Videos

Hager’s Home Repair Company, a regional hardware chain, which specializes in “do-it-yourself” materials and equipment rentals, is considering an acquisition of Lyon Lighting (LL). Doug Zona, Hager’s treasurer and your boss, has been asked to place a value on the target and he has enlisted your help.

LL has 20 million shares of stock trading at $12 per share. Security analysts estimate LL’s beta to be 1.25. The risk-free rate is 5.5% and the market risk premium is 4%. LL’s capital structure is 20% financed with debt at an 8% interest rate; any additional debt due to the acquisition also will have an 8% rate. LL has a 25% federal-plus-state tax rate, which will not change due to the acquisition.

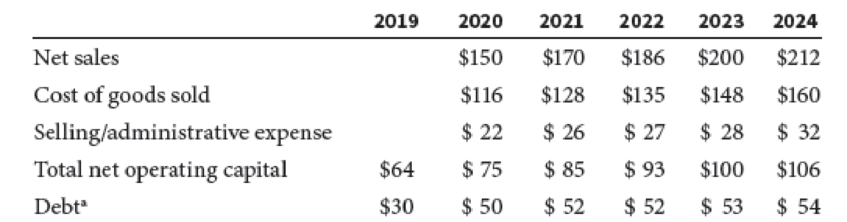

The following data incorporate expected synergies and required levels of total net operating capital for LL should Hager’s complete the acquisition. The

Note:

aDebt is added on the first day of the year, so the 2019 debt is LL’s debt prior to the acquisition.

Hager’s management is new to the merger game, so Zona has been asked to answer some basic questions about mergers as well as to perform the merger analysis. To structure the task, Zona has developed the following questions, which you must answer and then defend to Hager’s board:

Why can’t we estimate LL’s value to Hager’s by discounting the FCFs at the WACC? What method is appropriate? Use the projections and other data to determine the LL division’s

Want to see the full answer?

Check out a sample textbook solution

Chapter 22 Solutions

Financial Management: Theory & Practice

- Question 25 Jasmine bought a house for $225 000. She already knows that for the first $200 000, the land transfer tax will cost $1650. Calculate the total land transfer tax. (2 marks) Land Transfer Tax Table Value of Property Rate On the first $30 000 0% On the next $60 000 0.5% (i.e., $30 001 to $90 000) On the next $60 000 1.0% (i.e., $90 001 to $150 000) On the next $50 000 1.5% (i.e., $150 001 to $200 000) On amounts in excess of $200 000 2.0% 225000–200 000 = 825000 25000.002 × 25000 1= 8500 16 50+ 500 2 marksarrow_forwardSuppose you deposit $1,000 today (t = 0) in a bank account that pays an interest rate of 7% per year. If you keep the account for 5 years before you withdraw all the money, how much will you be able to withdraw after 5 years? Calculate using formula. Calculate using year-by-year approach. Find the present value of a security that will pay $2,500 in 4 years. The opportunity cost (interest rate that you could earn from alternative investments) is 5%. Calculate using the formula. Calculate using year-by-year discounting approach. Solve for the unknown in each of the following: Present value Years Interest rate Future value $50,000 12 ? $152,184 $21,400 30 ? $575,000 $16,500 ? 14% $238,830 $21,400 ? 9% $213,000 Suppose you enter into a monthly deposit scheme with Chase, where you have your salary account. The bank will deduct $25 from your salary account every month and the first payment (deduction) will be made…arrow_forwardPowerPoint presentation of a financial analysis that includes the balance sheet, income statement, and statement of cash flows for Nike and Adidas. Your analysis should also accomplish the following: Include the last three years of data, and evaluate the trends in the data. Summarize the footnotes on each of the statements. Compute the earnings per share for the three years. Compare the two companies and determine the insights gathered from the trend analysis.arrow_forward

- In addition to the customer affairs department of the insurance company the insurance policy must identify which other following on the policy Name of the producer Current director of insurance Policyholder satisfaction rating for paying claims 4. Financial rating from a recognized financial rating servicearrow_forwardIn addition to the customer affairs department of the insurance company the insurance policy must identify which other following on the policy Name of the producer Current director of insurance Policyholder satisfaction rating for paying claims D. Financial rating from a recognized financial rating servicearrow_forwardUnearned premium refunds for insurance policies cancelled when an insurance company is covered by the Illinois Insurance guaranty fund is subject to a MAXIMUM premium refund of what amount? A.$ 100.00 B.$ 1000.00 C.$10,000.00 D.$ 100,000.00arrow_forward

- Before the department of insurance can issue an order charging an insurance company with improper claims practices, they must first: Review the company's financial statement on file with the department Determine that the practice has been done with such frequency as to indicate a business practice Contact the company's competitors to determine if they know how the company operates Contact the NAIC to determine if the company is on the watch listarrow_forwardthe last three (3) years of the EPS and a summary of the footnotes for Nike and Adidas.arrow_forwardThe last three years of data, and evaluate the trends in the data. Summarize the footnotes on each of the statements. Compute the earnings per Include the last three years of data, and evaluate the trends in the data. Summarize the footnotes on each of the statements. Compute the earnings per share for the three years. Compare Nike and Adidas and determine the insights gathered from the trend analysis. With references PowerPoint slidesarrow_forward

- What does it means the Dignity in a Research Study? Please give examplesHow Christian researchers ensure dignity in a research study? Please give examplesarrow_forwardThe 3 A cost us also givenarrow_forwardFree Cash Flow Use the financial statements shown here for Lan & Chen Technologies. The federal-plus-state tax rate is 25%. Lan & Chen Technologies: Income Statements for Year Ending December 31 (Thousands of Dollars) 2023 2022 Sales $960,000 $900,000 Expenses excluding depreciation and amortization 820,000 774,000 EBITDA $140,000 $126,000 Depreciation and amortization 33,000 31,500 EBIT $107,000 $94,500 Interest Expense 10,000 8,900 EBT $97,000 $85,600 Taxes (25%) 24,250 21,400 Net income $72,750 $64,200 Common dividends $43,000 $41,230 Addition to retained earnings $29,750 $22,970 Lan & Chen Technologies: December 31 Balance Sheets (Thousands of Dollars) Assets 2023 2022 Cash and cash equivalents $48,250 $45,000 Short-term investments 3,200 3,600 Accounts Receivable 280,500 270,000 Inventories 141,000 135,000 Total current assets $472,950 $453,600 Net fixed assets 360,750 315,000 Total assets…arrow_forward

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning