Corporate Finance (4th Edition) (Pearson Series in Finance) - Standalone book

4th Edition

ISBN: 9780134083278

Author: Jonathan Berk, Peter DeMarzo

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 3.A, Problem A.1P

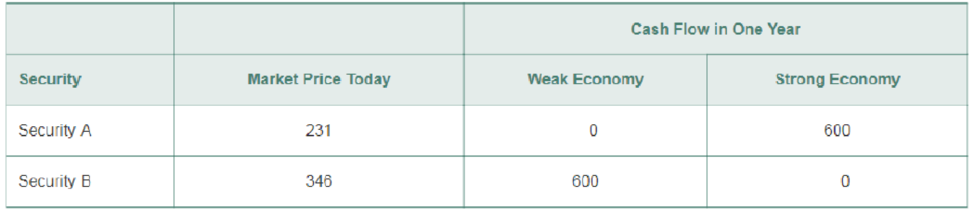

The table here shows the no-arbitrage prices of securities A and B that we calculated.

- a. What are the payoffs of a portfolio of one share of security A and one share of security B?

- b. What is the market price of this portfolio? What expected return will you earn from holding this portfolio?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

For EnPro, Please find the following values using the pdf (value line) provided . Please no excle.

When finding R, use the formula: Risk Free Rate + Beta * (Market Rate – Risk Free Rate)

The Risk Free Rate will always be 0.016 and the Market Rate will always be 0.136 for this problem. (For R, I got 17.2%, If I'm wrong can you please explain how)

On Value Line: DPO = All Div'ds to Net Profit

On Value Line: ROE = Return on Shr. Equity

On Value Line: P/E = Avg Ann'l P/E ratio*

The first 4 results should be rated to the year 2025 (r, Average DPO, Growth rate, Average P/E)

r= _

Average DPO= _

Growth rate= _

Average P/E= _

2026 EPS= _

2027 EPS= _

2028 EPS= _

2026 dividend= _

2027 dividend= _

2028 dividend= _

2028 price= _

2028 total cash flow Intrinsic value= _

You want to buy equipment that is available from 2 companies. The price of the equipment is the same for both companies. Gray

Media would let you make quarterly payments of $1,430 for 7 years at an interest rate of 1.59 percent per quarter. Your first payment to

Gray Media would be today. River Media would let you make monthly payments of $X for 8 years at an interest rate of 1.46 percent per

month. Your first payment to River Media would be in 1 month. What is X?

Input instructions: Round your answer to the nearest dollar.

59

You want to buy equipment that is available from 2 companies. The price of the equipment is the same for both companies. Gray

Media would let you make quarterly payments of $14,000 for 6 years at an interest rate of 1.50 percent per quarter. Your first payment

to Gray Media would be in 3 months. Island Media would let you make monthly payments of $X for 4 years at an interest rate of

1.35 percent per month. Your first payment to Island Media would be today. What is X?

Input instructions: Round your answer to the nearest dollar.

99

Chapter 3 Solutions

Corporate Finance (4th Edition) (Pearson Series in Finance) - Standalone book

Ch. 3.1 - Prob. 1CCCh. 3.1 - If crude oil trades in a competitive market, would...Ch. 3.2 - How do you compare costs at different points in...Ch. 3.2 - Prob. 2CCCh. 3.3 - What is the NPV decision rule?Ch. 3.3 - Why doesnt the NPV decision rule depend on the...Ch. 3.4 - Prob. 1CCCh. 3.4 - Prob. 2CCCh. 3.5 - If a firm makes an investment that has a positive...Ch. 3.5 - Prob. 2CC

Ch. 3.5 - Prob. 3CCCh. 3.A - The table here shows the no-arbitrage prices of...Ch. 3.A - Suppose security Chas a payoff of 600 when the...Ch. 3.A - Prob. A.3PCh. 3.A - Prob. A.4PCh. 3.A - Prob. A.5PCh. 3.A - Consider a portfolio of two securities: one share...Ch. 3.A2 - Why does the expected return of a risky security...Ch. 3.A2 - Prob. 2CCCh. 3.A3 - Prob. 1CCCh. 3.A3 - Prob. 2CCCh. 3 - Honda Motor Company is considering offering a 2000...Ch. 3 - You are an international shrimp trader. A food...Ch. 3 - Prob. 3PCh. 3 - Prob. 4PCh. 3 - You have decided to take your daughter skiing in...Ch. 3 - Suppose the risk-free interest rate is 4%. a....Ch. 3 - You have an investment opportunity in Japan. It...Ch. 3 - Your firm has a risk-free investment opportunity...Ch. 3 - You run a construction firm. You have just won a...Ch. 3 - Your firm has identified three potential...Ch. 3 - Your computer manufacturing firm must purchase...Ch. 3 - Prob. 12PCh. 3 - Prob. 13PCh. 3 - An American Depositary Receipt (ADR) is security...Ch. 3 - Prob. 15PCh. 3 - An Exchange-Traded Fund (ETF) is a security that...Ch. 3 - Consider two securities that pay risk-free cash...Ch. 3 - Prob. 18P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You plan to retire in 7 years with $X. You plan to withdraw $54,100 per year for 15 years. The expected return is 13.19 percent per year and the first regular withdrawal is expected in 7 years. What is X? Input instructions: Round your answer to the nearest dollar. SAarrow_forwardYou plan to retire in 3 years with $911,880. You plan to withdraw $X per year for 18 years. The expected return is 18.56 percent per year and the first regular withdrawal is expected in 3 years. What is X? Input instructions: Round your answer to the nearest dollar. $ 59arrow_forwardYou just borrowed $203,584. You plan to repay this loan by making regular quarterly payments of X for 69 quarters and a special payment of $56,000 in 7 quarters. The interest rate on the loan is 1.94 percent per quarter and your first regular payment will be made today. What is X? Input instructions: Round your answer to the nearest dollar. $arrow_forward

- I got 1.62 but it's wrong why?arrow_forwardYou plan to retire in 8 years with $X. You plan to withdraw $114,200 per year for 21 years. The expected return is 17.92 percent per year and the first regular withdrawal is expected in 9 years. What is X? Input instructions: Round your answer to the nearest dollar. 69 $arrow_forwardHow much do you need in your account today if you expect to make quarterly withdrawals of $6,300 for 7 years and also make a special withdrawal of $25,700 in 7 years. The expected return for the account is 4.56 percent per quarter and the first regular withdrawal will be made today. Input instructions: Round your answer to the nearest dollar. $arrow_forward

- For EnPro, Please find the following values using the pdf (value line) provided . Please no excle. On Value Line: DPO = All Div'ds to Net Profit On Value Line: ROE = Return on Shr. Equity On Value Line: P/E = Avg Ann'l P/E ratio* r= _ Average DPO= _ Growth rate= _ Average P/E= _ 2026 EPS= _ 2027 EPS= _ 2028 EPS= _ 2026 dividend= _ 2027 dividend= _ 2028 dividend= _ 2028 price= _ 2028 total cash flow Intrinsic value= _arrow_forwardDon't used hand raitingarrow_forwardYou want to buy equipment that is available from 2 companies. The price of the equipment is the same for both companies. Gray Media would let you make quarterly payments of $14,000 for 6 years at an interest rate of 1.50 percent per quarter. Your first payment to Gray Media would be in 3 months. Island Media would let you make monthly payments of $X for 4 years at an interest rate of 1.35 percent per month. Your first payment to Island Media would be today. What is X? Input instructions: Round your answer to the nearest dollar. SA $arrow_forward

- You want to buy equipment that is available from 2 companies. The price of the equipment is the same for both companies. Gray Media would let you make quarterly payments of $1,430 for 7 years at an interest rate of 1.59 percent per quarter. Your first payment to Gray Media would be today. River Media would let you make monthly payments of $X for 8 years at an interest rate of 1.46 percent per month. Your first payment to River Media would be in 1 month. What is X? Input instructions: Round your answer to the nearest dollar. $arrow_forwardYou just borrowed $203,584. You plan to repay this loan by making regular quarterly payments of X for 69 quarters and a special payment of $56,000 in 7 quarters. The interest rate on the loan is 1.94 percent per quarter and your first regular payment will be made today. What is X? Input instructions: Round your answer to the nearest dollar. 59arrow_forwardYou plan to retire in 4 years with $698,670. You plan to withdraw $X per year for 17 years. The expected return is 17.95 percent per year and the first regular withdrawal is expected in 5 years. What is X? Input instructions: Round your answer to the nearest dollar. $arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Chapter 8 Risk and Return; Author: Michael Nugent;https://www.youtube.com/watch?v=7n0ciQ54VAI;License: Standard Youtube License