Horngren's Financial & Managerial Accounting (5th Edition)

5th Edition

ISBN: 9780133866292

Author: Tracie L. Miller-Nobles, Brenda L. Mattison, Ella Mae Matsumura

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 5, Problem 5.37AP

A Preparing a multi-step income statement and journalizing closing entries

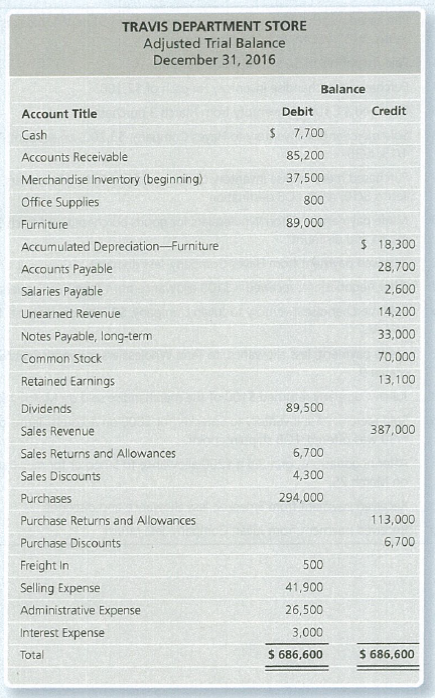

Travis Department Store uses a periodic inventory system. The adjusted

Requirements

1. Prepare Travis Department Store’s multi-step income statement for the year ended December 31, 2016. Assume ending Merchandise Inventory is $36,500.

2. Journalize Travis Department Store’s dosing entries.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Damerly Company (a Utah employer) wants to give a holiday bonus check of $375 to each employee. As it wants the check amount to be $375, it will need to gross-up the amount of the bonus. Calculate the withholding taxes and the gross amount of the bonus to be made to John Rolen if his cumulative earnings for the year are $46,910. Besides being subject to social security taxes and federal income tax (supplemental rate), a 4.95% Utah income tax must be withheld on supplemental payments.

Please given correct answer general Accounting

Hii ticher please given correct answer general Accounting

Chapter 5 Solutions

Horngren's Financial & Managerial Accounting (5th Edition)

Ch. 5 - Which account does a merchandiser use that a...Ch. 5 - The two main inventory accounting systems are the...Ch. 5 - The journal entry for the purchase of inventory on...Ch. 5 - JC Manufacturing purchase d inventory for 5,300...Ch. 5 - Prob. 5QCCh. 5 - Suppose Daves Discounts Merchandise Inventory...Ch. 5 - Which of the following accounts would be closed at...Ch. 5 - What is the order of the subtotals that appear on...Ch. 5 - Prob. 9QCCh. 5 - The journal entry for the purchase of inventory on...

Ch. 5 - What is a merchandiser, and what is the name of...Ch. 5 - Prob. 2RQCh. 5 - Describe the operating cycle of a merchandiser.Ch. 5 - What is Cost of Goods Sold (COGS), and where is it...Ch. 5 - How is gross profit calculated, and what does it...Ch. 5 - What are the two types of inventory accounting...Ch. 5 - What is an invoice?Ch. 5 - What account is debited when recording a purchase...Ch. 5 - Prob. 9RQCh. 5 - What is a purchase return? How does a purchase...Ch. 5 - Prob. 11RQCh. 5 - How is the net cost of inventory calculated?Ch. 5 - What are the two journal entries involved when...Ch. 5 - When granting a sales allowance, is there a return...Ch. 5 - Prob. 15RQCh. 5 - Prob. 16RQCh. 5 - Prob. 17RQCh. 5 - What are the four steps involved in the closing...Ch. 5 - Prob. 19RQCh. 5 - Prob. 20RQCh. 5 - Prob. 21RQCh. 5 - Prob. 22RQCh. 5 - Prob. 23ARQCh. 5 - When recording purchase returns and purchase...Ch. 5 - What account is debited when recording the payment...Ch. 5 - Prob. 26ARQCh. 5 - Is an adjusting entry needed for inventory...Ch. 5 - Highlight the differences in the closing process...Ch. 5 - Describe the calculation of cost of goods sold...Ch. 5 - Comparing periodic and perpetual inventory systems...Ch. 5 - Journalizing purchase transactions Consider the...Ch. 5 - Journalizing purchase transactions Consider the...Ch. 5 - Journalizing sales transactions Journalize the...Ch. 5 - Journalizing purchase and sales transactions...Ch. 5 - Adjusting for inventory shrinkage Carlas...Ch. 5 - Journalizing closing entries Rockwall RV Centers...Ch. 5 - Use the following information to answer Short...Ch. 5 - Use the following information to answer Short...Ch. 5 - Computing the gross profit percentage Morris...Ch. 5 - Journalizing purchase transactions-periodic...Ch. 5 - Prob. 5.12SECh. 5 - Journalizing closing entries-periodic inventory...Ch. 5 - Computing cost of goods sold in a periodic...Ch. 5 - For all exercises, assume the perpetual inventory...Ch. 5 - Journalizing purchase transactions from an invoice...Ch. 5 - Journalizing purchase transactions Hartford...Ch. 5 - Computing missing amounts Consider the following...Ch. 5 - Journalizing sales transactions Journalize the...Ch. 5 - Journalizing purchase and sales transactions...Ch. 5 - Journalizing adjusting entries and computing gross...Ch. 5 - Use the following information to answer Exercises...Ch. 5 - Prob. 5.23ECh. 5 - Use the following information to answer Exercises...Ch. 5 - Computing the gross profit percentage Cupcake...Ch. 5 - Journalizing purchase transactionsperiodic...Ch. 5 - Journalizing sales transactions-periodic inventory...Ch. 5 - Journalizing purchase and sales...Ch. 5 - Journalizing dosing entries-periodic inventory...Ch. 5 - Computing cost of goods sold in a periodic...Ch. 5 - Journalizing purchase and sale transactions...Ch. 5 - Journalizing purchase and sale transactions...Ch. 5 - Preparing a multi-step income statement,...Ch. 5 - Journalizing adjusting entries, preparing adjusted...Ch. 5 - Preparing a single-step income statement,...Ch. 5 - Journalizing purchase and sale...Ch. 5 - A Preparing a multi-step income statement and...Ch. 5 - Journalizing purchase and sale transactions...Ch. 5 - Prob. 5.39BPCh. 5 - Prob. 5.40BPCh. 5 - Journalizing adjusting entries, preparing adjusted...Ch. 5 - Prob. 5.42BPCh. 5 - Prob. 5.43BPCh. 5 - Preparing a multi-step income statement and...Ch. 5 - Journalizing purchase and sale transactions,...Ch. 5 - Journalizing purchase and sale transactions,...Ch. 5 - Comprehensive Problem for Chapters 1-5 Completing...Ch. 5 - Prob. 5.1CTDCCh. 5 - Dobbs Wholesale Antiques makes all sales under...Ch. 5 - Rae Philippe was a warehouse manager for Atkins...Ch. 5 - Prob. 5.1CTFSC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- On a particular date, FedEx has a stock price of $89.27 and an EPS of $7.11. Its competitor, UPS, had an EPS of $0.38. What would be the expected price of UPS stock on this date, if estimated using the method of comparables? A) $4.77 B) $7.16 C) $9.54 D) $10.50arrow_forwardHow much will you accumulated after 35 year? General accountingarrow_forwardGiven correct answer general Accountingarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting

Accounting

ISBN:9781337272124

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial Accounting

Accounting

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...

Accounting

ISBN:9781305666160

Author:James A. Heintz, Robert W. Parry

Publisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...

Accounting

ISBN:9781305654174

Author:Gary A. Porter, Curtis L. Norton

Publisher:Cengage Learning

The accounting cycle; Author: Alanis Business academy;https://www.youtube.com/watch?v=XTspj8CtzPk;License: Standard YouTube License, CC-BY