Videos

Income (loss) recognition; Long-term contract; revenue recognition over time vs. upon project completion

• LO5–9

Brady Construction Company contracted to build an apartment complex for a price of $5,000,000. Construction began in 2018 and was completed in 2020. The following is a series of independent situations, numbered 1 through 6, involving differing costs for the project. All costs are stated in thousands of dollars.

Required:

Copy and complete the following table:

The revenue recognition principle

The revenue recognition principle refers to the revenue that should be recognized in the time period, when the performance obligation (sales or services) of the company is completed.

Revenue recognized point of long term contract

A long-term contract qualifies for revenue recognition over time. The seller can recognize the revenue as per percentage of the completion of the project, which is recognized as revenue minus cost of completion until date.

If a contract does not meet the performance obligation norm, then the seller cannot recognize the revenue till the project is complete.

To determine: The amount of gross profit or loss to be recognized under various situations.

Answer to Problem 5.21E

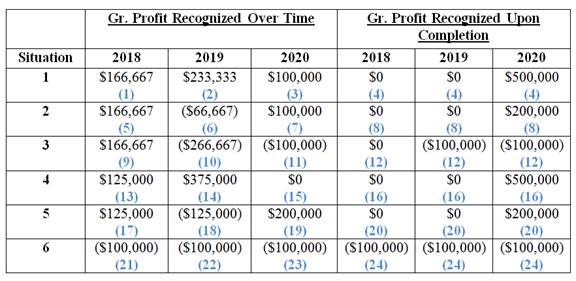

The amount of gross profit or loss to be recognized under various situations is as follows:

(Figure 1)

Explanation of Solution

Working note:

Situation – 1

1. Compute the value of gross profit or loss recognized over time

Here,

| Particulars | 2018 | 2019 | 2020 |

| Contract price (A) | $5,000,000 | $5,000,000 | $5,000,000 |

| Actual costs to date | 1,500,000 | 3,600,000 | 4,500,000 |

| Estimated costs to complete | 3,000,000 | 900,000 | 0 |

| Total estimated costs (B) | 4,500,000 | 4,500,000 | 4,500,000 |

| Estimated gross profit(actual in 2020)

|

$500,000 | $500,000 | $500,000 |

Table (1)

In the year 2018:

In the year 2019:

In the year 2020:

2. Compute the value of gross profit or loss recognized upon completion

| Year | Gross profit recognized |

| 2018 | 0 |

| 2019 | 0 |

| 2020 | $500,000 |

| Total gross profit | $500,000 |

Table (2)

(4)

Situation – 2

1. Compute the value of gross profit or loss recognized over time

Here,

| Particulars | 2018 | 2019 | 2020 |

| Contract price (A) | $5,000,000 | $5,000,000 | $5,000,000 |

| Actual costs to date | 1,500,000 | 2,400,000 | 4,800,000 |

| Estimated costs to complete | 3,000,000 | 2,400,000 | 0 |

| Total estimated costs (B) | 4,500,000 | 4,800,000 | 4,800,000 |

| Estimated gross profit(actual in 2020)

|

$500,000 | $200,000 | $200,000 |

Table (3)

In the year 2018:

In the year 2019:

In the year 2020:

2. Compute the value of gross profit or loss recognized upon completion

| Year | Gross profit recognized |

| 2018 | 0 |

| 2019 | 0 |

| 2020 | $200,000 |

| Total gross profit | $200,000 |

Table (4)

(8)

Situation – 3

1. Compute the value of gross profit or loss recognized over time

Here,

| Particulars | 2018 | 2019 | 2020 |

| Contract price (A) | $5,000,000 | $5,000,000 | $5,000,000 |

| Actual costs to date | 1,500,000 | 3,600,000 | 5,200,000 |

| Estimated costs to complete | 3,000,000 | 1,500,000 | 0 |

| Total estimated costs (B) | 4,500,000 | 5,100,000 | 5,200,000 |

| Estimated gross profit(actual in 2020)

|

$500,000 | $(100,000) | $(200,000) |

Table (5)

In the year 2018:

In the year 2019:

In the year 2020:

2. Compute the value of gross profit or loss recognized upon completion

| Year | Gross profit recognized |

| 2018 | 0 |

| 2019 | $(100,000) |

| 2020 | $(100,000) |

| Total gross profit | $(200,000) |

Table (6)

(12)

Situation – 4

1. Compute the value of gross profit or loss recognized over time

Here,

| Particulars | 2018 | 2019 | 2020 |

| Contract price (A) | $5,000,000 | $5,000,000 | $5,000,000 |

| Actual costs to date | 500,000 | 3,500,000 | 4,500,000 |

| Estimated costs to complete | 3,500,000 | 875,000 | 0 |

| Total estimated costs (B) | 4,000,000 | 4,375,000 | 4,500,000 |

| Estimated gross profit(actual in 2020)

|

$1,000,000 | $625,000 | $500,000 |

Table (7)

In the year 2018:

In the year 2019:

In the year 2020:

2. Compute the value of gross profit or loss recognized upon completion

| Year | Gross profit recognized |

| 2018 | 0 |

| 2019 | 0 |

| 2020 | $500,000 |

| Total gross profit | $500,000 |

Table (8)

(16)

Situation – 5

1. Compute the value of gross profit or loss recognized over time

Here,

| Particulars | 2018 | 2019 | 2020 |

| Contract price (A) | $5,000,000 | $5,000,000 | $5,000,000 |

| Actual costs to date | 500,000 | 3,500,000 | 4,800,000 |

| Estimated costs to complete | 3,500,000 | 1,500,000 | 0 |

| Total estimated costs (B) | 4,000,000 | 5,000,000 | 4,800,000 |

| Estimated gross profit(actual in 2020)

|

$1,000,000 | $0 | $200,000 |

Table (9)

In the year 2018:

In the year 2019:

In the year 2020:

2. Compute the value of gross profit or loss recognized upon completion

| Year | Gross profit recognized |

| 2018 | 0 |

| 2019 | 0 |

| 2020 | $200,000 |

| Total gross profit | $200,000 |

Table (10)

(20)

Situation – 6

1. Compute the value of gross profit or loss recognized over time

Here,

| Particulars | 2018 | 2019 | 2020 |

| Contract price (A) | $5,000,000 | $5,000,000 | $5,000,000 |

| Actual costs to date | 500,000 | 3,500,000 | 5,300,000 |

| Estimated costs to complete | 4,600,000 | 1,700,000 | 0 |

| Total estimated costs (B) | 5,100,000 | 5,200,000 | 5,300,000 |

| Estimated gross profit(actual in 2020)

|

$(100,000) | $(200,000) | $(300,000) |

Table (11)

In the year 2018:

In the year 2019:

In the year 2020:

2. Compute the value of gross profit or loss recognized upon completion

| Year | Gross profit recognized |

| 2018 | $(100,000) |

| 2019 | (100,000) |

| 2020 | (100,000) |

| Total gross profit | $(300,000) |

Table (12)

(24)

Want to see more full solutions like this?

Chapter 5 Solutions

INTERMEDIATE ACCOUNTING, W/CONNECT

- Can you solve this general accounting question with accurate accounting calculations?arrow_forwardRayburn Corporation has a building that it bought during year 0 for $850,000. It sold the building in year 5. During the time it held the building, Rayburn depreciated it by $100,000. What are the amount and character of the gain or loss Rayburn will recognize on the sale in each of the following alternative situations? Note: Loss amounts should be indicated by a minus sign. Enter NA if a situation is not applicable. Leave no answers blank. Enter zero if applicable. Problem 11-43 Part-a (Static) a. Rayburn receives $840,00arrow_forwardCan you solve this financial accounting question with the appropriate financial analysis techniques?arrow_forward

- I need the correct answer to this general accounting problem using the standard accounting approach.arrow_forwardFenton Manufacturing Inc. had a variable costing operating income of $128,400 in 2023. Ending inventory decreased during 2023 from 45,000 units to 40,000 units. During both 2022 and 2023, fixed manufacturing overhead was $1,080,000, and 135,000 units were produced. Determine the absorption costing operating income for 2023.arrow_forwardWhat are the total product Costs for the company under variable costing?arrow_forward

- I am searching for the accurate solution to this general accounting problem with the right approach.arrow_forwardI am searching for the correct answer to this general accounting problem with proper accounting rules.arrow_forwardPlease provide the correct answer to this general accounting problem using valid calculations.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education