Concept explainers

Videos

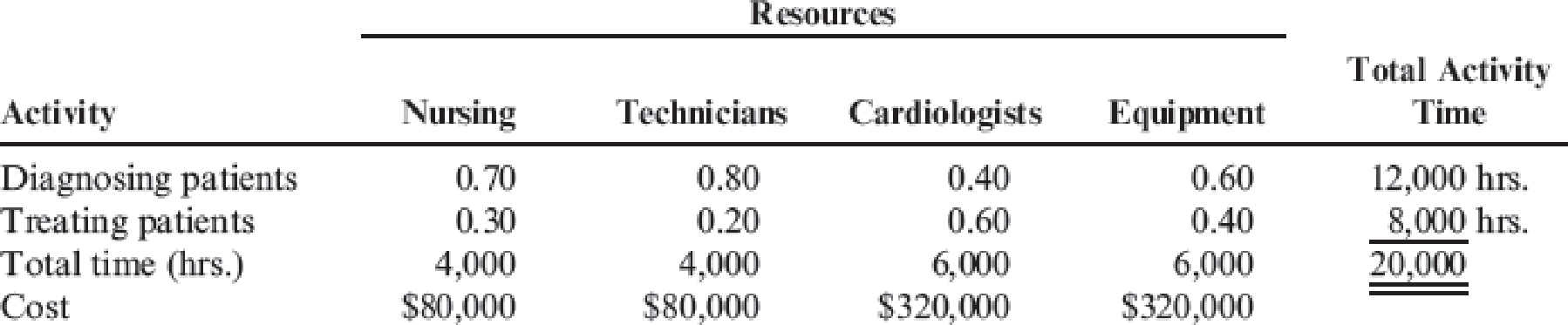

The Bienestar Cardiology Clinic has two major activities: diagnostic and treatment. The two activities use four resources: nursing, medical technicians, cardiologists, and equipment. Detailed interviews have provided the work distribution matrix shown below.

The total time estimated corresponds to practical capacity (interviewers adjusted the total time to about 80 percent of the available time). The equipment time is measured in machine hours. Thus, the total time (at practical capacity) in the system is 20,000 hours. In considering the implementation of a TDABC model, the following unit times and transaction information are also provided:

Required:

- 1. Calculate the cost of each activity using the indicated values of the resource drivers.

- 2. Calculate the capacity cost rate for TDABC. Using the capacity cost rate, calculate the cost of each activity under TDABC. Compare these values with those obtained in Requirement 1 and discuss possible reasons for any differences.

- 3. Suppose that the actual activity driver quantities are 3,500 and 9,000. Calculate the cost of unused capacity.

- 4. Suppose that the clinic acquires new equipment that reduces the total time required for the two activities from 6,000 to 4,000 hours. The equipment cost remains the same. Explain how the ABC system would be updated and then describe how TDABC would provide updates.

- 5. Suppose that diagnosing patients without any cardiac disease takes two hours while diagnosing patients with mildly diseased hearts takes an additional 1.5 hours and those with more severe problems takes an additional two hours. Prepare a time equation and, using the capacity cost rate from Requirement 2, calculate the activity rate for each of the three types of patients.

Trending nowThis is a popular solution!

Chapter 4 Solutions

Bundle: Cornerstones of Cost Management, Loose-Leaf Version, 4th + CengageNOWv2, 1 term Printed Access Card

- Determine the term being defined or described by the following statement: Evaluation of how income will change based on an alternative course of action. a. Differential analysis b. Opportunity cost c. Product cost distortion d. Sunk cost e. Theory of constraintsarrow_forwardAccount Que.arrow_forwardWhat is Jordan ROE? General accountingarrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,