Concept explainers

Videos

Sales-Type Lease with Receipts at End of Year Lamplighter Company, the lessor, agrees to lease equipment to Tilson Company, the lessee, beginning January 1, 2016. The lease terms, provisions, and related events are as follows:

- The lease is noncancelable and has a term of 8 years.

- The annual rentals are $32,000, payable at the end of each year.

- Tilson agrees to pay all executory costs.

- The interest rate implicit in the lease is 14%.

- The cost of the equipment to the lessor is $110,000.

- The lessor incurs no material initial direct costs.

- The collectibility of the rentals is reasonably assured, and there are no important uncertainties surrounding the amount of unreimbursable costs yet to be incurred by the lessor.

- The lessor estimates that the fair value at the end of the lease term will be $20,000 and that the economic life of the equipment is 9 years.

Required:

- 1. Calculate the selling price implied by the lease and prepare a table summarizing the lease receipts and interest revenue earned by the lessor for this sales-type lease.

- 2. Next Level State why this is a sales-type lease.

- 3. Prepare journal entries for Lamplighter for the years 2016, 2017, and 2019.

- 4. Prepare partial

balance sheets for Lamplighter for December 31, 2016, and December 31, 2017, showing how the accounts should be disclosed.

1.

Calculate the selling price as implied in the lease and prepare a table summarizing the lease receipts and interest revenue earned by the lessor Company L for the sales-type lease.

Explanation of Solution

Sales-type Lease: In a Sales-Type lease, the lessor sells the asset to the lessee and records a receivable. In this type of lease, the lessor records a dealer’s or manufacturer’s profit or loss depending upon the difference between the fair value of the assets and the carrying value of the asset.

Calculate the selling price as implied in the lease:

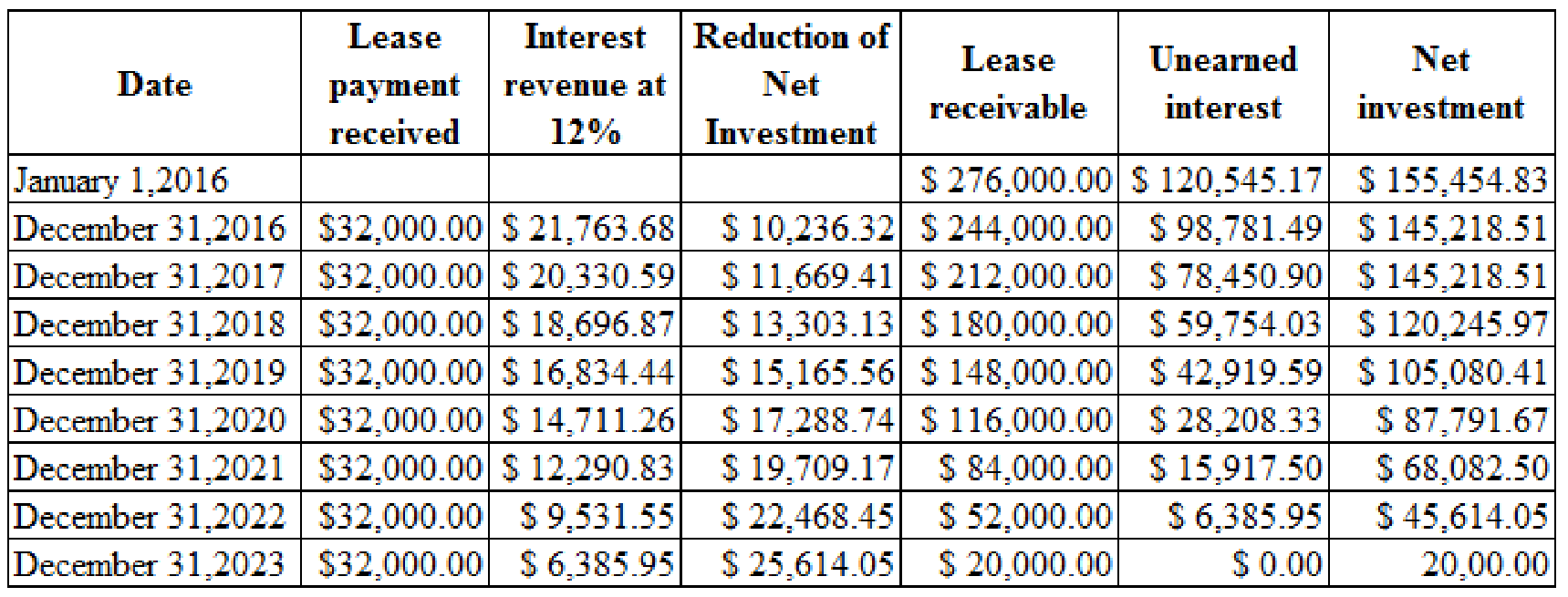

Prepare a table summarizing the lease receipts and interest revenue earned by the lessor Company L for the sales-type lease:

Table (1)

Notes for the above table:

2.

Explain the reasons for classifying the lease as a sale-type lease

Explanation of Solution

In this case, the lease is considered as sales-type lease because, the present value of the lease payments($148,443.65) is greater than the cost of the equipment less the present value of its residual value

3.

Prepare the journal entries for Company L, the lessor for the years 2016, 2017 and 2018.

Explanation of Solution

Journal: Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Rules of Debit and Credit: Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

Prepare the journal entries for Company L, the lessor for the years 2016, 2017 and 2018:

| Date | Accounts title and explanation | Post Ref. | Debit($) | Credit($) |

| January 1,2016 | Lease Receivable | 276,000.00 | ||

| Cost of Asset Leased | 102,988.82 | |||

| Sales | 148,443.65 | |||

| Equipment Leased | 110,000.00 | |||

| Unearned Interest: Leases | 120,545.17 | |||

| (To record the lease receivable in a sales-type lease) | ||||

| December 31,2016 | Unearned Interest: Leases | 21,763.68 | ||

| Interest Revenue: Leases | 21,763.68 | |||

| (To recognize the interest revenue of the year) | ||||

| December 31,2016 | Cash | 320,000.00 | ||

| Lease Receivable | 320,000.00 | |||

| (To record the receipt of lease payment ) | ||||

| December 31,2017 | Cash | 32,000.00 | ||

| Lease Receivable | 32,000.00 | |||

| (To record the receipt of final lease payment ) | ||||

| December 31,2017 | Unearned Interest: Leases | 20,330.59 | ||

| Interest Revenue: Leases | 20,330.59 | |||

| (To recognize the interest revenue of the year) | ||||

| December 31,2019 | Cash | 32,000.00 | ||

| Lease Receivable | 32,000.00 | |||

| (To record the receipt of final lease payment ) | ||||

| December 31,2019 | Unearned Interest: Leases | 16,834.44 | ||

| Interest Revenue: Leases | 16,834.44 | |||

| (To recognize the interest revenue of the year) |

Table (1)

4.

Prepare partial balance sheets for Company L for December 31, 2016 and December 31, 2017 showing the lease accounts reported on it.

Explanation of Solution

Balance Sheet: Balance Sheet is one of the financial statements which summarize the assets, the liabilities, and the Shareholder’s equity of a company at a given date. It is also known as the statement of financial status of the business.

Prepare partial balance sheets for Company L for December 31, 2016 and December 31, 2017 showing the lease accounts reported on it:

| Company L | ||

| Balance Sheet(Partial) | ||

| As on December 31 | ||

| Particulars | 2016 | 2017 |

| Assets | ||

| Current Assets: | ||

| Net Investment in Direct Financing Leases | $28,070.18 | $28,070.18 |

| Non-Current Assets: | ||

| Net Investment in Direct Financing Leases | $117,148.33 | $105,478.92 |

| Liabilities | ||

| Current liabilities: | ||

| Non-Current liabilities: | ||

Table (4)

Notes for the above table:

Want to see more full solutions like this?

Chapter 20 Solutions

Bundle: Intermediate Accounting: Reporting and Analysis, 2017 Update, Loose-Leaf Version, 2nd + CengageNOWv2, 2 terms Printed Access Card

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning