Videos

MASTERY PROBLEM

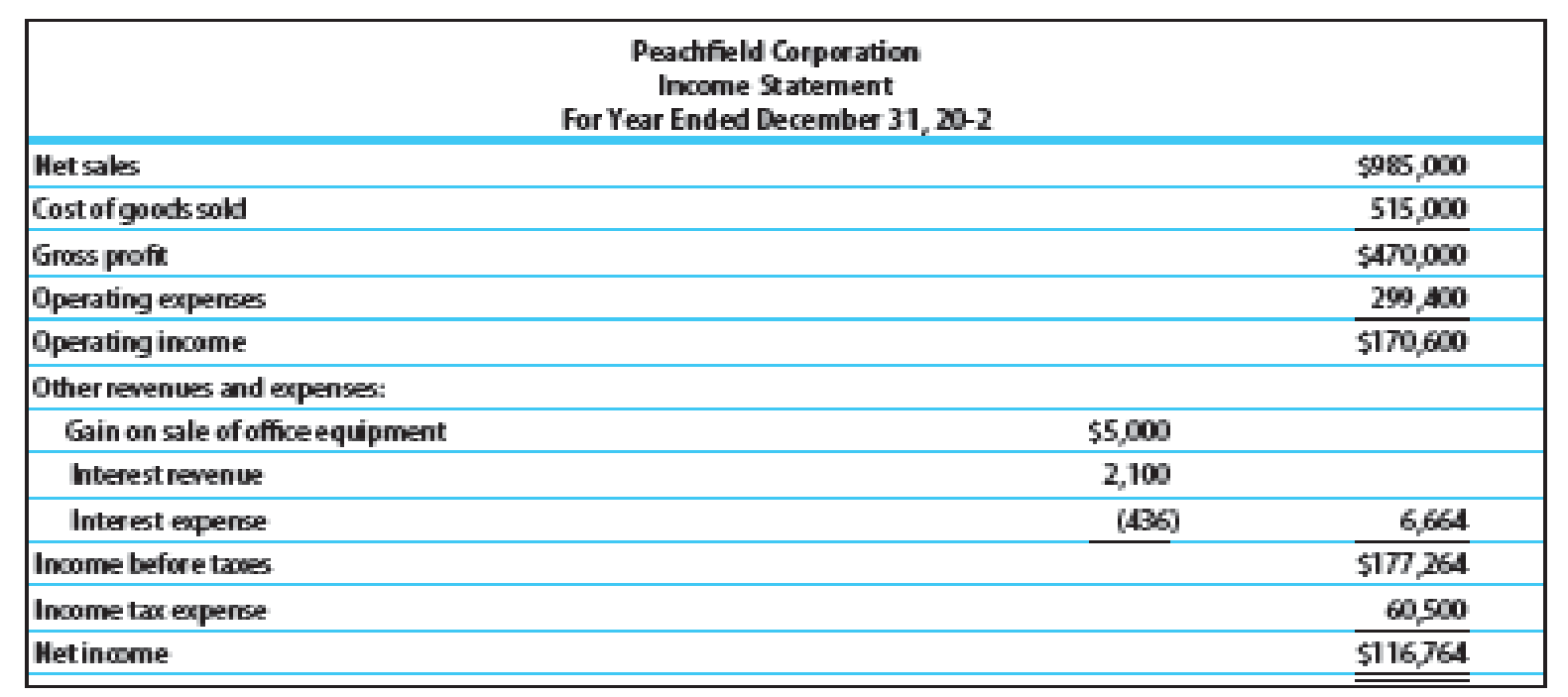

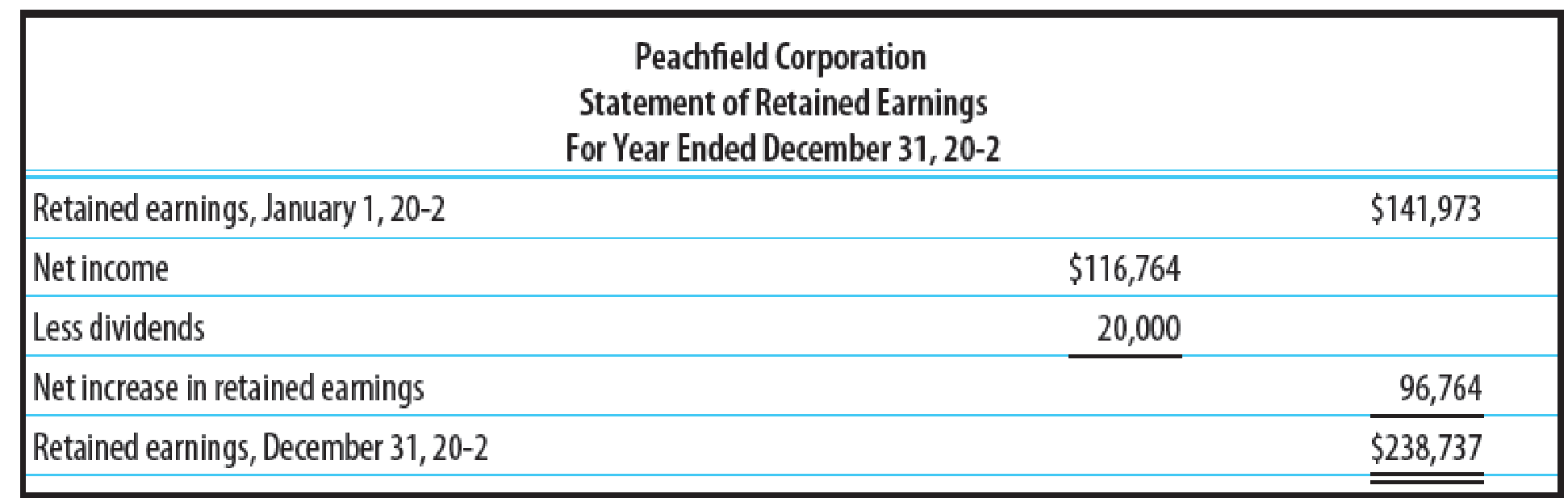

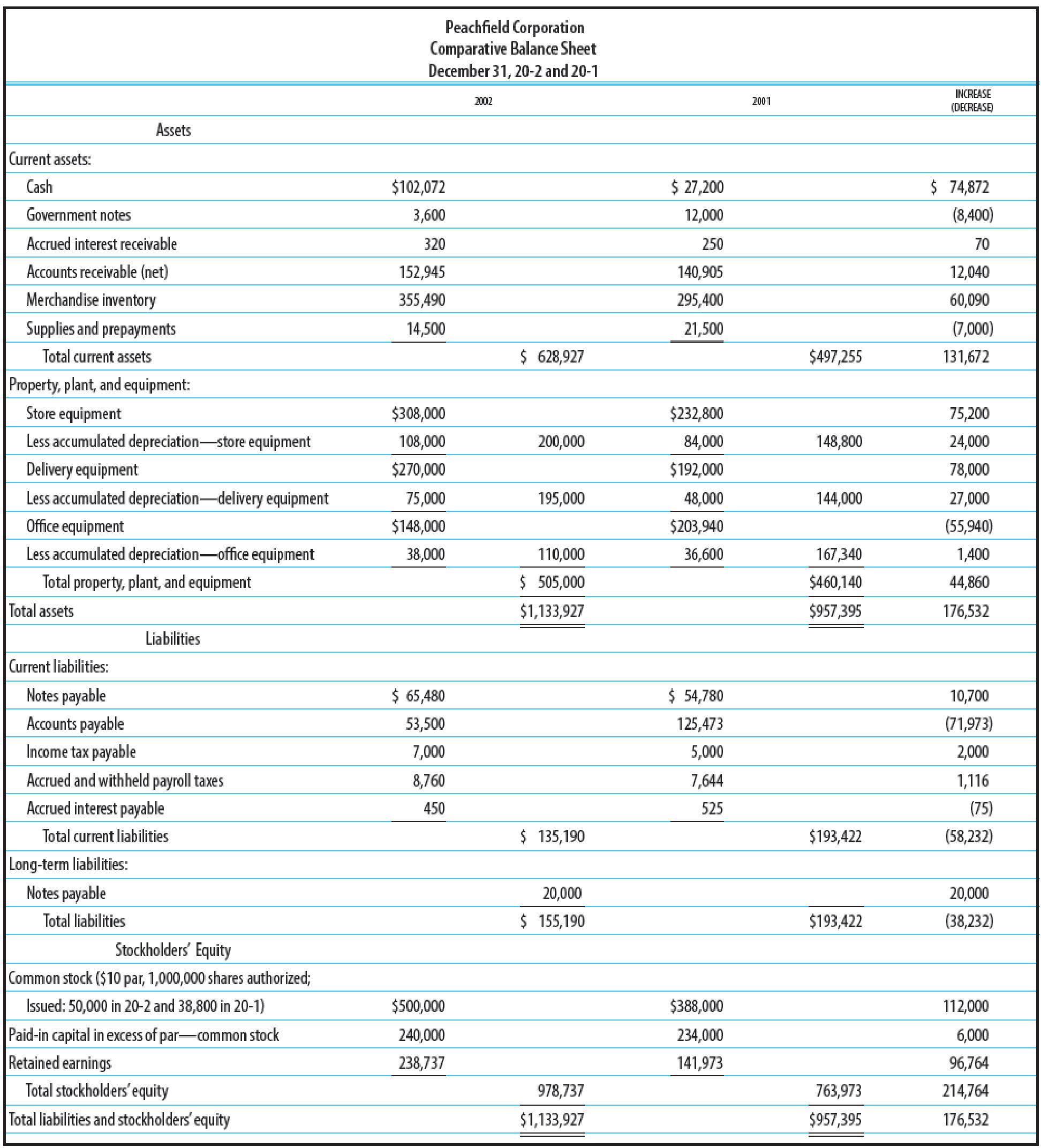

Financial statements for Peachfield Corporation as well as additional information relevant to

Additional information:

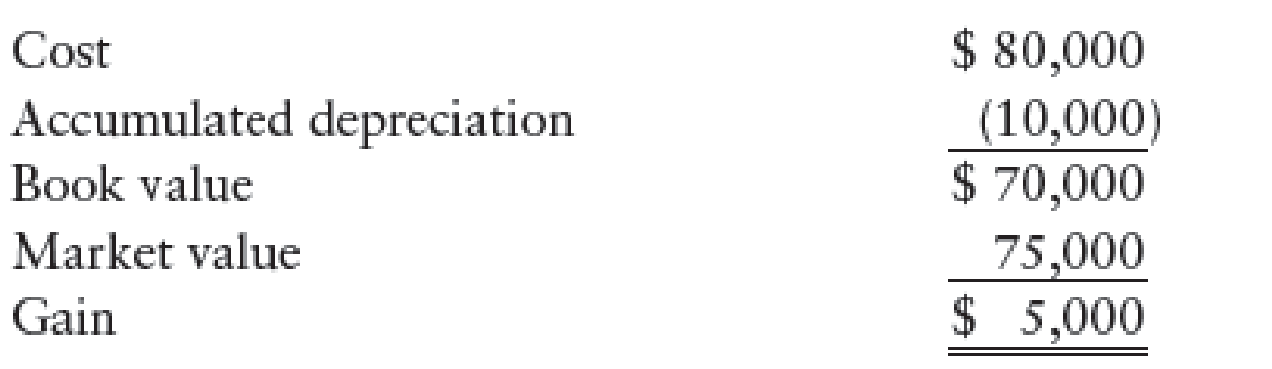

1. Office equipment was sold during the year for $75,000.

2.

3. No other equipment was sold during the year. The following purchases were made for cash.

4. Declared and paid cash dividends of $20,000.

5. Issued 11,200 shares of $10 par common stock for $118,000.

6. Issued a note payable for $10,700.

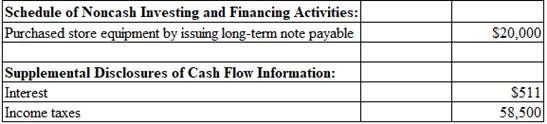

7. Additional store equipment was acquired by issuing a long-term note payable for $20,000.

REQUIRED

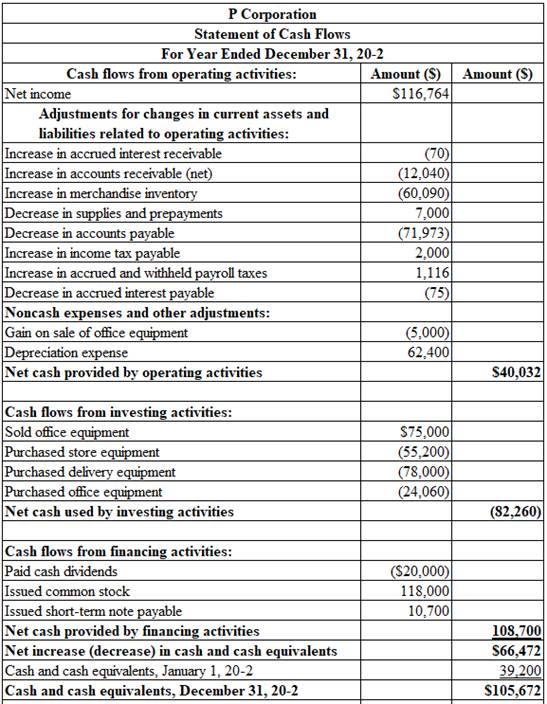

1. Prepare a statement of cash flows explaining the change in cash and cash equivalents.

2. Reconcile cash and cash equivalents at the bottom of the statement of cash flows.

1.

Prepare a statement of cash flows explaining the change in cash and cash equivalents.

Explanation of Solution

Statement of cash flows: This statement reports all the cash transactions which are responsible for inflow and outflow of cash, and result of these transactions is reported as ending balance of cash at the end of reported period. Statement of cash flows includes the changes in cash balance due to operating, investing, and financing activities.

Indirect method: Under indirect method, net income is reported first, and then non-cash expenses, losses from fixed assets, and changes in opening balances and ending balances of current assets and current liabilities are adjusted to reconcile the net income balance.

Cash flows from operating activities: Operating activities refer to the normal activities of a company to carry out the business.

The below table shows the way of calculation of cash flows from operating activities:

| Cash flows from operating activities (Indirect method) |

| Net income: |

| Add: Decrease in current assets |

| Increase in current liability |

| Depreciation expense and amortization expense |

| Loss on sale of plant assets |

| Deduct: Increase in current assets |

| Decrease in current liabilities |

| Gain on sale of plant assets |

| Net cash provided from or used by operating activities |

Table (1)

Cash flows from investing activities: Investing activities refer to the activities carried out by a company for acquisition of long term assets. It includes the purchase or sale of equipment or land, or marketable securities, which is used for business operations.

The below table shows the way of calculation of cash flows from investing activities:

| Cash flows from investing activities |

| Add: Proceeds from collection of loan made to borrowers |

| Sale of marketable securities / investments |

| Sale of property, plant and equipment |

| Proceeds from discounting notes receivables |

| Deduct: Purchase of fixed assets/long-lived assets |

| Loan made by the company to others |

| Purchase of marketable securities |

| Net cash provided from or used by investing activities |

Table (2)

Cash flows from financing activities: Financing activities refer to the activities carried out by a company to mobilize funds to carry out the business activities. It includes raising cash from long-term debt or payment of long-term debt, which is used for business operations.

The below table shows the way of calculation of cash flows from financing activities:

| Cash flows from financing activities |

| Add: Issuance of common stock |

| Proceeds from borrowings by signing of a mortgage |

| Proceeds from sale of treasury stock |

| Proceeds from issuance of debt |

| Deduct: Payment of dividend |

| Repayment of debt |

| Repayment of the principal on loan |

| Redemption of debt |

| Purchase of treasury stock |

| Net cash provided from or used by financing activities |

Table (3)

Prepare a statement of cash flows explaining the change in cash and cash equivalents.

Table (1)

Working notes:

Compute the amount of cash paid for interest in 20-2.

Compute the amount of cash paid for income taxes in 20-2.

2.

Reconcile cash and cash equivalents at the bottom of the statement of cash flows.

Explanation of Solution

Cash: Cash is the money readily available in the form of currency. Since cash can be easily converted into other types of assets, it is reported as first item in the assets section as the most liquid asset.

Cash equivalents: Cash equivalents are the near-cash items, which are readily convertible into cash. Cash equivalents have a maturity period of three months, or less than 3 months. Cash equivalents are reported along with cash in the assets section of the balance sheet, as ‘Cash and cash equivalents’.

Calculate the amount of cash and cash equivalents at January 1, 20-2.

Calculate the amount of cash and cash equivalents at December 31, 20-2.

Want to see more full solutions like this?

Chapter 23 Solutions

Bundle: College Accounting, Chapters 1-15, Loose-Leaf Version, 22nd + LMS Integrated for CengageNOWv2, 1 term Printed Access Card

- Hello tutor please help mearrow_forwardStark Company, a 90% owned subsidiary of Parker, Incorporated, sold land to Parker on May 1, 2023, for $80,000. The land originally cost Stark $85,000. Stark reported net income of $200,000, $180,000, and $220,000 for 2023, 2024, and 2025, respectively. Parker sold the land purchased from Stark for $92,000 in 2025. Both companies use the equity method of accounting. Which of the following will be included in a consolidation entry for 2023? Multiple Choice Credit Gain on Sale of Land for $5,000. Debit Retained Earnings for $5,000. Debit Loss on Sale of Land for $5,000. Credit Loss on Sale of Land for $5,000. Debit Land for $5,000.arrow_forwardWhat is the current stock price of this financial accounting question?arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning