Concept explainers

Videos

Comprehensive Receivables Problem Blackmon Corporation’s December 31, 2018,

*The company has a recourse liability of $700 related to a note receivable sold to a bank.

During 2019, credit sales (terms, n/EOM) totaled $2,200,000, and collections on

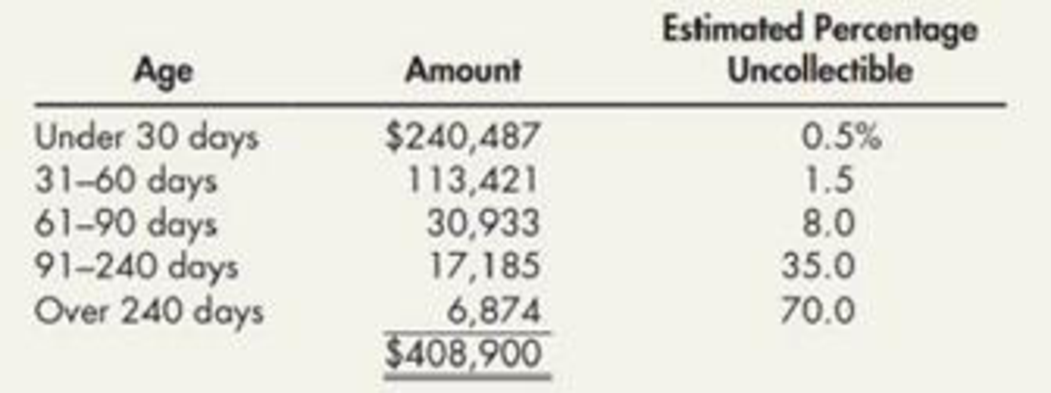

On December 31, 2019, an aging of the accounts receivable balance indicated the following:

Required:

- 1. Prepare the

journal entries to record the preceding receivable transactions during 2019 and the necessaryadjusting entry on December 31, 2019. Assume a 360-day year for interest calculations and round calculations to the nearest dollar. - 2. Prepare the receivables portion of Blackmon’s December 31, 2019, balance sheet.

- 3. Next Level Compute Blackmon’s accounts receivable turnover in days, assuming a 360-day business year. What is your evaluation of its collection policies?

- 4. If Blackmon uses IFRS, what might be the heading of the section for the receivables reported in Requirement 2?

1.

Journalize the entries to record the previous receivables transaction and prepare the necessary adjusting entry on December 31, 2019.

Explanation of Solution

Accounts receivable:

Accounts receivable refers to the amounts to be received within a short period from customers upon the sale of goods and services on account. In other words, accounts receivable are amounts customers owe to the business. Accounts receivable is an asset of a business.

Prepare journal entries:

| Date | Account Title and Explanation | Debit | Credit |

| Accounts receivable | $2,200,000 | ||

| Sales revenue | $2,200,000 | ||

| (To record the sale on credit) |

Table (1)

| Date | Account Title and Explanation | Debit | Credit |

| Cash | $1,900,000 | ||

| Accounts receivable | $1,900,000 | ||

| ( To record payment received) |

Table (2)

| Date | Account Title and Explanation | Debit | Credit |

| Allowance for doubtful accounts | $18,000 | ||

| Accounts receivable | $18,000 | ||

| (To record accounts receivables written- off) |

Table (3)

| Date | Account Title and Explanation | Debit | Credit |

| Accounts receivable | $1,350 | ||

| Allowance for doubtful accounts | $1,350 | ||

| (To record accounts receivables written- off) |

Table (4)

| Date | Account Title and Explanation | Debit | Credit |

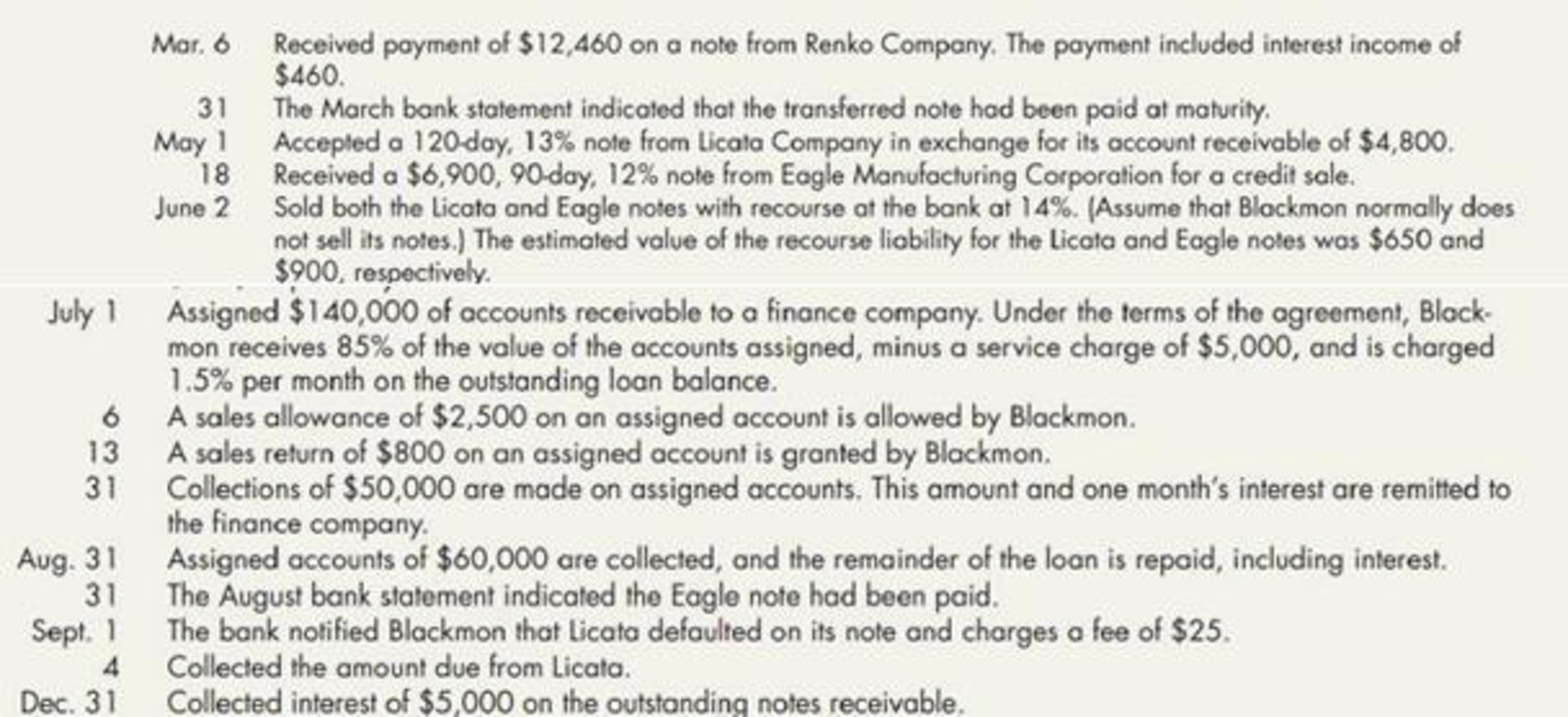

| March 6 | Cash | $1,350 | |

| Accounts receivable | $1,350 | ||

| (To record cash collected on accounts) |

Table (5)

| Date | Account Title and Explanation | Debit | Credit |

| March 6 | Cash | $12,460 | |

| Notes receivable | $12,000 | ||

| Interest income | $460 | ||

| (To record the cash collected from notes receivable along with interest) |

Table (6)

| Date | Account Title and Explanation | Debit | Credit |

| March 31 | Recourse liability | $700 | |

| Gain from sale of note | $700 | ||

| (To record the fair value of recourse liability) |

Table (7)

| Date | Account Title and Explanation | Debit | Credit |

| May 1 | Notes Receivable | $4,800 | |

| Accounts receivable | $4,800 | ||

| (To record the notes receivable) |

Table (8)

| Date | Account Title and Explanation | Debit | Credit |

| May 18 | Notes receivable | $6,900 | |

| Sales revenue | $6,900 | ||

| (To record the receipt of the interest bearing note) |

Table (10)

| Date | Account Title and Explanation | Debit | Credit |

| June 2 | Cash | $11,736 | |

|

Loss from sale of receivable | $1,603 | ||

| Notes receivable | $11,700 | ||

| Interest income | $89.97 | ||

| Recourse liability | $1,550 | ||

| (To record the factoring of accounts receivable) |

Table (11)

Note: For the values of amount refer to Table (26) and Table (27)

| Date | Account Title and Explanation | Debit | Credit |

| July 1 | Cash (balancing figure) | $114,000 | |

| Assignment service charge expense | $5,000 | ||

| Notes payable (11) | $119,000 | ||

| (To record the assignment service charge expense) |

Table (12)

| Date | Account Title and Explanation | Debit | Credit |

| July 1 | Accounts receivable assigned | 140,000 | |

| Accounts receivables | 140,000 | ||

| ( To record the remaining accounts owed) |

Table (13)

| Date | Account Title and Explanation | Debit | Credit |

| July 6 | Return liability | 2,500 | |

| Accounts receivable assigned | 2,500 | ||

| (To record the return liability of accounts receivable assigned) |

Table (14)

| Date | Account Title and Explanation | Debit | Credit |

| July 13 | Return liability | 800 | |

| Accounts receivable assigned | 800 | ||

| (To record the return liability of accounts receivable assigned) |

Table (15)

| Date | Account Title and Explanation | Debit | Credit |

| July 31 | Cash | 50,000 | |

| Accounts receivable assigned | 50,000 | ||

| (To record the receipt of accounts receivable assigned) |

Table (16)

| Date | Account Title and Explanation | Debit | Credit |

| July 31 | Notes payable | 50,000 | |

| Interest expense (12) | 1,785 | ||

| Cash | 51,785 | ||

| (To record the interest expense on notes payable) |

Table (17)

| Date | Account Title and Explanation | Debit | Credit |

| August 31 | Cash | 60,000 | |

| Accounts receivable assigned | 60,000 | ||

| (To record the receipt of cash) |

Table (18)

| Date | Account Title and Explanation | Debit | Credit |

| August 31 | Notes payable (15) | 69,000 | |

| Interest expense (13) | 1,035 | ||

| Cash | 70,035 | ||

| (To record the interest expense on notes payable) |

Table (19)

| Date | Account Title and Explanation | Debit | Credit |

| August 31 | Accounts receivable | 26,700 | |

| Accounts receivable assigned | 26,700 | ||

| (To record the accounts receivable assigned) |

Table (20)

Note:

| Date | Account Title and Explanation | Debit | Credit |

| August 31 | Recourse liability | 900 | |

| Gain from sale of notes | 900 | ||

| (To record the fair value of recourse liability) |

Table (21)

| Date | Account Title and Explanation | Debit | Credit |

| September 1 | Notes receivable dishonored | 4,383 | |

| Recourse liability | 650 | ||

| Cash (14) | 5,033 | ||

| (To record the notes dishonored) |

Table (22)

| Date | Account Title and Explanation | Debit | Credit |

| September 4 | Cash (14) | 5,033 | |

| Notes receivables dishonored | 4,383 | ||

| Gain from collection of dishonored note | 650 | ||

| (To record the ) |

Table (23)

| Date | Account Title and Explanation | Debit | Credit |

| December 31 | Cash | 5,000 | |

| Interest income | 5,000 | ||

| (To record the interest income) |

Table (24)

| Date | Account Title and Explanation | Debit | Credit |

| December 31 |

Bad debt expense | 17,855 | |

| Allowance for doubtful accounts | 17,855 | ||

| (To record the bad debt expenses of the period) |

Table (25)

Working note:

(1) Calculate the amount of loss from receivable:

| Particulars | Amount ($) |

| Face value of the note | 4,800 |

| Interest to maturity (2) | 208 |

| Maturity value of note | 5,008 |

| Less: Discount (3) | (171.38) |

| Proceeds | 4,836.62 |

| Less: Book value of note (4) | (4,855.47) |

| Recourse liability | (650) |

| Loss from sale of receivable | (668.85) |

Table (26)

(2) Calculate the interest to maturity:

(3) Calculate the amount of discount:

Note: 88 days is calculated by subtracting 120 days from 32 days (May 1 to June 2).

(4) Calculate the book value of note:

(5) Calculate accrued interest income:

Note: 20 days is calculated from November 1 to November 20.

(6) Calculate the amount of loss from receivable of Company E:

| Particulars | Amount ($) |

| Face value of the note | 6,900 |

| Interest to maturity (7) | 207 |

| Maturity value of note | 7,107 |

| Less: Discount (8) | (207.29) |

| Proceeds | 6,899.71 |

| Less: Book value of note (9) | (6,934.50) |

| Recourse liability | (900) |

| Loss from sale of receivable | (934.79) |

Table (27)

(7) Calculate the interest to maturity:

(8) Calculate the amount of discount:

Note: 75 days is calculated by subtracting 90 days from 15 days (May 18 to June 2).

(9) Calculate the book value of note:

(10) Calculate accrued interest income:

Note: 20 days is calculated from November 1 to November 20.

(11) Calculate the advance amount of accounts receivable:

(12) Calculate the amount of interest expense on July 31:

(13) Calculate the interest expense on August 31:

(14) Calculate the amount of cash on September 1:

(15) Calculate the amount of cash on August 1:

2.

Prepare the receivable portion of Company B as on December 31, 2019.

Explanation of Solution

Receivables portion of Company B is prepared as follows:

| Particulars | Amount | Amount |

| Accounts receivables (16) | $408,900 | |

| Less: Allowance for doubtful accounts (16) | ($16,205) | |

| $392,695 | ||

| Notes receivables | $38,000 | |

| Total receivables | $430,695 |

Table (28)

Working note:

(16) Calculate the estimated total amount of uncollectible:

| Age | Amount (a) | Estimated Percentage uncollectible (b) | Estimated amount of uncollectible |

| Under 30 days | $240.487 | 0.5% | 1,202 |

| 30–60 days | $113,421 | 1.5% | 1,701 |

| 61–90 days | $30,933 | 8.0% | 2,475 |

| 91–240 days | $17,185 | 35% | 6,015 |

| Over 240 days | $6,874 | 70% | 4,812 |

| $408,900 | $16,205 |

Table (29)

3.

Calculate the accounts receivable turnover in days and analyze its collection policy.

Explanation of Solution

Accounts receivable turnover:

Accounts receivable turnover is a liquidity measure of accounts receivable in times, which is calculated by dividing the net credit sales by the average amount of net accounts receivables. In other words, it indicates the number of times the average amount of net accounts receivables collected during a particular period.

Average collection period:

Average collection period indicates the number of days taken by a business to collect its outstanding amount of accounts receivable on an average.

Calculate the receivables turnover in days:

The receivables turnover in days for Corporation B is 51 days and it seems to be slow, therefore, the company must be very violent in its collection policies.

Working note:

(17) Compute the receivables turnover ratio:

(18) Calculate average accounts receivable (net):

4.

State the heading for the accounts receivable section in requirement 2, if Company B uses IFRS.

Explanation of Solution

“Loans and Receivables” can be used as the heading for the accounts receivables section, if Company B uses IFRS.

Want to see more full solutions like this?

Chapter 6 Solutions

Intermediate Accounting: Reporting And Analysis

- Assume that none of the fixed overhead can be avoided. However, if the robots are purchased from Tienh Inc., Crane can use the released productive resources to generate additional income of $375,000. (Enter negative amounts using either a negative sign preceding the number e.g. -45 or parentheses e.g. (45).) Direct materials Direct labor Variable overhead 1A Fixed overhead Opportunity cost Purchase price Totals Make A Buy $ SA Net Income Increase (Decrease) $ Based on the above assumptions, indicate whether the offer should be accepted or rejected? The offerarrow_forwardThe following is a list of balances relating to Phiri Properties Ltd during 2024. The company maintains a memorandum debtors and creditors ledger in which the individual account of customers and suppliers are maintained. These were as follows: Debit balance in debtors account 01/01/2024 66,300 Credit balance in creditors account 01/01/2024 50,600 Sunday credit balance on debtors ledger Goods purchased on credit 724 257,919 Goods sold on credit Cash received from debtors Cash paid to suppliers Discount received Discount allowed Cash purchases Cash sales Bad Debts written off Interest on overdue account of customers 323,614 299,149 210,522 2,663 2,930 3,627 5,922 3,651 277 Returns outwards 2,926 Return inwards 2,805 Accounts settled by contra between debtors and creditors ledgers 1,106 Credit balances in debtors ledgers 31/12/2024. 815 Debit balances in creditors ledger 31/12/2024.698 Required: Prepare the debtors control account as at 31/12/2024. Prepare the creditors control account…arrow_forwardSolnarrow_forward

- incoporate the accounting conceptual frameworksarrow_forwarda) Define research methodology in the context of accounting theory and discuss the importance of selecting appropriate research methodology. Evaluate the strengths and limitations of quantitative and qualitative approaches in accounting research. b) Assess the role of modern accounting theories in guiding research in accounting. Discuss how contemporary theories, such as stakeholder theory, legitimacy theory, and behavioral accounting theory, shape research questions, hypotheses formulation, and empirical analysis. Question 4 Critically analyse the role of financial reporting in investment decision-making, emphasizing the qualitative characteristics that enhance the usefulness of financial statements. Discuss how financial reporting influences both investor confidence and regulatory decisions, using relevant examples.arrow_forwardFastarrow_forward

- Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning