Concept explainers

Videos

Rolertyme Company manufactures roller skates. With the exception of the rollers, all parts of the skates are produced internally. Neeta Booth, president of Rolertyme, has decided to make the rollers instead of buying them from external suppliers. The company needs 100,000 sets per year (currently it pays $1.90 per set of rollers).

The rollers can be produced using an available area within the plant. However, equipment for production of the rollers would need to be leased ($30,000 per year lease payment). Additionally, it would cost $0.50 per machine hour for power, oil, and other operating expenses. The equipment will provide 60,000 machine hours per year. Direct material costs will average $0.75 per set, and direct labor will average $0.25 per set. Since only one type of roller would be produced, no additional demands would be made on the setup activity. Other

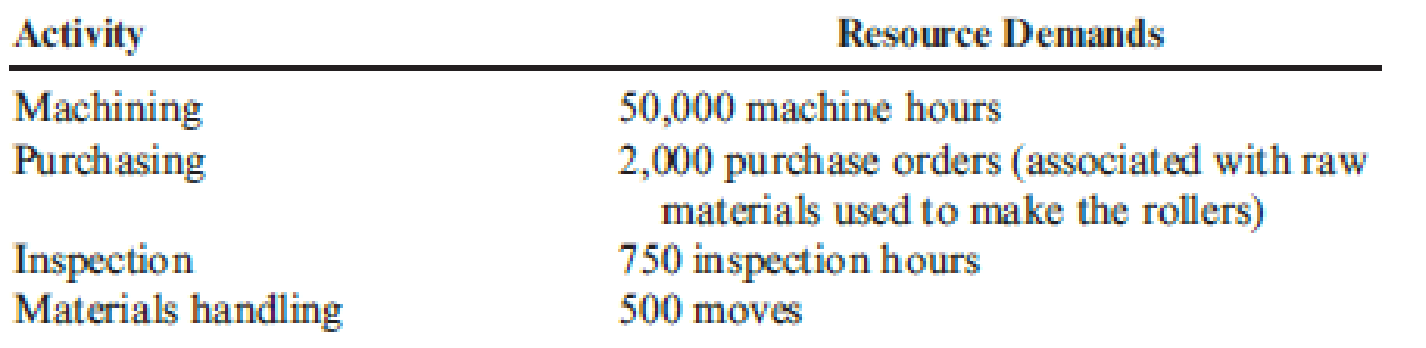

Production of rollers would place the following demands on the overhead activities:

Producing the rollers also means that the purchase of outside rollers will cease. Thus, purchase orders associated with the outside acquisition of rollers will drop by 5,000. Similarly, the moves for the handling of incoming orders will decrease by 200. The company has not inspected the rollers purchased from outside suppliers.

Required:

- 1. Classify all resources associated with the production of rollers as flexible resources and committed resources. Label each committed resource as a short- or long-term commitment. How should we describe the cost behavior of these short- and long-term resource commitments? Explain.

- 2. Calculate the total annual resource spending (for all activities except for setups) that the company will incur after production of the rollers begins. Break this cost into fixed and variable activity costs. In calculating these figures, assume that the company will spend no more than necessary. What is the effect on resource spending caused by production of the rollers?

- 3. Refer to Requirement 2. For each activity, break down the cost of activity supplied into the cost of activity output and the cost of unused activity.

Trending nowThis is a popular solution!

Chapter 3 Solutions

Cornerstones of Cost Management (Cornerstones Series)

- Michael McDowell Co. establishes a $108 million liability at the end of 2025 for the estimated site-cleanup costs at two of its manufacturing facilities. All related closing costs will be paid and deducted on the tax return in 2026. Also, at the end of 2025, the company has $54 million of temporary differences due to excess depreciation for tax purposes, $7.56 million of which will reverse in 2026. The enacted tax rate for all years is 20%, and the company pays taxes of $34.56 million on $172.80 million of taxable income in 2025. McDowell expects to have taxable income in 2026. Assuming that the only deferred tax account at the beginning of 2025 was a deferred tax liability of $5,400,000, draft the income tax expense portion of the income statement for 2025, beginning with the line "Income before income taxes." (Hint: You must first compute (1) the amount of temporary difference underlying the beginning $5,400,000 deferred tax liability, then (2) the amount of temporary differences…arrow_forwardNeed help with this general accounting questionarrow_forwardHow much is the annual amortization expense for 2022 on these financial accounting question?arrow_forward

- Give true answer this general accounting questionarrow_forwardAmy is evaluating the cash flow consequences of organizing her business entity SHO as an LLC (taxed as a sole proprietorship), an S corporation, or a C corporation. She used the following assumptions to make her calculations: a) For all entity types, the business reports $22,000 of business income before deducting compensation paid to Amy and payroll taxes SHO pays on Amy's behalf. b) All entities use the cash method of accounting. c) If Amy organizes SHO as an S corporation or a C corporation, SHO will pay Amy a $5,000 annual salary (assume the salary is reasonable for purposes of this problem). For both the S and C corporations, Amy will pay 7.65 percent FICA tax on her salary and SHO will also pay 7.65 percent FICA tax on Amy's salary (the FICA tax paid by the entity is deductible by the entity). d) Amy's marginal ordinary income tax rate is 35 percent, and her income tax rate on qualified dividends and net capital gains is 15 percent. e) Amy's marginal self-employment tax rate is…arrow_forwardInformation pertaining to Noskey Corporation’s sales revenue follows: November 20X1 (Actual) December 20X1 (Budgeted) January 20X2 (Budgeted)Cash sales $ 115,000 $ 121,000 $ 74,000Credit sales 282,000 409,000 208,000Total sales $ 397,000 $ 530,000 $ 282,000Management estimates 5% of credit sales to be uncollectible. Of collectible credit sales, 60% is collected in the month of sale and the remainder in the month following the month of sale. Purchases of inventory each month include 70% of the next month’s projected total sales (stated at cost) plus 30% of projected sales for the current month (stated at cost). All inventory purchases are on account; 25% is paid in the month of purchase, and the remainder is paid in…arrow_forward

- Mirror Image Distribution Company expects its September sales to be 20% higher than its August sales of $163,000. Purchases were $113,000 in August and are expected to be $133,000 in September. All sales are on credit and are expected to be collected as follows: 40% in the month of the sale and 60% in the following month. Purchases are paid 20% in the month of purchase and 80% in the following month. The cash balance on September 1 is $23,000. The ending cash balance on September 30 is estimated to be:arrow_forwardBalance sheet information is useful for all of the following except:a) evaluating a company's financial flexibilityb) evaluating a company's liquidityc) assesing a company's riskd) determining free cash flowsarrow_forwardNonearrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning