Concept explainers

Videos

a & b

Prepare the necessary journal entries and post to the ledger accounts.

a & b

Explanation of Solution

Prepare the journal entries in the books of M Research firms.

| Date | Account titles and Explanation | Debit ($) | Credit ($) |

| June 1 | Cash (A+) | 28,000 | |

| Common stock (E+) | 28,000 | ||

| (To record the issuance of common stock) | |||

| June 2 | Equipment (A+) | 11,040 | |

| Supplies (A+) | 2,840 | ||

| Cash(A-) | 4,000 | ||

| Accounts payable (L+) | 9,880 | ||

| (To record the purchase of asset) | |||

| June 3 | Rent expense (L-) | 1,275 | |

| Cash (A-) | 1,275 | ||

| (To record the rent expense) | |||

| June 4 | Prepaid advertisement (A+) | 975 | |

| Cash (A-) | 975 | ||

| (To record the prepaid advertisement) | |||

| June 5 | Cash (A+) | 6,400 | |

| Unearned service revenue (L+) | 6,400 | ||

| (To record the unearned service revenue) | |||

| June 6 | Accounts receivable (A+) | 7,500 | |

| Service revenue (E+) | 7,500 | ||

| (To record the service revenue) | |||

| June 7 | Salaries expense (E-) | 3,600 | |

| Cash (A-) | 3,600 | ||

| (To record the Salaries expense) | |||

| June 8 | Travel expense (E-) | 1,440 | |

| Cash (A-) | 1,440 | ||

| (To record the travel expense) | |||

| June 9 | Postage expense(E-) | 520 | |

| Cash (A-) | 520 | ||

| (To record the postage expense) | |||

| June 10 | Salaries expense(E-) | 3,600 | |

| Cash (A-) | 3,600 | ||

| (To record the salaries expense) | |||

| June 11 | Accounts receivable (A+) | 7,200 | |

| Service revenue (E+) | 7,200 | ||

| (To record the service revenue) | |||

| June 12 | Cash (A+) | 7,800 | |

| Accounts receivable (A-) | 7,800 | ||

| (To record the accounts receivable) | |||

| June 13 | Dividends (E-) | 2,500 | |

| Cash(A-) | 2,500 | ||

| (To record the payment of cash dividends) |

Table (1)

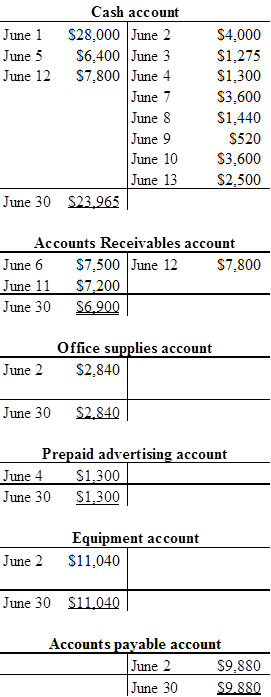

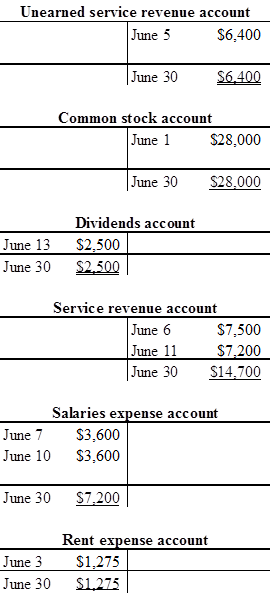

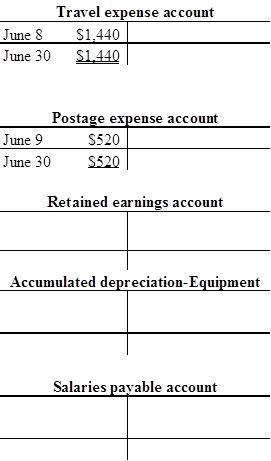

T-account:

T-account is the form of the ledger account, where the journal entries are posted to this account. It is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.

The components of the T-account are as follows:

a) The title of the account

b) The left or debit side

c) The right or credit side

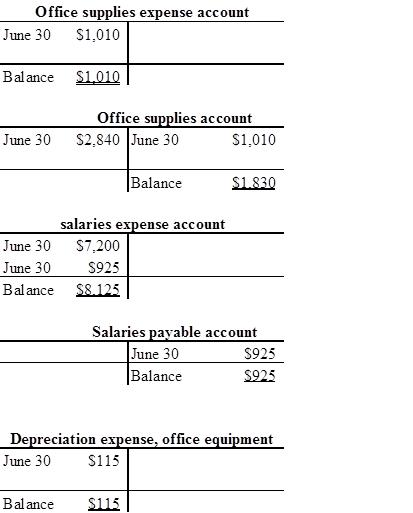

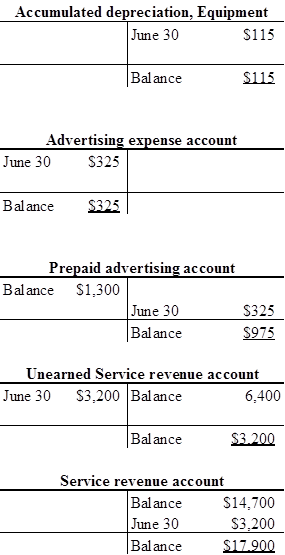

Prepare the T-accounts:

c.

Prepare an unadjusted

c.

Explanation of Solution

Unadjusted trial balance:

Unadjusted trial balance is that statement which contains complete list of accounts with their unadjusted balances. This statement is prepared at the end of every financial period.

Prepare the unadjusted trial balance as of 30th June.

| T Company | ||

| Unadjusted Trial Balance | ||

| June 30, 2014 | ||

| Accounts | Debit ($) | Credit ($) |

| Cash | 23,965 | |

| Supplies | 2,840 | |

| Accounts receivable | 6,900 | |

| Prepaid advertising | 1,300 | |

| Equipment | 11,040 | |

| Accounts Payable | 9,880 | |

| Common Stock | 28,000 | |

| Dividends | 2,500 | |

| Service Revenue | 14,700 | |

| Unearned Service Revenue | 6,400 | |

| Salaries Expense | 7,200 | |

| Rent expense | 1,275 | |

| Travel expense | 1,440 | |

| Postage expense | 520 | |

| Total | 58,980 | 58,980 |

Table (2)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $58,980.

d.

Prepare the

d.

Explanation of Solution

Adjusting entries: Adjusting entries are the journal entries which are recorded at the end of the accounting period to correct or adjust the revenue and expense accounts, to concede with the accrual principle of accounting.

Prepare the adjusting entries in the books of W Catering Service.

| Date | Account titles and Explanation | Debit ($) | Credit ($) |

| June 30 | Office Supplies Expense (E+) (1) | 1,010 | |

| Office Supplies (A–) | 1,010 | ||

| (To record the adjusting entry for office supplies expense) | |||

| June 30 | Salaries Expense (E+) | 925 | |

| Salaries Payable (L+) | 925 | ||

| (To record the adjusting entry for salaries expense) | |||

| June 30 | 115 | ||

| 115 | |||

| (To record the amount of depreciation for June ) | |||

| June 30 | Advertising Expense (E–) | 325 | |

| Prepaid Insurance(A–) | 325 | ||

| (To record the amount of prepaid advertising expired during the period) | |||

| June 30 | Unearned Service (L–) | 3,200 | |

| Service Revenue (E+) | 3,200 | ||

| (To record the amount of unearned service revenue earned for the month of June) |

Table (3)

Working note:

Calculate the amount of office supplies used during the year:

Calculate the amount of depreciation on equipment for the month June:

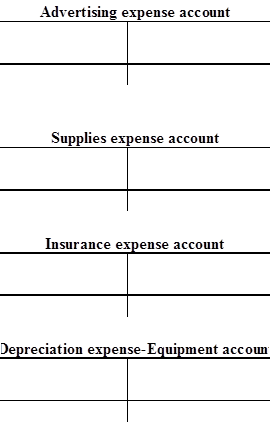

T-account:

T-account is the form of the ledger account, where the journal entries are posted to this account. It is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.

The components of the T-account are as follows:

a) The title of the account

b) The left or debit side

c) The right or credit side

Prepare the T-accounts:

Want to see more full solutions like this?

Chapter 3 Solutions

FINANCIAL ACCT.F/UNDERGRADS-W/ACCESS

- Ferrari Industries is preparing its cash budget for the month of August. The company estimated credit sales for August at $320,000. Actual credit sales for July were $240,000. Estimated collections in August for credit sales in August are 30%. Estimated collections in August for credit sales in July are 55%. Estimated collections in August for credit sales prior to July are $22,000. Estimated write-offs in August for uncollectible credit sales are $14,000. The estimated provision for bad debts in August for credit sales in August is $12,000. What are the estimated cash receipts from accounts receivable collections in August?arrow_forwardI need help with question is correct answer and accountingarrow_forwardWhat is the ending inventory value?arrow_forward

- I am looking for a reliable way to solve this financial accounting problem using accurate principles.arrow_forwardI am trying to find the accurate solution to this financial accounting problem with appropriate explanations.arrow_forwardPlease provide the accurate answer to this general accounting problem using valid techniques.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education