Videos

Combat Fire, Inc. manufactures steel cylinders and nozzles for two models of fire extinguishers: (1) a home fire extinguisher and (2) a commercial fire extinguisher. The home model is a high-volume (54,000 units), half-gallon cylinder that holds 2 1/2 pounds of multi-purpose dry chemical at 480 PSI. The commercial model is a low-volume (10,200 units), two-gallon cylinder that holds 10 pounds of multi-purpose dry chemical at 390 PSI. Both products require 1.5 hours of direct labor for completion. Therefore, total annual

direct labor hours are 96,300 or [1.5 hours × (54,000 + 10,200)]. Expected annual manufacturing

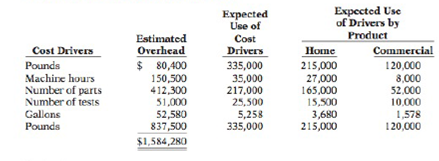

The company’s managers identified six activity cost pools and related cost drivers and accumulated overhead by cost pool as follow's.

Instructions

(a) Under traditional product costing, compute the total unit cost of each product. Prepare a simple comparative schedule of the individual costs by product (similar to Illustration 4-3 on page 137).

(b) Under ABC, prepare a schedule showing the computations of the activity-based overhead rates (per cost driver).

(c) Prepare a schedule assigning each activity's overhead cost pool to each product based on the use of cost drivers. (Include a computation of overhead cost per unit, rounding to the nearest cent.)

(d) Compute the total cost per unit for each product under ABC.

(e) Classify each of the activities as a value-added activity or a non-value-added activity.

(f) Comment on (1) the comparative overhead cost per unit for the two products under ABC. and (2) the comparative total costs per unit under traditional costing and ABC.

Want to see the full answer?

Check out a sample textbook solution

Chapter 4 Solutions

Managerial Accounting: Tools for Business Decision Making

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning