Concept explainers

Videos

Statement of

Direct method: The direct method uses the cash basis of accounting for the preparation of the statement of cash flows. It takes into account those revenues and expenses for which cash is either received or paid.

Cash flows from operating activities: Cash flows from operating activity represent the net cash flows from the general operation of the business by comparing the cash receipt and cash payments.

Cash Receipts: It encompasses all the cash receipts from sale of goods and on account receivable.

Cash Payments: It encompasses all the cash payments that are made to suppliers of goods and all expenses that are paid.

The below table shows the way of calculation of cash flows from operating activities:

| Cash flows from operating activities (Direct method) |

| Add: Cash receipts. |

| Cash receipt from customer |

| Less: Cash payments: |

| To supplier |

| For operating expenses |

| Income tax expenses |

| Net cash provided from or used by operating activities |

Table (1)

Cash flows from investing activities: Cash provided by or used in investing activities is a section of statement of cash flows. It includes the purchase or sale of equipment or land, or marketable securities, which is used for business operations.

The below table shows the way of calculation of cash flows from investing activities:

| Cash flows from investing activities |

| Add: Proceeds from sale of fixed assets |

| Sale of marketable securities / investments |

| Deduct: Purchase of fixed assets/long-lived assets |

| Purchase of marketable securities |

| Net cash provided from or used by investing activities |

Table (2)

Cash flows from financing activities: Cash provided by or used in financing activities is a section of statement of cash flows. It includes raising cash from long-term debt or payment of long-term debt, which is used for business operations.

The below table shows the way of calculation of cash flows from financing activities:

| Cash flows from financing activities |

| Add: Issuance of common stock |

| Proceeds from borrowings |

| Proceeds from issuance of debt |

| Issuance of bonds payable |

| Deduct: Payment of dividend |

| Repayment of debt |

| Interest paid |

| Redemption of debt |

| Repurchase of stock |

| Net cash provided from or used by financing activities |

Table (3)

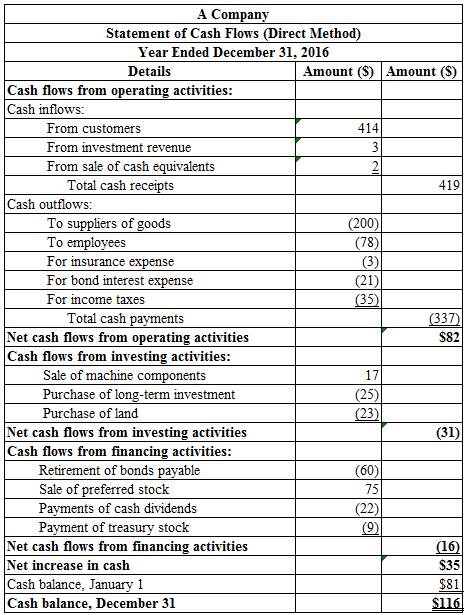

To Prepare: The statement of cash flows from operating activities using direct method for A Company for the year ended December 31, 2016.

Answer to Problem 21.11P

Prepare the statement of cash flow:

Figure (1)

Explanation of Solution

Working notes:

Calculate the amount of cash received from customers:

Cash received from customers} = [Sales revenue + (Accounts receivable in 2015−Accounts receivable in2016)]=[$410+($194−$190)]=$410+$4=$414

Calculate the amount of investment revenue:

Investment revenue = [Amount of investment revenue−A's company share ofnet income−(Investment revenue receivable in 2016−Investment revenue receivable in2015)]=[$11−$6−($6−$4)]=$11−$6−$2=$3

Calculate the amount of cash paid to suppliers:

Cash paid to suppliers = [Cost of goods sold + (Inventory in 2016−Inventory in 2015)+(Accounts payable in 2015−Accounts payable in 2016)]=[$180+($205−$200)+($65−$50)]=$180+$5+$15=$200

Calculate the amount of cash paid to employees:

Cash paid to employees = [Salaries expense + (Salary payable in 2015−Salary payable in 2016)]=[$73 + ($11−$6)]=$73 + $5=$78

Calculate the amount of cash paid for insurance:

Cash paid for insurance =[ Insurance expense−(Prepaid insurance in 2015−Prepaid insurance in 2016)]=[$7−($8−$4)]=$7−$4=$3

Calculate the amount of cash paid for bond interest:

Cash paid for bond interest = [Bond interest expense−(Bond interest payable in 2016−Bond interest payable in 2015)−(Discount on bonds in 2015−Discount on bonds in 2016)]=[$28−($8−$4)−($25−$22)]=$28−$4−$3=$21

Calculate the amount of cash paid for income taxes:

Cash paid for income taxes = [Income tax expense−(Deferred income tax liability in 2016−Deferred income tax liability in 2015)+(Income tax payable in 2015−Income tax payable in 2016)]=[$36−($11−$8)+($14−$12)]=$36−$3+$2=$35

Calculate the amount of sale of machine components:

Sale of machine components = [(Unknown node type: x-custom-btb-me in 2016−Depreciation in 2016)−Loss on machine damage]=($315−$280)−$18=$35−$18=$17

Calculate the amount of land:

Land = Cost of the land−Cash paid for the land=$46−$23=$23(Note issued)

Calculate the amount of retirement of bonds payable:

Retirement of bonds payable = (Bonds payable in 2015−Bonds payable in 2016)=$275−$215=$60

Calculate the amount of dividend:

Step 1: Calculate the amount of cash dividend.

Retained earning in 2016 = (Retained earning in 2015 + Net income−Dividends)$242=$227+$67−DividendDividend=$227+$67−$242=$294−$242=$52

Step 2: Calculate the amount of stock dividend.

Stock dividend = {Number of stock dividend shares × Par value of share}=4 million shares ×$7.5=$30shares

Step 3: Calculate the amount of dividend paid:

Dividend paid = Cash dividend−Stock dividend=$52−$30=$22

Notes:

Note 1: Treasury bill was sold during 2016 at a gain of $2 million. Therefore, it is considered as a gain on sale of cash equivalents.

Note 2: purchase of long-term investment is $25 million.

Note 3: Purchase of land of $23 by issuing cash and a 15%, 4-years lease is considered as non cash investing and financing activities.

Note 4: Sale of

Note 5: the amount of purchase of

Want to see more full solutions like this?

Chapter 21 Solutions

LooseLeaf Intermediate Accounting w/ Annual Report; Connect Access Card

- How much intrest bank collect?arrow_forwardRequired information Skip to question [The following information applies to the questions displayed below.]XYZ declared a $1 per share dividend on August 15. The date of record for the dividend was September 1 (the stock began selling ex-dividend on September 2). The dividend was paid on September 10. Ellis is a cash-method taxpayer. Determine if he must include the dividends in gross income under the following independent circumstances. b. Ellis bought 100 shares of XYZ stock on August 1 for $21 per share. Ellis sold his XYZ shares on September 5 for $23 per share. Ellis received the $100 dividend on September 10 (note that even though Ellis didn’t own the stock on September 10, he still received the dividend because he was the shareholder on the record date).arrow_forwardHow much overhead applied over this year?arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education