Intermediate Financial Management (MindTap Course List)

13th Edition

ISBN: 9781337395083

Author: Eugene F. Brigham, Phillip R. Daves

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 4, Problem 16P

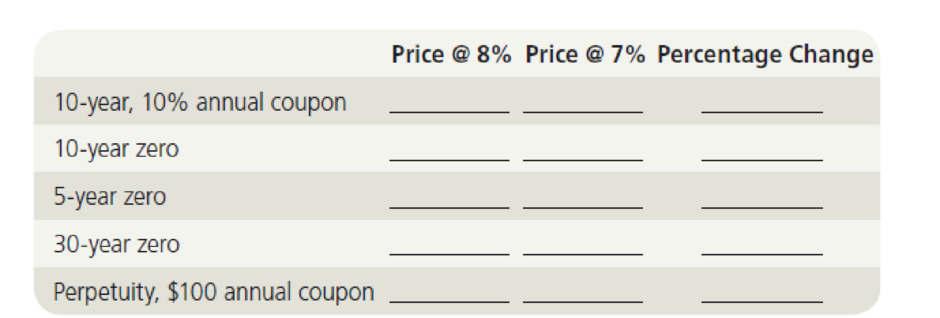

Interest Rate Sensitivity

A bond trader purchased each of the following bonds at a yield to maturity of 8%. Immediately after she purchased the bonds, interest rates fell to 7%. What is the percentage change in the price of each bond after the decline in interest rates? Assume annual coupons and annual compounding. Fill in the following table:

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

A real estate broker insures an office building for $500,000 under a Building and Personal Property Coverage Form with a Causes of Loss-Broad Form attached. If smoke from a nearby industrial factory enters the office building and causes $10,000 in damage to the interior, the policy will pay a MAXIMUM of which of the following amounts?

a. $0

b. $1,000

c. $5,000

d. $10,000

National Bank currently has $500 million in transaction deposits on its balance sheet. The current reserve requirement is 10 percent, but the Federal Reserve is decreasing this requirement to 8 percent.

Show the balance sheet of the Federal Reserve and National Bank if National Bank converts all excess reserves to loans, but borrowers return only 50 percent of these funds to National Bank as transaction deposits.

Show the balance sheet of the Federal Reserve and National Bank if National Bank converts 75 percent of its excess reserves to loans and borrowers return 60 percent of these funds to National Bank as transaction deposits.

The FOMC has instructed the FRBNY Trading Desk to purchase $500 million in U.S. Treasury securities. The Federal Reserve has currently set the reserve requirement at 5 percent of transaction deposits. Assume U.S. banks withdraw all excess reserves and give out loans.

What is the full effect of this purchase on bank deposits and the money supply if borrowers return only 95 percent of these funds to their banks in the form of transaction deposits?

Chapter 4 Solutions

Intermediate Financial Management (MindTap Course List)

Ch. 4 - Short-term interest rates are more volatile than...Ch. 4 - The rate of return on a bond held to its maturity...Ch. 4 - If you buy a callable bond and interest rates...Ch. 4 - A sinking fund can be set up in one of two ways....Ch. 4 - Prob. 1PCh. 4 - Prob. 2PCh. 4 - Current Yield for Annual Payments Heath Food...Ch. 4 - Determinant of Interest Rates

The real risk-free...Ch. 4 - Default Risk Premium A Treasury bond that matures...Ch. 4 - Prob. 6P

Ch. 4 - Bond Valuation with Semiannual Payments

Renfro...Ch. 4 - Prob. 8PCh. 4 - Bond Valuation and Interest Rate Risk The Garraty...Ch. 4 - Prob. 10PCh. 4 - Prob. 11PCh. 4 - Bond Yields and Rates of Return A 10-year, 12%...Ch. 4 - Yield to Maturity and Current Yield You just...Ch. 4 - Current Yield with Semiannual Payments

A bond that...Ch. 4 - Prob. 15PCh. 4 - Interest Rate Sensitivity

A bond trader purchased...Ch. 4 - Bond Value as Maturity Approaches An investor has...Ch. 4 - Prob. 18PCh. 4 - Prob. 19PCh. 4 - Prob. 20PCh. 4 - Bond Valuation and Changes in Maturity and...Ch. 4 - Yield to Maturity and Yield to Call

Arnot...Ch. 4 - Prob. 23PCh. 4 - Prob. 1MCCh. 4 - Prob. 2MCCh. 4 - How does one determine the value of any asset...Ch. 4 - Prob. 4MCCh. 4 - What would be the value of the bond described in...Ch. 4 - Suppose a 10-year, 10% semiannual coupon bond with...Ch. 4 - Prob. 9MCCh. 4 - Prob. 10MCCh. 4 - Prob. 11MCCh. 4 - Prob. 12MCCh. 4 - Prob. 14MCCh. 4 - Prob. 15MCCh. 4 - Prob. 16MCCh. 4 - Prob. 17MC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You bought a bond five years ago for $935 per bond. The bond is now selling for $980. It also paid $75 in interest per year, which you reinvested in the bond. Calculate the realized rate of return earned on this bond. I want to learn how to solve this on my financial calculator. Can you show me how to solve it through there.arrow_forwardWhat are the Cases Not Readily Bound and what is a Dignity in a Research Study? What are the differences between Dignity in a Research Study and Cases Not Readily Bound? Please help to give examples.arrow_forwardWhat are the Case Study Research Design Components. Please help to give examplesWhat are the Case Study Design Tests and Tactics and how would they do?arrow_forward

- Describe some different types of ratios and how they are used to assess performance. Explain the components of the formula and the order of operations to calculate them. Discuss what these ratios say about the financial health of the organization. Determine why it is sometimes misleading to compare a company's financial ratios with those of other firms that operate within the same industry.arrow_forwardIs there retained earning statement an important financial statement at the income statement and or the cash flows statement?arrow_forward2-13. (Term structure of interest rates) You want to invest your savings of $20,000 in government securities for the next 2 years. Currently, you can invest either in a secu- rity that pays interest of 8% per year for the next 2 years or in a security that matures in 1 year but pays only 6% interest. If you make the latter choice, you would then reinvest your savings at the end of the first year for another year. Why might you choose to make the investment in the 1-year security that pays an interest rate of only 6%, as opposed to investing in the 2-year security pay- ing 8%? Provide numerical support for your answer. Which theory of term structure have you supported in your answer? 2-14. (Yield curve) If yields on Treasury securities were currently as follows: TERM YIELD 6 months 1.0% 1 year 1.7% 2 years 2.1% 3 years 2.4% 4 years 2.7% 5 years 2.9% 10 years 3.5% 15 years 3.9% 20 years 4.0% 30 years 4.1% a. Plot the yield curve. b. Explain this yield curve using the unbiased…arrow_forward

- What is the holistic case study format, could you please provide an example?arrow_forwardDescription Discuss in detail the Goal(s) of the firm. Additionally, List and discuss the 5 principles that form the foundations of finance. Lastly, List and discuss the various legal forms of business organizations.arrow_forwardWhat is the purpose of a case studty? Why is it important for researchers? Please give the examplesarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

What happens to my bond when interest rates rise?; Author: The Financial Pipeline;https://www.youtube.com/watch?v=6uaXlI4CLOs;License: Standard Youtube License