EBK CORPORATE FINANCE

4th Edition

ISBN: 9780134202785

Author: DeMarzo

Publisher: VST

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 3.A, Problem A.1P

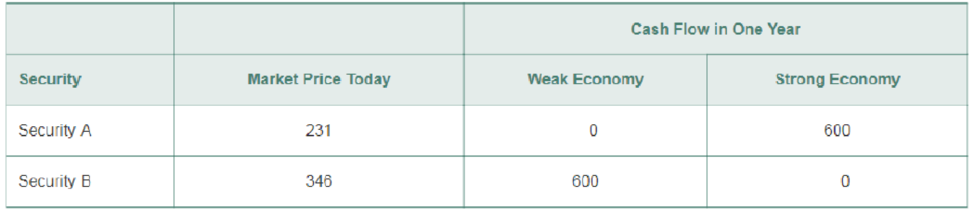

The table here shows the no-arbitrage prices of securities A and B that we calculated.

- a. What are the payoffs of a portfolio of one share of security A and one share of security B?

- b. What is the market price of this portfolio? What expected return will you earn from holding this portfolio?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Don't used Ai solution

Assume an investor deposits $116,000 in a professionally managed account. One year later, the account has grown in value to $136,000 and the investor withdraws $43,000. At the end of the second year, the account value is $107,000. No other additions or withdrawals were made. During the same two years, the risk-free rate remained constant at 3.94 percent and a relevant benchmark earned 9.58 percent the first year and 6.00 percent the second. Calculate geometric average of holding period returns over two years. (You need to calculate IRR of cash flows over two years.)

Round the answer to two decimals in percentage form.

Please help with these questions.

Chapter 3 Solutions

EBK CORPORATE FINANCE

Ch. 3.1 - Prob. 1CCCh. 3.1 - If crude oil trades in a competitive market, would...Ch. 3.2 - How do you compare costs at different points in...Ch. 3.2 - Prob. 2CCCh. 3.3 - What is the NPV decision rule?Ch. 3.3 - Why doesnt the NPV decision rule depend on the...Ch. 3.4 - Prob. 1CCCh. 3.4 - Prob. 2CCCh. 3.5 - If a firm makes an investment that has a positive...Ch. 3.5 - Prob. 2CC

Ch. 3.5 - Prob. 3CCCh. 3.A - The table here shows the no-arbitrage prices of...Ch. 3.A - Suppose security Chas a payoff of 600 when the...Ch. 3.A - Prob. A.3PCh. 3.A - Prob. A.4PCh. 3.A - Prob. A.5PCh. 3.A - Consider a portfolio of two securities: one share...Ch. 3.A2 - Why does the expected return of a risky security...Ch. 3.A2 - Prob. 2CCCh. 3.A3 - Prob. 1CCCh. 3.A3 - Prob. 2CCCh. 3 - Honda Motor Company is considering offering a 2000...Ch. 3 - You are an international shrimp trader. A food...Ch. 3 - Prob. 3PCh. 3 - Prob. 4PCh. 3 - You have decided to take your daughter skiing in...Ch. 3 - Suppose the risk-free interest rate is 4%. a....Ch. 3 - You have an investment opportunity in Japan. It...Ch. 3 - Your firm has a risk-free investment opportunity...Ch. 3 - You run a construction firm. You have just won a...Ch. 3 - Your firm has identified three potential...Ch. 3 - Your computer manufacturing firm must purchase...Ch. 3 - Prob. 12PCh. 3 - Prob. 13PCh. 3 - An American Depositary Receipt (ADR) is security...Ch. 3 - Prob. 15PCh. 3 - An Exchange-Traded Fund (ETF) is a security that...Ch. 3 - Consider two securities that pay risk-free cash...Ch. 3 - Prob. 18P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Please help with these questionsarrow_forwardIn 1895, the first U.S. Putting Green Championship was held. The winner's prize money was $170. In 2022, the winner's check was $3,950,000. a. What was the percentage increase per year in the winner's check over this period? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. b. If the winner's prize increases at the same rate, what will it be in 2053? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. a. Increase per year b. Winners prize in 2053 %arrow_forwardDerek plans to retire on his 65th birthday. However, he plans to work part-time until he turns 73.00. During these years of part-time work, he will neither make deposits to nor take withdrawals from his retirement account. Exactly one year after the day he turns 73.0 when he fully retires, he will begin to make annual withdrawals of $183,008.00 from his retirement account until he turns 94.00. After this final withdrawal, he wants $1.52 million remaining in his account. He he will make contributions to his retirement account from his 26th birthday to his 65th birthday. To reach his goal, what must the contributions be? Assume a 6.00% interest rate. Round to 2 decimal places.arrow_forward

- Derek plans to retire on his 65th birthday. However, he plans to work part-time until he turns 71.00. During these years of part-time work, he will neither make deposits to nor take withdrawals from his retirement account. Exactly one year after the day he turns 71.0 when he fully retires, he will begin to make annual withdrawals of $177,333.00 from his retirement account until he turns 94.00. He he will make contributions to his retirement account from his 26th birthday to his 65th birthday. To reach his goal, what must the contributions be? Assume a 9.00% interest rate. Submit Answer format: Currency: Round to: 2 decimal places.arrow_forwardDerek plans to retire on his 65th birthday. However, he plans to work part-time until he turns 72.00. During these years of part-time work, he will neither make deposits to nor take withdrawals from his retirement account. Exactly one year after the day he turns 72.0 when he fully retires, he will wants to have $3,104,476.00 in his retirement account. He he will make contributions to his retirement account from his 26th birthday to his 65th birthday. To reach his goal, what must the contributions be? Assume a 8.00% interest rate. Submit Answer format: Currency: Round to: 2 decimal places.arrow_forwardBanking and finance sector ma job kaise payearrow_forward

- 1. Bond X is worth $91 today. The bond will mature in one year and pay $100 or $84 with probabilities 0.75 and 0.25, respectively. Assuming the bond pays no cash flows during the year, which of the following is closest to the expected return on the bond? 5% 0% 0% 5% 0% 2. At the beginning of the year, a mutual fund has a NAV of $20. At the end of the year, the NAV is $21 and the fund has received no dividends or other distributions throughout the year. The return on the fund’s benchmark over the same period of time was 10%. Suppose the fund incurred expenses of $2 per fund share during the year. What was the return on the fund’s underlying portfolio before any expenses that affected NAV? Did this before-expense return beat the fund’s benchmark? 15%; Yes, the fund’s underlying portfolio beat its benchmark 15%; No, the fund’s underlying portfolio beat its benchmark 0%; No, the fund’s underlying portfolio beat its benchmark 20%; Yes, the fund’s underlying portfolio beat its benchmark…arrow_forward1. Which of the following assets is most likely to trade over the counter but still have high liquidity? a. A short-term Treasury bond b. A long-term corporate bond c. A short-term corporate bond d. A large-cap stock e. A small-cap stock 2. Assume you purchased 600 shares of XYZ common stock on margin at $35 per share from your broker. If the initial margin is 60%, the amount you borrowed from the broker is closest to _________. a. $8,500 b. $21,000 c. $29,500 d. $12,500 e. $16,000 3. You invest $1,550 in security A with a beta of 1.4 and $1,350 in security B with a beta of 0.4. The beta of this portfolio is closest to _____________ . a. 0.95 b. 0.90 c. 1.35 d. 1.05 e. 1.15 4. Which of the following orders is most likely to increase the difference between the highest bid price and the lowest ask price? a. A large market order b. A large limit order c. A small limit order d. A small market order e. There will be no major difference between these 5. Bond X is worth $91 today.…arrow_forward1. At the beginning of the year, a mutual fund has a NAV of $20. At the end of the year, the NAV is $21 and the fund has received no dividends or other distributions throughout the year. The return on the fund’s benchmark over the same period of time was 10%. What was the return to investors in the fund? Did the fund’s return to investors beat the benchmark return? a. 5%; No, the fund did not beat its benchmark b. 10%; No, the fund did not beat its benchmark c. 15%; No, the fund did not beat its benchmark d. 20%; Yes, the fund beat its benchmark e. None of the above 2. You are advising a pension fund that is required to have a portfolio risk of 5%. Which of the following would be the portfolio optimization problem for constructing their fund? a. Maximize return subject to a constraint that portfolio volatility is 5% b. Not enough information c. Maximize the Sharpe ratio with no additional constraints d. Minimize the risk needed to get their long-term return target e. None of the…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Chapter 8 Risk and Return; Author: Michael Nugent;https://www.youtube.com/watch?v=7n0ciQ54VAI;License: Standard Youtube License