Videos

The current price of Estelle Corporation stock is $25. In each of the next two years, this stock price will either go up by 20% or go down by 20%. The stock pays no dividends. The one-year risk-free interest rate is 6% and will remain constant. Using the Binomial Model, calculate the price of a one-year call option on Estelle stock with a strike price of $25.

To determine: The price of a one year call option on ET stock.

Introduction: A binomial model portrays the development of irregular variables over a progression of time steps, relegating specified probabilities to increase or decrease in the variable. The binomial option pricing model makes the improving supposition that, toward the finish of every period, the price of stocks has just two conceivable values.

Answer to Problem 1P

Explanation of Solution

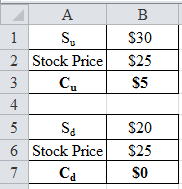

Determine the increase or decrease in the stock price.

Therefore, the stock price either increases to $30 or decreases to $20

Here

S – Denotes the current stock price

K – Denotes the strike price

C – Denotes the call price

B – Denotes the risk-free investment or initial investment in the portfolio

Su – Denotes the probability of increase in stock price (the price to go up)

Sd – Denotes the probability of decrease in stock price next period (the price to go down)

rf – Denotes the risk-free rate

Cu – Denotes the price of the call option if the stock price increases (the price to go up)

Cd – Denotes the price of the call option if the stock price decreases (the price to go down)

Δ – Denotes the shares of stock in the portfolio or the sensitivity of option price to stock price

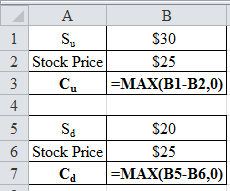

Determine the option payoff:

Using Excel function =MAX, the option payoff is determined as follows:

Excel spreadsheet:

Excel workings:

Therefore, the option payoff either increases to $5 or decreases to $0.

Determine the shares of stock in the replicating portfolio:

Therefore, the share of stock in the replicating portfolio is 0.5.

Determine the risk-free investment or initial investment in the portfolio:

Therefore, the risk-free investment or initial investment in the portfolio is -9.4340.

Determine the price of a one year call option on ET stock:

Therefore, the price of a one year call option on ET stock is $3.07.

Want to see more full solutions like this?

Chapter 21 Solutions

Corporate Finance: The Core (4th Edition) (Berk, DeMarzo & Harford, The Corporate Finance Series)

Additional Business Textbook Solutions

Financial Accounting: Tools for Business Decision Making, 8th Edition

Engineering Economy (17th Edition)

Gitman: Principl Manageri Finance_15 (15th Edition) (What's New in Finance)

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

Horngren's Accounting (12th Edition)

- Define the following: Callable bond Puttable bond Zero-coupon bond Premium bond Discount bond Crossover bonds Even though most corporate bonds in the United States make coupon payments semiannually, bonds issued elsewhere often have annual coupon payments. Suppose a German company issues a bond with a par value of EUR 1,000, 15 years to maturity, a coupon rate of 7.2%. If the yield to maturity is 6.3%, what is the current price of the bond? Rhiannon Corporation has bonds on the market with 13 years to maturity, a YTM of 7.6%, a par value of $1,000, a current market price of $1,075. The bonds make semiannual payments. What must the coupon rate be on these bonds? What would be coupon rate if the current market price is $962.68? What would be the coupon rate if the bonds make quarterly payments? Suppose that a bond has a face value of $1,000 and a YTM of 8% per annum. If the bond pays monthly coupons with an annual coupon rate of 9.6%, what will be the current price of…arrow_forwardWildcat, Incorporated, has estimated sales (in millions) for the next four quarters as follows: Q1 Q2 Q3 Sales $ 195 $ 215 $ 235 Q4 $ 265 Sales for the first quarter of the following year are projected at $210 million. Accounts receivable at the beginning of the year were $83 million. Wildcat has a 45-day collection period. Wildcat's purchases from suppliers in a quarter are equal to 50 percent of the next quarter's forecast sales, and suppliers are normally paid in 36 days. Wages, taxes, and other expenses run about 20 percent of sales. Interest and dividends are $18 million per quarter. Wildcat plans a major capital outlay in the second quarter of $98 million. Finally, the company started the year with a $84 million cash balance and wishes to maintain a $40 million minimum balance. a-1. Assume that Wildcat can borrow any needed funds on a short-term basis at a rate of 3 percent per quarter and can invest any excess funds in short-term marketable securities at a rate of 2 percent per…arrow_forwardConsider the following two bonds: Bond A Bond B Face value $1,000 $1,000 Coupon rate (annual) 8% 8% YTM 9% 7% Maturity 10 years 10 years Price (PV) ? ? Calculate the price for each bond. What is the primary factor affecting the prices of the bonds? Indicate which bond is premium and which one is discount. Is there any relationship between the YTM and the coupon rate in case of premium/discount bonds? Now, consider the following two bonds: Bond X Bond Y Face value $1,000 $1,000 Coupon rate (annual) 8% 8% YTM 11% 11% Maturity 5 years 10 years Price (PV) ? ? Calculate the price for each bond. What is the relationship between bond price and maturity, all else equal? A bond with a par value of $1,000 and a maturity of 8 years is selling for $925. If the annual coupon rate is 7%, what’s the yield on the bond? What would be the yield if the bond had semiannual payments?…arrow_forward

- Don't used hand raitingarrow_forwardDon't used Ai solutionarrow_forwardAssume an investor deposits $116,000 in a professionally managed account. One year later, the account has grown in value to $136,000 and the investor withdraws $43,000. At the end of the second year, the account value is $107,000. No other additions or withdrawals were made. During the same two years, the risk-free rate remained constant at 3.94 percent and a relevant benchmark earned 9.58 percent the first year and 6.00 percent the second. Calculate geometric average of holding period returns over two years. (You need to calculate IRR of cash flows over two years.) Round the answer to two decimals in percentage form.arrow_forward

- Please help with the problem 5-49.arrow_forwardPlease help with these questionsarrow_forwardIn 1895, the first U.S. Putting Green Championship was held. The winner's prize money was $170. In 2022, the winner's check was $3,950,000. a. What was the percentage increase per year in the winner's check over this period? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. b. If the winner's prize increases at the same rate, what will it be in 2053? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. a. Increase per year b. Winners prize in 2053 %arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT