCh. 6 - Prob. 40PCh. 6 - Prob. 41PCh. 6 - Prob. 42PCh. 6 - Terry traveled to a neighboring state to...Ch. 6 - Prob. 44PCh. 6 - Prob. 45PCh. 6 - Prob. 46PCh. 6 - Prob. 47PCh. 6 - Prob. 48PCh. 6 - Prob. 49PCh. 6 - Prob. 50PCh. 6 - Prob. 51PCh. 6 - Brittany Callihan sold stock (basis of 184,000) to...Ch. 6 - Prob. 53PCh. 6 - Prob. 54PCh. 6 - Prob. 55PCh. 6 - Prob. 56PCh. 6 - Prob. 57CPCh. 6 - Prob. 58CPCh. 6 - Prob. 1RPCh. 6 - Prob. 2RPCh. 6 - Prob. 3RPCh. 6 - Which of the following is a deduction for AGI? a....Ch. 6 - Which of the following is not a deduction for AGI?...Ch. 6 - David is a CPA and enjoys playing the lottery....Ch. 6 - Prob. 4CPACh. 6 - Prob. 5CPACh. 6 - Prob. 6CPA

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Aspen Components produces electronic parts with a unit selling price of $28. The company incurs variable costs of $16.50 per unit and has annual fixed costs of $690,000. The company has the capacity to produce 120,000 units annually but is currently operating at 70% capacity. A special order has been received for 15,000 units at a price of $19.75 per unit. If Aspen accepts this special order, should it produce these units as a one-time special order? What would be the impact on the company's profit?arrow_forwardgeneral accounting question using accurate calculation methods?arrow_forwardPlease provide the correct answer to this financial accounting problem using accurate calculations.arrow_forward

- What is the estimated overhead cost if 180 direct labor hours are expected to be used in the upcoming period?arrow_forwardI need help finding the accurate solution to this general accounting problem with valid methods.arrow_forwardCan you solve this general accounting problem using appropriate accounting principles?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Individual Income Taxes

Accounting

ISBN:9780357109731

Author:Hoffman

Publisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Depreciation -MACRS; Author: Ronald Moy, Ph.D., CFA, CFP;https://www.youtube.com/watch?v=jsf7NCnkAmk;License: Standard Youtube License