Videos

INTEREST RATE DETERMINATION AND YIELD CURVES

a. What effect would each of the following events likely have on the level of nominal interest rates?

- 1. Households dramatically increase their savings rate.

- 2. Corporations increase their demand for funds following an increase in investment opportunities.

- 3. The government runs a larger-than-expected budget deficit.

- 4. There is an increase in expected inflation.

b. Suppose you are considering two possible investment opportunities: a 12-year Treasury bond and a 7-year, A-rated corporate bond. The current real risk-free rate is 4%; and inflation is expected to be 2% for the next 2 years, 3% for the following 4 years, and 4% thereafter. The maturity risk premium is estimated by this formula: MRP = 0 02(t − 1)%. The liquidity premium (LP) for the corporate bond is estimated to be 0.3%. You may determine the default risk premium (DRP), given the company’s bond rating, from the table below. Remember to subtract the bond’s LP from the corporate spread given in the table to arrive at the bond’s DRP. What yield would you predict for each of these two investments?

| Rate | Corporate Bond Yield Spread = DRP + LP | ||

| U.S. Treasury | 0.83% | ---- | |

| AAA corporate | 0.93 | 0.10% | |

| AA corporate | 1.29 | 0.46 | |

| A corporate | 1.67 | 0.84 | |

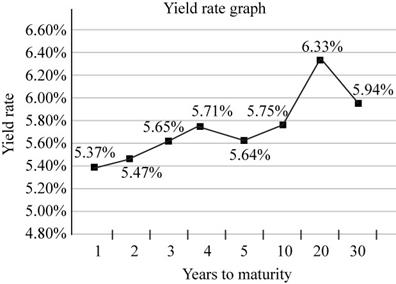

c. Given the following Treasury bond yield information, construct a graph of the yield curve.

| Maturity | Yield |

| 1 year | 5.37% |

| 2 years | 5.47 |

| 3 years | 5.65 |

| 4 years | 5.71 |

| 5 years | 5.64 |

| 10 years | 5.75 |

| 20 years | 6.33 |

| 30 years | 5.94 |

d. Based on the information about the corporate bond provided in part b, calculate yields and then construct a new yield curve graph that shows both the Treasury and the corporate bonds.

e. Which part of the yield curve (the left side or right side) is likely to be most volatile over time?

f. Using the Treasury yield information in part c, calculate the following rates using geometric averages:

- 1. The 1-year rate 1 year from now

- 2. The 5-year rate 5 years from now

- 3. The 10-year rate 10 years from now

- 4. The 10-year rate 20 years from now

a. (1)

To identify: The effect of given events on the nominal interest rate.

Nominal Rate:

An interest rate which is agreed and paid such as the borrower is ready to pay and the lender is ready to receive the money is known as the nominal interest rate.

Answer to Problem 20SP

The increment in the rates of savings account of households leads to increase in nominal interest rate as the households get good returns from treasury bills or bonds the nominal rate would increase.

Explanation of Solution

- The increase ininterest rate of savings account of the households resultsto increase the demand for the funds.

- To offer the good returns to households lead to increase in demand forinvestment in a savings account and the returns of Treasury securities where the household invest their money would also increase.

Hence, if the households would increase the interest rates to get more investment it will lead to increase in nominal rate.

(2)

To identify: The effect of given events on the nominal interest rate.

Nominal Rate:

An interest rate which is agreed and paid such as the borrower is ready to pay and the lender is ready to receive the money is known as the nominal interest rate.

Answer to Problem 20SP

The corporations increase the rates to increase the demand of their funds which leads to increase in nominal rate.

Explanation of Solution

- The corporations require fund for their business and to increase the demand for the product.

- Increase in demand of the product leads to increase in nominal interest rate.

Hence, the increase in nominal rate would result in the increase in demand of the funds of corporations.

3.

To identify: The effect of given events on the nominal interest rate.

Nominal Rate:

An interest rate which is agreed and paid such as the borrower is ready to pay and the lender is ready to receive the money is known as the nominal interest rate.

Answer to Problem 20SP

Solution:

The larger-than-expected budget leads to increase in nominal interest rate.

Explanation of Solution

- The larger-than-expected budget refers the negative condition of the budget of government.

- To make the balance of budget, the governmentwould issue the investment securities and increase the interest on that and nominal rates would increase.

Hence, the larger deficit of the budget leads to increase in nominal rate as the government issues the securities to raise fund.

4.

To identify: The effect of given events on the nominal interest rate.

Nominal Rate:

An interest rate which is agreed and paid such as the borrower is ready to pay and the lender is ready to receive the money is known as the nominal interest rate.

Answer to Problem 20SP

Increase in interest rate leads to increase rate as it is included in nominal rate.

Explanation of Solution

- Inflation refers to the condition when the price of the goods and commodity increase and the purchasing power parity would also increase.

- The interest rates of the investments avenues include the inflation rate in it.

Hence, the increase in inflation positively leads to increase in nominal interest rate.

b.

To compute: The expected yield for 12-year Treasury bond and 7-year A-rated corporate bond.

Yield:

Yield is the percentage of the securities at which the return is provided by the company to its investors. Yield can be there in the form of dividend and interest.

Explanation of Solution

Compute the yield for the 12-years treasury bonds.

The risk-free rate is 4%. (Given)

The inflation premium is 3.33%. (Calculated in working note)

The maturity risk premium is 0.22%. (Calculated in working note)

The formula to calculate the yield on treasury bonds,

Where,

-

-

-

- MRP is maturity risk premium.

Substitute 4% for

The yield on 12-year treasury bonds is 7.55%.

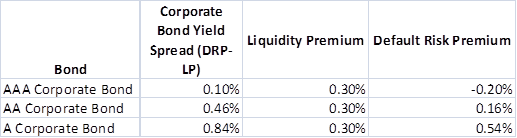

Compute the default risk premium on a corporate bond,

Table (1)

Compute the yield for AAA Corporate bond.

The risk-free rate is 4%. (Given)

The liquidity premium and default risk premium is 0.10%. (Given)

The inflation premium is 2.86%. (Calculated in working note)

The maturity risk premium is 0.12%. (Calculated in working note)

The formula to calculate the yield,

Where,

-

-

-

- MRP is maturity risk premium.

- DRP is default risk premium.

- LP is the liquidity premium.

Substitute 4% for

The yield on 7-year AAA corporate bond is 7.08%.

Compute the yield for AA Corporate bond.

The risk-free rate is 4%. (Given)

Default risk premium and liquidity premium is 0.46%. (Given)

The inflation premium is 2.86%. (Calculated in working note)

The maturity risk premium is 0.12%. (Calculated in working note)

The formula to calculate the yield,

Where,

-

-

-

- MRP is maturity risk premium.

- DRP is default risk premium.

- LP is liquidity premium.

Substitute 4% for

The yield on 7-year AA corporate bond is 7.44%.

Compute the yield for A Corporate bond.

The risk-free rate is 4%. (Given)

Default risk premium and liquidity premium is 0.84%. (Given)

The inflation premium is 2.86%. (Calculated in working note)

The maturity risk premium is 0.12%. (Calculated in working note)

The formula to calculate the yield,

Where,

-

-

-

- MRP is maturity risk premium.

- DRP is default risk premium.

- LP is liquidity premium.

Substitute 4% for

The yield on 7-year A corporate bond is 7.82%.

Working note:

Treasury bond calculations:

Computation of inflation premium on 12-years treasury bonds,

Computation of the maturity risk premium,

7-years bond calculations:

Computation of the inflation premium,

Computation of the maturity risk premium,

Hence,the default risk premiums of AAA corporate bond, AA corporate bond, and A corporate bond, are (0.20%), 0.16% and 0.54% respectively. The expected yield of 12-yearTreasury bond is 7.55%, AAA corporate bond is 7.08%, AA corporate bond is 7.44% and A corporate bond is 7.82%.

c.

To prepare: A yield curve chart for given information.

Yield Curve:

The graphical representation of the expected return, provided by the company to its investors during the years is known as the yield curve.

Answer to Problem 20SP

The yield curve chart

Fig 1

Explanation of Solution

- The x-axis shows the number of years.

- The y-axis shows years to maturity.

- The graph shows the expected yield with their respective years.

- The yield curve is sloping upwards and is increasing until the 20th year and then it slopes downward.

The yield curve chart for the given information is as mentioned above.

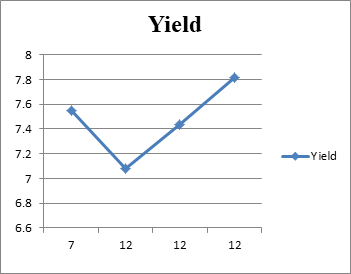

d.

To draw: The yield curve chart.

Answer to Problem 20SP

Statement to show the relative yields, calculated in part b.

| Bond | Expected Yield |

| 12-year Treasury Bond | 7.55% |

| 7-year AAA Corporate Bond | 7.08% |

| 7-year AA Corporate Bond | 7.44% |

| 7-year A Corporate Bond | 7.82% |

Table (2)

The yield to maturity graph:

Fig 2

Explanation of Solution

- The x-axis shows the number of years.

- The y-axis shows years to maturity.

- The graph shows the expected yield with their respective years.

- The yield curve shows a downward slope up to 12 years.

- The curve then shows an upward slope and continues to increase.

Thus, the yield curve chart is shown as above.

e.

To identify: The side of a yield curve which would be more volatile.

Answer to Problem 20SP

Solution:

The right side of the yield curve would be more volatile as an increase in the maturity increases the yield of the bond.

Explanation of Solution

- The yield curve represents the yield of relative bonds with their respective years.

- The yield increase towards the right as the year of maturity increases and more volatile from the right side.

Hence, the right side of the yieldcurve is more volatile than the left side.

f. (1)

To identify: The rates for the following statements.

Explanation of Solution

Given,

The yield for 2 years is 5.47%.

The yield for 1 year is 5.37%.

The formula to compute the rate,

Substitute 0.0547 for yield for year 2, 0.0537 for yield for year 1, 1 for a number of years and 1 for years from now.

The rate is 5.57%.

Hence, the rate of 1-year, 1 year from now is 5.57%.

2.

To identify: The rates for the following statements.

Explanation of Solution

Given,

The yield for 10 years is 5.75%.

The yield for 5years is 5.64%.

The formula to compute the rate,

Substitute 0.0575 for yield for year 10, 0.0564 for yield for year 5, 5 for a number of years and 5 for years from now.

Take root to bothsides.

The rate is 5.86%.

Hence, the rate of 5-year, 5 years from now is 5.86%.

3.

To identify: The rates for the following statements.

Explanation of Solution

Given,

The yield for 20 years is 6.33%.

The yield for 10years is 5.75%.

The formula to compute the rate,

Substitute 0.0633 for yield for year 20, 0.0575 for yield for year 10, 10 for a number of years and 10 for years from now.

Take root to bothsides.

The rate is 6.91%.

Hence, the rate of 10-year, 10 years from now is 6.91%.

4.

To identify: The rates for the following statements.

Explanation of Solution

Given,

The yield for 30 years is 5.94%.

The yield for 20 years is 6.33%.

The formula to compute the rate,

Substitute 0.0633 for yield for year 20, 0.0594 for yield for year 30, 10 for a number of years and 20 for years from now.

Take root to bothsides.

The rate is 5.61%.

Hence, the rate of 10-year, 20 years from now is 5.61%.

Want to see more full solutions like this?

Chapter 6 Solutions

EP FUNDAMENTALS OF FIN.MGMT.-MINDTAP

- How can the book value still serve as a useful metric for investors despite the dominance of market value?arrow_forwardHow do you think companies can practically ensure that stakeholder interests are genuinely considered, while still prioritizing the financial goal of maximizing shareholder equity? Do you think there’s a way to measure and track this balance effectively?arrow_forward$5,000 received each year for five years on the first day of each year if your investments pay 6 percent compounded annually. $5,000 received each quarter for five years on the first day of each quarter if your investments pay 6 percent compounded quarterly. Can you show me either by hand or using a financial calculator please.arrow_forward

- Can you solve these questions on a financial calculator: $5,000 received each year for five years on the last day of each year if your investments pay 6 percent compounded annually. $5,000 received each quarter for five years on the last day of each quarter if your investments pay 6 percent compounded quarterly.arrow_forwardNow suppose Elijah offers a discount on subsequent rooms for each house, such that he charges $40 for his frist room, $35 for his second, and $25 for each room thereafter. Assume 30% of his clients have only one room cleaned, 25% have two rooms cleaned, 30% have three rooms cleaned, and the remaining 15% have four rooms cleaned. How many houses will he have to clean before breaking even? If taxes are 25% of profits, how many rooms will he have to clean before making $15,000 profit? Answer the question by making a CVP worksheet similar to the depreciation sheets. Make sure it works well, uses cell references and functions/formulas when appropriate, and looks nice.arrow_forward1. Answer the following and cite references. • what is the whole overview of Green Markets (Regional or Sectoral Stock Markets)? • what is the green energy equities, green bonds, and green financing and how is this related in Green Markets (Regional or Sectoral Stock Markets)? Give a detailed explanation of each of them.arrow_forward

- Could you help explain “How an exploratory case study could be goodness of work that is pleasing to the Lord?”arrow_forwardWhat are the case study types and could you help explain and make an applicable example.What are the 4 primary case study designs/structures (formats)?arrow_forwardThe Fortune Company is considering a new investment. Financial projections for the investment are tabulated below. The corporate tax rate is 24 percent. Assume all sales revenue is received in cash, all operating costs and income taxes are paid in cash, and all cash flows occur at the end of the year. All net working capital is recovered at the end of the project. Year 0 Year 1 Year 2 Year 3 Year 4 Investment $ 28,000 Sales revenue $ 14,500 $ 15,000 $ 15,500 $ 12,500 Operating costs 3,100 3,200 3,300 2,500 Depreciation 7,000 7,000 7,000 7,000 Net working capital spending 340 390 440 340 ?arrow_forward

- What are the six types of alternative case study compositional structures (formats)used for research purposes, such as: 1. Linear-Analytical, 2. Comparative, 3. Chronological, 4. Theory Building, 5. Suspense and 6. Unsequenced. Please explainarrow_forwardFor an operating lease, substantially all the risks and rewards of ownership remain with the _________. QuestFor an operating lease, substantially all the risks and rewards of ownership remain with the _________: A) Tenant b) Lessee lessor none of the above tenant lessee lessor none of the aboveLeasing allows the _________ to acquire the use of a needed asset without having to make the large up-front payment that purchase agreements require Question 4 options: lessor lessee landlord none of the abovearrow_forwardHow has AirBnb negatively affected the US and global economy? How has Airbnb negatively affected the real estate market? How has Airbnb negatively affected homeowners and renters market? What happened to Airbnb in the Tax Dispute in Italy?arrow_forward

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT