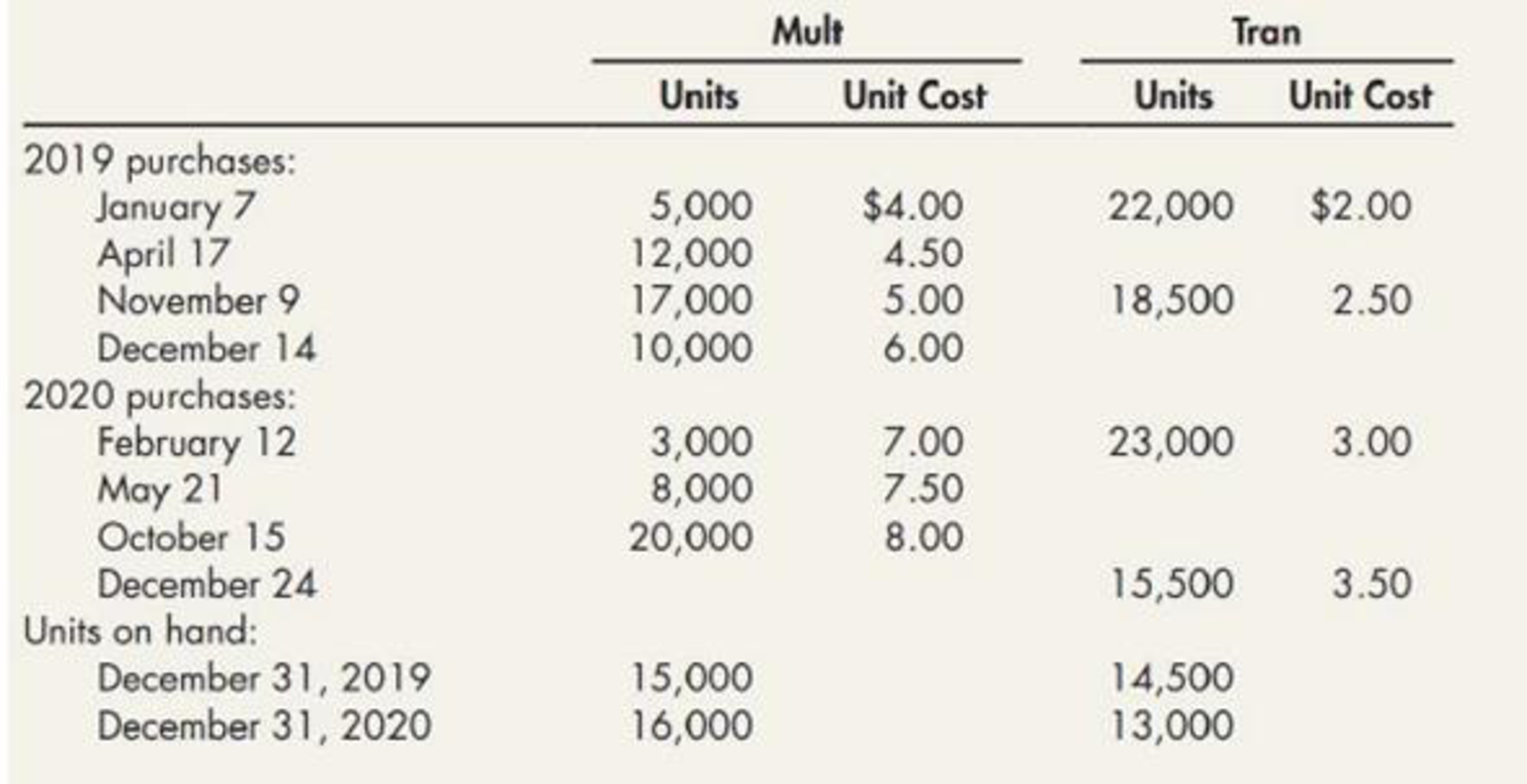

Kraft Manufacturing Company manufactures two products: Mult and Tran. At December 31, 2019, Kraft used the FIFO inventory method. Effective January 1, 2020, Kraft changed to the LIFO inventory method. The cumulative effect of this change is not determinable, and, as a result, the ending inventory of 2019, for which the FIFO method was used, is also the beginning inventory for 2020 for the LIFO method. Any layers added during 2020 should be costed by reference to the first acquisitions of 2020, and any layers liquidated during 2020 should be considered a permanent liquidation. The following information was available from Kraft’s inventory records for the two most recent years: Required: Compute the effect on income before income taxes for the year ended December 31, 2020, resulting from the change from the FIFO to the LIFO inventory method.

Kraft Manufacturing Company manufactures two products: Mult and Tran. At December 31, 2019, Kraft used the FIFO inventory method. Effective January 1, 2020, Kraft changed to the LIFO inventory method. The cumulative effect of this change is not determinable, and, as a result, the ending inventory of 2019, for which the FIFO method was used, is also the beginning inventory for 2020 for the LIFO method. Any layers added during 2020 should be costed by reference to the first acquisitions of 2020, and any layers liquidated during 2020 should be considered a permanent liquidation. The following information was available from Kraft’s inventory records for the two most recent years: Required: Compute the effect on income before income taxes for the year ended December 31, 2020, resulting from the change from the FIFO to the LIFO inventory method.

Solution Summary: The author explains the three types of accounting changes: a change in an accounting principle, changes in accounting estimates, and the retrospective adjustment method.

Kraft Manufacturing Company manufactures two products: Mult and Tran. At December 31, 2019, Kraft used the FIFO inventory method. Effective January 1, 2020, Kraft changed to the LIFO inventory method. The cumulative effect of this change is not determinable, and, as a result, the ending inventory of 2019, for which the FIFO method was used, is also the beginning inventory for 2020 for the LIFO method. Any layers added during 2020 should be costed by reference to the first acquisitions of 2020, and any layers liquidated during 2020 should be considered a permanent liquidation.

The following information was available from Kraft’s inventory records for the two most recent years:

Required:

Compute the effect on income before income taxes for the year ended December 31, 2020, resulting from the change from the FIFO to the LIFO inventory method.

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning