Videos

Analyze Pacific Airways

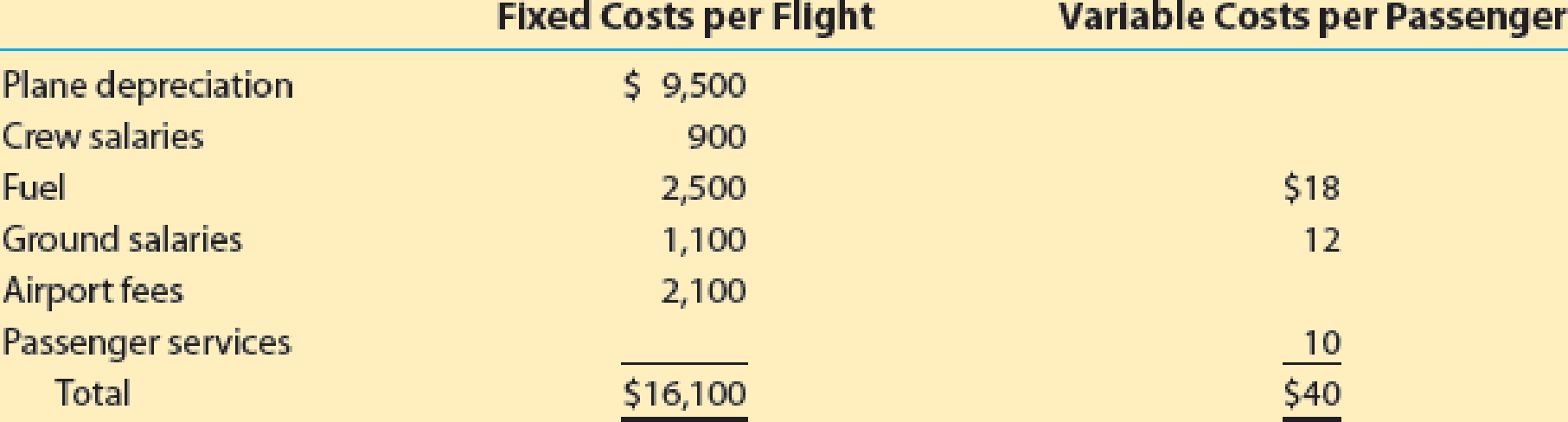

Pacific Airways provides air travel services between Los Angeles and Seattle. Cost information per flight is as follows:

Each flight has a capacity of 150 seats, with an average of 125 seats sold per flight at an average ticket price of $180. Assume Pacific Airways is considering a new service that would provide tickets at half price. Passengers would need to fly standby to receive the discount, but would be provided a flight for a given day of travel. An analysis revealed that an average of 8 existing passengers would use the new discounted tickets for travel. In addition, 15 new passengers would be attracted to the offer.

- a. Determine the contribution margin per passenger for the full-priced ticket.

- b. Determine the break-even number of seats sold per flight.

- c. Determine the contribution margin per passenger for discounted tickets.

- d. Should Pacific Airways offer the discounted ticket plan? Answer the question by computing the incremental contribution margin per flight for the plan.

a.

Compute the contribution margin per passenger for the full-priced ticket.

Explanation of Solution

Contribution Margin: The amount of sales revenue remained after the variable costs are incurred is called contribution margin. In other words, contribution margin is the surplus amount of revenue over variable costs.

The following is the formula to calculate the contribution margin:

Contribution Margin = Sales – Variable cost

Calculate the contribution margin per passenger.

The contribution margin per passenger at full fare is $140.

b.

Compute the break-even number of seats sold per flight.

Explanation of Solution

Break-even: Break even refers to the point where the production can yield all the costs involved and any further production contributes to the profit.

Calculate the break even seats per flight.

The break even seats per flight are 115 seats.

c.

Compute the contribution margin per passenger for the discounted tickets.

Explanation of Solution

Contribution Margin: The amount of sales revenue remained after the variable costs are incurred is called contribution margin. In other words, contribution margin is the surplus amount of revenue over variable costs.

Calculate the contribution margin per passenger.

The contribution margin per passenger at discounted fare is $50.

d.

Compute the incremental contribution margin per flight to decide on the proposal to allow discount.

Explanation of Solution

Contribution Margin: The amount of sales revenue remained after the variable costs are incurred is called contribution margin. In other words, contribution margin is the surplus amount of revenue over variable costs.

Calculate the incremental contribution margin per flight.

The incremental contribution margin per flight is $30.

Working Note (1):

Calculate the lost contribution margin from customers switching tickets.

Working Note (2):

Calculate the gained contribution margin from discount customers.

Differential Analysis: Differential analysis refers to the analysis of differential revenue which a company could gain or differential cost which a company could incur based on the available alternative options of business.

Prepare the differential analysis table to analyze the effect of the new plan:

| Differential Analysis of Company PA | |||

| Continue with No Change (Alt. 1) or Offer the Discount Plan (Alt. 2) | |||

| February 5 | |||

| Particulars | No Change (Alternative 1) | Discount Plan (Alternative 2) | Differential Effect (Alternative 2) |

| Revenues per flight | (3) $22,500 | (4) $23,130 | $630 |

| Costs per flight: | |||

| Plane depreciation | ($9,500) | ($9,500) | $0 |

| Crew salaries | ($900) | ($900) | $0 |

| Fuel | (5) ($4,750) | (6) ($5,020) | ($270) |

| Ground salaries | (7) ($2,600) | (8) ($2,780) | ($180) |

| Airport fees | ($2,100) | ($2,100) | $0 |

| Passenger services | (9) ($1,250) | (10) ($1,400) | ($150) |

| Income per flight | $1,400 | $1,430 | $30 |

Table (1)

The differential analysis of Company PA shows that the offer of Discount plan, has a greater differential income of $30.

Working Note (3):

Calculate the revenue per flight for existing plan.

Working Note (4):

Calculate the revenue per flight for new plan.

Working Note (5):

Calculate the fuel price for existing plan.

Working Note (6):

Calculate the fuel price for new plan.

Working Note (7):

Calculate the ground salaries for existing plan.

Working Note (8):

Calculate the ground salaries for new plan.

Working Note (9):

Calculate the passenger services cost for existing plan.

Working Note (10):

Calculate the passenger services cost for new plan.

Want to see more full solutions like this?

Chapter 25 Solutions

Financial and Managerial Accounting - Workingpapers

- Hello tutor please provide correct answer general accounting questionarrow_forwardRobinson Manufacturing discovered the following information in its accounting records: $519,800 in direct materials used, $223,500 in direct labor, and $775,115 in manufacturing overhead. The Work in Process Inventory account had an opening balance of $72,400 and a closing balance of $87,600. Calculate the company’s Cost of Goods Manufactured.arrow_forwardSanjay would like to organize HOS (a business entity) as either an S corporation or as a corporation (taxed as a C corporation) generating a 16 percent annual before-tax return on a $350,000 investment. Sanjay’s marginal tax rate is 24 percent and the corporate tax rate is 21 percent. Sanjay’s marginal tax rate on individual capital gains and dividends is 15 percent. HOS will pay out its after-tax earnings every year to either its members or its shareholders. If HOS is taxed as an S corporation, the business income allocation would qualify for the deduction for qualified business income (assume no limitations on the deduction). Assume Sanjay does not owe any additional Medicare tax or net investment income tax. Required 1. For each scenario, C corporation and S corporation, calculate the total tax (entity level and owner level). 2. For each scenario, C corporation and S corporation, calculate the effective tax rate. C Corporation S Corporation 1. Total tax…arrow_forward

- I need correct solution of this general accounting questionarrow_forwardHii expert please given correct answer general accountingarrow_forwardMarkowis Corp has collected the following data concerning its maintenance costs for the pest 6 months units produced Total cost July 18,015 36,036 august 37,032 40,048 September 36,036 55,055 October 22,022 38,038 November 40,040 74,575 December 38,038 62,062 Compute the variable coot per unit using the high-low method. (Round variable cost per mile to 2 decimal places e.g. 1.25) Compute the fixed cost elements using the high-low method.arrow_forward

- Use the following data to determine the total dollar amount of assets to be classified as current assets. Marigold Corp. Balance Sheet December 31, 2025 Cash and cash equivalents Accounts receivable Inventory $67000 Accounts payable $126000 86500 Salaries and wages payable 11100 149000 Bonds payable 161500 Prepaid insurance 83000 Total liabilities 298600 Stock investments (long-term) 193000 Land 199500 Buildings $226000 Common stock 309400 Less: Accumulated depreciation (53500) 172500 Retained earnings 475500 Trademarks 133000 Total stockholders' equity 784900 Total assets $1083500 Total liabilities and stockholders' equity $1083500 ○ $269100 $385500 ○ $236500 ○ $578500arrow_forwardShould the machine be replaced?arrow_forwardUsing the following balance sheet and income statement data, what is the total amount of working capital? Current assets $39700 Net income $52100 Current liabilities 19800 Stockholders' equity 96700 Average assets 198400 Total liabilities 52100 Total assets 148800 Average common shares outstanding was 18600. ○ $9900 ○ $39700 ○ $19900 ○ $12400arrow_forward

- Suppose that Old Navy has assets of $4265000, common stock of $1018000, and retained earnings of $659000. What are the creditors' claims on their assets? ○ $2588000 ○ $3906000 ○ $1677000 ○ $4624000arrow_forwardBrody Corp. uses a process costing system. Beginning inventory for January consisted of 1,400 units that were 46% completed. 10,300 units were started during January. On January 31, the inventory consisted of 550 units that were 77% completed. How many units were completed during the period?arrow_forwardCurrent Attempt in Progress Whispering Winds Corp. has five plants nationwide that cost $275 million. The current fair value of the plants is $460 million. The plants will be reported as assets at $735 million. O $460 million. $275 million. O $185 million.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College