a.

Prepare the journal entries made by the parent to record the sale of the equipment to the subsidiary; and by the subsidiary to record the purchase and the [I] entries for the year of sale.

a.

Explanation of Solution

An acquisition of assets is the purchase of a corporation by purchasing its assets rather than its stock. An acquisition is when one company acquires most or all of the shares of another company to gain control over that company. An investment in equity is money which is invested in a company by buying that company's shares in the stock market. Typically, those shares are traded in a stock exchange.

The required

| Date | Account title and Explanation | Post Ref | Debit ($) | Credit ($) |

| Cash | ||||

| Equipment | ||||

| Gain on sale of Equipment | ||||

|

(To record the sale of equipment) |

Table (1)

The required journal entry recorded by the subsidiary is as follows:

| Date | Account title and Explanation | Post Ref | Debit ($) | Credit ($) |

| Equipment | ||||

| Cash | ||||

|

(To record the purchase of equipment) | ||||

| [Igain] Gain on sale of equipment | ||||

| Equipment | ||||

| Accumulated depreciation | ||||

| (To adjust Gain, Equipment, and Accumulated Depreciation on the date of the intercompany transfer of equipment) | ||||

| [Idep] Accumulated Depreciation | ||||

| Depreciation Expense | ||||

| (To eliminate the excess depreciation expense recorded by the subsidiary, and to adjust accumulated depreciation from the BOY amount to the EOY amount) |

Table (2)

Working notes:

In January of 2014, the parent sold Equipment to the subsidiary for a cash price of $128,700. The subsidiary retained the depreciation policy of the parent and depreciates the equipment over its remaining 10-year useful life.

Depreciation charged by the subsidiary on equipment is $128,700/10 i.e., $12,870

The parent had acquired the equipment at a cost of $124,800 and depreciated the equipment over its 12-year useful life using the straight-line method.

Depreciation charged by the parent on equipment is $124,800/12 i.e., $10,400

Calculate excess depreciation:

b.

Compute the remaining portion of the deferred gain on January 1, 2016.

b.

Explanation of Solution

In January of 2014, the parent sold Equipment to the subsidiary for a cash price of $128,700. The subsidiary retained the

Depreciation charged by the subsidiary on equipment is $128,700/10 i.e., $12,870

The parent had acquired the equipment at a cost of $124,800 and depreciated the equipment over its 12-year useful life using the straight-line method.

Depreciation charged by the parent on equipment is $124,800/12 i.e., $10,400

Calculate excess depreciation:

Operating expenses of the subsidiary is

Gain on the sale of equipment is

Through the BOY, two years have passed, so the deferred gain at the start of the current year is as follows:

Hence, the remaining portion of the deferred gain on Jan 1, 2016 is

c.

Compute the amount of netincome (loss) from subsidiary reported by the parent company for the year ended Dec 31,2016 assuming that the parent applied the equity method.

c.

Explanation of Solution

Equity income is money generated from stock dividends that investors can access by buying dividend-declared stocks or by buying funds that invest in dividend-declared stocks.

Subsidiary net income is

AAP Depreciation is

Deferred gain on intercompany sale is

The computation to yield the income (loss) from subsidiary reported by the parent company during2016is as follows:

| Particulars | Amount ($) |

| Subsidiary net income | |

| AAP Depreciation | |

| Deferred gain on intercompany sale | |

| Income (loss) from subsidiary |

Table (3)

Hence, the income (loss) from subsidiary is

d.

Compute the equity investment account balanceon Dec 31, 2016.

d.

Explanation of Solution

An investment in equity is money which is invested in a company by buying that company's shares in the stock market. Typically, those shares are traded in a stock exchange.

EOY

EOY Common stock of subsidiary is

Calculate EOY Unamortized AAP assets:

| Particulars | Amount ($) | Dep./Amort. | Amount |

| PPE, net | |||

| Patent | |||

| Goodwill | |||

| EOY AAP assets |

Table (4)

The computation to yield the Equity Investment balance on Dec 31, 2016 is as follows:

| Particulars | Amount ($) |

|

EOY subsidiary retained earnings | |

| EOY subsidiary common stock | |

| Add: Unamortized AAP @ EOY | |

| Less: Unconfirmed gain @ EOY | |

| EOY Equity investment balance |

Table (5)

Hence, the equity investment balance as on Dec 31, 2016is

e.

Prepare the consolidation entries for the year ended Dec 31, 2016.

e.

Explanation of Solution

Consolidated financial statements are a group of entities financial statements that are presented as those of a single economic entity. They are the financial statements of a group in which the parent company and its subsidiaries introduce their assets, liabilities, equity, revenue, expenses and

Consolidated accounting is used to club a parent company's financial information and one or more subsidiaries. The parent prepares consolidated financial statements through

The computation ofBOY [ADJ] for 2016 consolidation is as follows:

| Particulars | Amount ($) |

|

Change in retained earnings (S) thru BOY | |

| Cumulative AAP amort thru BOY | |

| Less: BOY Downstream Unconfirmed Asset | |

| ADJ Amount |

Table (6)

The required consolidation journal entries are as follows:

| Date | Account title and Explanation | Post Ref | Debit ($) | Credit ($) |

| [ADJ] BOY Equity Investment | ||||

| BOY Retained Earnings (P) | ||||

| [C] Income (loss) from subsidiary | ||||

| Dividends | ||||

| [E] Common Stock (S) @ BOY | ||||

| Retained Earnings (S) @BOY | ||||

| Equity Investment | ||||

| [A] PPE, net | ||||

| Patent | ||||

| Goodwill | ||||

| Equity Investment@ BOY | ||||

| [D Depreciation and Amort. expenses | ||||

| PPE, net | ||||

| Patent | ||||

|

(To record depreciation and amortization expense for the [A] assets) | ||||

| [Igain] Equity investment @BOY | ||||

| PPE, net | ||||

| [Idep] PPE, net | ||||

| Depreciation Expense |

Table (7)

f.

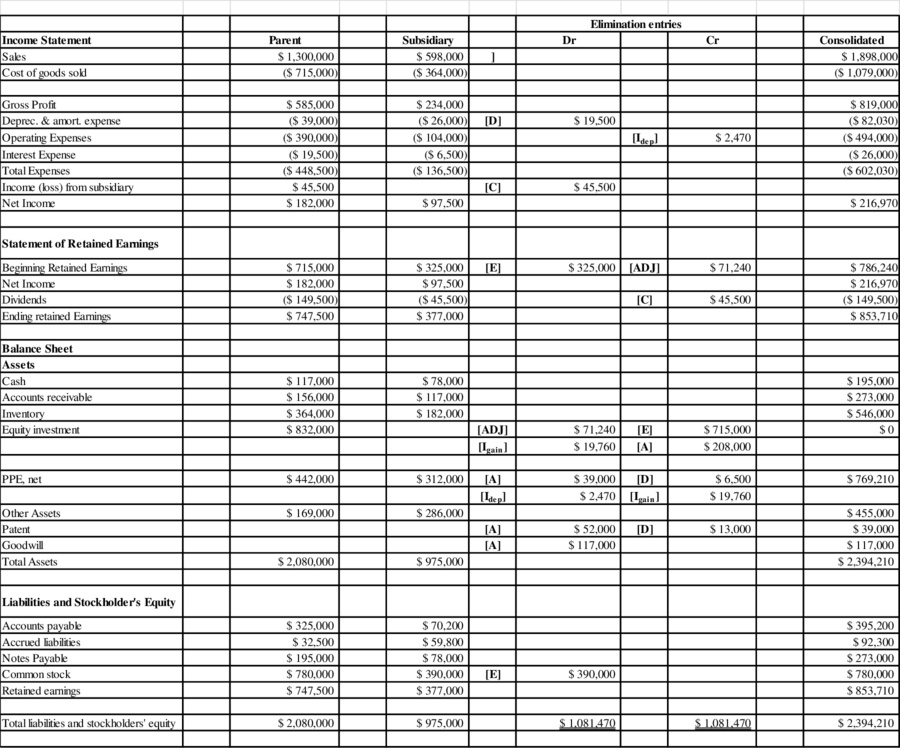

Prepare the consolidation spreadsheet for the year ended December 31, 2016.

f.

Explanation of Solution

Consolidated financial statements are a group of entities financial statements that are presented as those of a single economic entity. They are the financial statements of a group in which the parent company and its subsidiaries introduce their assets, liabilities, equity, revenue, expenses and cash flows as those of a single business organization.

A consolidated

Consolidation worksheet is an instrument used to prepare a parent's consolidated financial statements and their subsidiaries. It demonstrates the individual book values of companies, the adjustments and eliminations necessary, and the consolidated final values.

The consolidated spreadsheet for the year ended December 31, 2016 is shown below:

Table (8)

Want to see more full solutions like this?

Chapter 4 Solutions

ADVANCED ACCOUNTING

- Boston Supplies had cash sales of $78,450, credit sales of $45,670, sale returns and allowances of $6,890, and sales discounts of $3,750. What is the company's net sales for this period?arrow_forwardWhat is the company's net sales for this period?arrow_forwardWhat is the primary purpose of preparing a trial balance? a) To calculate net profit or lossb) To check the mathematical accuracy of the ledger accountsc) To prepare the income statementd) To report cash flowsarrow_forward

- Machinery was purchased for $78,500 on January 1, 2018. Shipping costs were $2,200 and installation expenses totaled $4,300. It is estimated that the machinery will have a $15,000 salvage value at the end of its 8-year useful life. What is the amount of accumulated depreciation on December 31, 2020, if the straight-line method of depreciation is used?arrow_forwardI am trying to find the accurate solution to this general accounting problem with appropriate explanations.arrow_forwardWhat is the primary goal of financial management?A) Maximizing profitsB) Maximizing shareholder wealthC) Minimizing costsD) Ensuring liquidityarrow_forward

- Which of the following is NOT an example of an operating activity in cash flow statement? a) Receipts from customersb) Payments to suppliersc) Proceeds from issuing sharesd) Payments to employeesarrow_forwardCan you solve this general accounting problem using accurate calculation methods?arrow_forwardPlease provide the answer to this general accounting question using the right approach.arrow_forward

- The accounting equation is:a) Assets + Liabilities = Equityb) Assets = Liabilities + Equityc) Liabilities = Assets + Equityd) Assets + Equity = Liabilitiesarrow_forwardGeneral Accountingarrow_forwardThe primary objective of financial accounting is to:a) Provide management with detailed reports for decision-making.b) Help the company save taxes.c) Provide financial information to external users.d) Track inventory levels. need help!arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education