Intermediate Financial Management (MindTap Course List)

13th Edition

ISBN: 9781337395083

Author: Eugene F. Brigham, Phillip R. Daves

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 5, Problem 3P

Black-Scholes Model

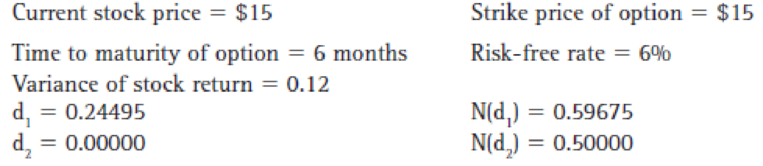

Assume that you have been given the following information on Purcell Industries call options:

According to the Black-Scholes option pricing model, what is the option’s value?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Identify the key parameters that influence option price. Discuss the impact of a rise and fall in the value of each parameter on the prices of put and call options.

a. Explain the covered call options strategy b. Graphically show a covered call options strategy, including payoff. Explain why an investor mayuse this option strategy.c. Using put-call parity, explain the shape of the payoff line (in part (a) of this question). Whatoption position does it look like and why?

Compare the binomial and Black-Scholes option pricing models. What are their differences and similarities? In what circumstances would you prefer one versus the other?

Use real market data as well as academic references.

Chapter 5 Solutions

Intermediate Financial Management (MindTap Course List)

Ch. 5 - Define each of the following terms:

Option; call...Ch. 5 - Prob. 2QCh. 5 - Prob. 3QCh. 5 - Prob. 1PCh. 5 - The exercise price on one of Flanagan Companys...Ch. 5 - Black-Scholes Model

Assume that you have been...Ch. 5 - Put–Call Parity

The current price of a stock is...Ch. 5 - Prob. 5PCh. 5 - Binomial Model The current price of a stock is 20....Ch. 5 - Prob. 7P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Assume that you have been given the following information on Purcell Corporations call options: According to the Black-Scholes option pricing model, what is the options value?arrow_forwardDefine each of the following terms: Option; call option; put option Exercise value; strike price Black-Scholes option pricing modelarrow_forwardCompare the binomial and Black-Scholes option pricing models. What are their differences and similarities? In what circumstances would you prefer one versus the other? Support your arguments using references.arrow_forward

- Describe about the Option-pricing models?arrow_forwardDiscuss the payoff structures for call and put options and the determinants of call and put option prices. Explain how the option pricing theory can be applied in credit risk modelling.arrow_forwardThe price level you choose for price protection on a call option is referred to as: A. The strike price B. The option premium C. The time value D. The intrinsic valuearrow_forward

- a) discuss the relationship between the up-factor (u), down-factor (d), risk-free rate (r), and binomial probability (p) in the binomial model. b) discuss the assumptions in Black-Scholes-Merton model (BSM) from memory. c) discuss the variables in the BSM formula and explain how they affect call option pricing. d) define historical volatility and implied volatility. e) demonstrate how to reduce risk with gamma hedging.arrow_forwardWhat impact does each of the followingparameters have on the value of a call option?(1) Current stock pricearrow_forwardReal Options & Game Theory: The value of a call option and a put option is influenced by the following variables: - Underlying asset value- Strike Price- Variance of Underlying asset- Time to Expiration What effect would an increase in each of these variables have on the value of a calloption and a put option?arrow_forward

- Describe the five variables (Assets price, Strick price or Exercise Price, Risk- Free- Rate, Time to Expiration, Volatility) that Black-Scholes-Merton Formula uses to calculate the price of call and put options. Explain how the change in these variables (Assets price, Strick price or Exercise Price, Risk- Free- Rate, Time to Expiration, Volatility) affects the price of the option.arrow_forwardDescribe Option-Pricing Theory.arrow_forwardExplain in detail with an example how the change of the variables (like Stock Price, Exercise Price, Risk-Free Rate, Volatility or Standard Deviation, and Time to Expiration) of Black-Scholes-Merton Formula affect the price of the option.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

Accounting for Derivatives Comprehensive Guide; Author: WallStreetMojo;https://www.youtube.com/watch?v=9D-0LoM4dy4;License: Standard YouTube License, CC-BY

Option Trading Basics-Simplest Explanation; Author: Sky View Trading;https://www.youtube.com/watch?v=joJ8mbwuYW8;License: Standard YouTube License, CC-BY