Concept explainers

Videos

Journal entries and

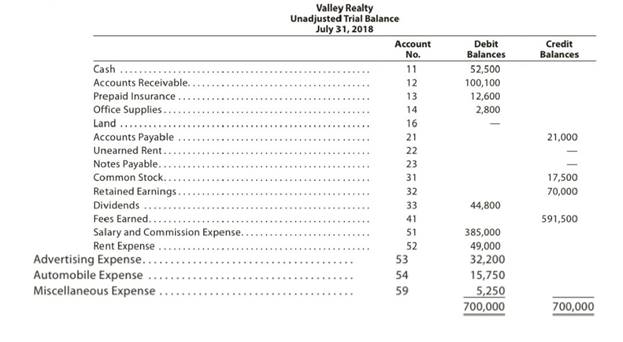

Valley Realty acts as an agent in buying, selling, renting, and managing real estate. The unadjusted trial balance on July 31, 2018, follows:

The following business transactions were completed by Valley Realty during August 2018:

| Aug. 1. | Purchased office supplies on account, $3,150. |

| 2. | Paid rent on office for month, $7,200. |

| 3. | Received cash from clients on account, $83,900. |

| 5. | Paid insurance premiums, $12,000. |

| 9. | Returned a portion of the office supplies purchased on August 1, receiving full credit for their cost, $400. |

| 17. | Paid advertising expense, $8,000. |

| 23. | Paid creditors on account, $13,750. |

| Enter the following transactions on Page 19 of the two-column journal: | |

| 29. | Paid miscellaneous expenses, $1,700. |

| 30. | Paid automobile expense (including rental charges for an automobile), $2,500. |

| 31. | Discovered an error in computing a commission during July; received cash from the salesperson for the overpayment, $2,000. |

| 31. | Paid salaries and commissions for the month, $53,000. |

| 31. | Recorded revenue earned and billed to clients during the month, $183,500. |

| 31. | Purchased land for a future building site for $75,000, paying $7,500 in cash and giving a note payable for the remainder. |

| 31. | Paid dividends, $1,000. |

| 31. | Rented land purchased on August 31 to a local university for use as a parking lot during football season (September, October, and November); received advance payment of $5,000. |

Instructions

- 1. Record the August 1 balance of each account in the appropriate balance column of a four- column account, write Balance in the item section, and place a check mark (*0 in the Posting Reference column.

- 2. Journalize the transactions for August in a two-column journal beginning on Page 18.

Journal entry explanations may be omitted. - 3. Post to the ledger, extending the account balance to the appropriate balance column after each posting.

- 4. Prepare an unadjusted trial balance of the ledger as of August 31, 2018.

- 5. Assume that the August 31 transaction for dividends should have been $10,000. (A) Why did the unadjusted trial balance in (4) balance? (B) Journalize the correcting entry. (C) Is this error a transposition or slide?

(2) and (3)

Journal:

Journal is the book of original entry. Journal consists of the day today financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

Rules of debit and credit:

“An increase in an asset account, an increase in an expense account, a decrease in liability account, and a decrease in a revenue account should be debited.

Similarly, an increase in liability account, an increase in a revenue account and a decrease in an asset account, a decrease in an expenses account should be credited”.

T-account:

An account is referred to as a T-account, because the alignment of the components of the account resembles the capital letter ‘T’. An account consists of the three main components which are as follows:

- The title of the account

- The left or debit side

- The right or credit side

Unadjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Slide error:

A slide error occurs, when the decimal point of an amount has been misplaced.

To journalize: The transactions of August in a two column journal beginning on page 18.

Explanation of Solution

Journalize the transactions of August in a two column journal beginning on page 18.

| Journal Page 18 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2018 | Office supplies | 14 | 3,150 | ||

| August | 1 | Accounts payable | 21 | 3,150 | |

| (To record the purchase of supplies of account) | |||||

| 2. | Rent expense | 52 | 7,200 | ||

| Cash | 11 | 7,200 | |||

| (To record the payment of rent) | |||||

| 3 | Cash | 11 | 83,900 | ||

| Accounts receivable | 12 | 83,900 | |||

| (To record the receipt of cash from clients) | |||||

| 5 | Prepaid insurance | 13 | 12,000 | ||

| Cash | 11 | 12,000 | |||

| (To record the payment of insurance premium) | |||||

| 9 | Accounts payable | 21 | 400 | ||

| Office supplies | 14 | 400 | |||

| (To record the payment made to creditors on account) | |||||

| 17 | Advertising expense | 53 | 8,000 | ||

| Cash | 11 | 8,000 | |||

| (To record the payment of advertising expense) | |||||

| 23 | Accounts payable | 21 | 13,750 | ||

| Cash | 11 | 13,750 | |||

| (To record the payment made to creditors on account) | |||||

Table (1)

| Journal Page 19 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2018 | 29 | Miscellaneous expense | 59 | 1,700 | |

| August | Cash | 11 | 1,700 | ||

| (To record the payment made for Miscellaneous expense) | |||||

| 30 | Automobile expense | 54 | 2,500 | ||

| Cash | 11 | 2,500 | |||

| (To record the payment made for automobile expense) | |||||

| 31 | Cash | 11 | 2,000 | ||

| Salary and commission expense | 51 | 2,000 | |||

| (To record the receipt of cash) | |||||

| 31 | Salary and commission expense | 51 | 53,000 | ||

| Cash | 11 | 53,000 | |||

| (To record the payment made for salary and commission expense) | |||||

| 31 | Accounts receivable | 12 | 183,500 | ||

| Fees earned | 41 | 183,500 | |||

| (To record the revenue earned and billed) | |||||

| 31 | Land | 16 | 75,000 | ||

| Cash | 11 | 7,500 | |||

| Notes payable | 23 | 67,500 | |||

| (To record the purchase of land party for cash and party on signing a note) | |||||

| 31 | Dividends | 33 | 1,000 | ||

| Cash | 11 | 1,000 | |||

| (To record the drawing made for personal use) | |||||

| 31 | Cash | 11 | 5,000 | ||

| Unearned rent | 22 | 5,000 | |||

| (To record the cash received for the service yet to be provide) | |||||

Table (2)

(1) and (3)

To record: The beginning balances of each accounts in the appropriate balance column of a four-column account, and post them to the ledger extending the account balance to the appropriate balance column after each posting.

Explanation of Solution

Solution:

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 52,500 | |||

| 2 | 18 | 7,200 | 45,300 | ||||

| 3 | 18 | 83,900 | 129,200 | ||||

| 5 | 18 | 12,000 | 117,200 | ||||

| 17 | 18 | 8,000 | 109,200 | ||||

| 23 | 18 | 13,750 | 95,450 | ||||

| 29 | 19 | 1,700 | 93,750 | ||||

| 30 | 19 | 2,500 | 91,250 | ||||

| 31 | 19 | 2,000 | 93,250 | ||||

| 31 | 19 | 53,000 | 40,250 | ||||

| 31 | 19 | 7,500 | 32,750 | ||||

| 31 | 19 | 1,000 | 31,750 | ||||

| 31 | 19 | 5,000 | 36,750 | ||||

Table (3)

| Account: Accounts Receivable Account no. 12 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 100,100 | |||

| 3 | 18 | 83,900 | 16,200 | ||||

| 31 | 19 | 183,500 | 199,700 | ||||

Table (4)

| Account: Prepaid Insurance Account no. 13 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 12,600 | |||

| 5 | 18 | 12,000 | 24,600 | ||||

Table (5)

| Account: Office Supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 2,800 | |||

| 1 | 18 | 3,150 | 5,950 | ||||

| 9 | 18 | 400 | 5,550 | ||||

Table (6)

| Account: Land Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 31 | 19 | 75,000 | 75,000 | |||

Table (7)

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 21,000 | |||

| 1 | 18 | 3,150 | 24,150 | ||||

| 9 | 18 | 400 | 23,750 | ||||

| 23 | 18 | 13,750 | 10,000 | ||||

Table (8)

| Account: Unearned Rent Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 31 | 19 | 5,000 | 5,000 | |||

Table (9)

| Account: Notes Payable Account no. 23 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 31 | 19 | 67,500 | 67,500 | |||

Table (11)

| Account: Common stock Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 17,500 | |||

Table (12)

| Account: Retained earnings Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 70,000 | |||

Table (13)

| Account: Dividends Account no. 33 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 44,800 | |||

| 31 | 19 | 1,000 | 45,800 | ||||

Table (13)

| Account: Fees earned Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 591,500 | |||

| 31 | 19 | 183,500 | 775,000 | ||||

Table (14)

| Account: Salary and commission expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 385,000 | |||

| 31 | 19 | 2,000 | 383,000 | ||||

| 31 | 19 | 53,000 | 436,000 | ||||

Table (15)

| Account: Rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 49,000 | |||

| 2 | 18 | 7,200 | 56,200 | ||||

Table (16)

| Account: Advertising expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 32,200 | |||

| 17 | 18 | 8,000 | 40,200 | ||||

Table (17)

| Account: Automobile expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 15,750 | |||

| 30 | 19 | 2,500 | 18,250 | ||||

Table (19)

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| August | 1 | Balance | ✓ | 5,250 | |||

| 29 | 19 | 1,700 | 6,950 | ||||

Table (20)

(4)

To prepare: An unadjusted trial balance of Company V at August 31, 2018.

Explanation of Solution

Prepare an unadjusted trial balance of Company V at August 31, 2018 as follows:

|

Company V Unadjusted Trial Balance August 31, 2018 |

|||

| Particulars |

Account No. |

Debit $ | Credit $ |

| Cash | 11 | 36,750 | |

| Accounts receivable | 12 | 199,700 | |

| Prepaid insurance | 13 | 24,600 | |

| Office supplies | 14 | 5,550 | |

| Land | 16 | 75,000 | |

| Accounts payable | 21 | 10,000 | |

| Unearned rent | 22 | 5,000 | |

| Notes payable | 23 | 67,500 | |

| Common stock | 31 | 17,500 | |

| Retained earnings | 32 | 70,000 | |

| Dividends | 33 | 45,800 | |

| Fees earned | 41 | 775,000 | |

| Salaries and commission expense | 51 | 436,000 | |

| Rent expense | 52 | 56,200 | |

| Advertising expense | 53 | 40,200 | |

| Automobile expense | 54 | 18,250 | |

| Miscellaneous expense | 59 | 6,950 | |

| Total | 945,000 | 945,000 | |

Table (20)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $945,000.

(5) (a)

To explain: Whetherthe unadjusted trial balance in (4) balance

Explanation of Solution

The unadjusted trial balance in (4) would still balance, since the debit equalized the credit in the original journal entry.

(5) (b)

To journalize: The correcting entry

Explanation of Solution

The Correcting entry is as follows:

| Journal Page 19 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2018 | Dividends | 33 | 9,000 | ||

| August | 31 | Cash | 11 | 9,000 | |

| (To record the correcting entry) | |||||

Table (21)

Working notes:

(5) (c)

To identify: Whether the error made is a slide or transposition.

Explanation of Solution

The drawings account balance recorded as $10,000 instead of $1,000 is a slide error. Since, the decimal point of the amount has been misplaced.

Want to see more full solutions like this?

Chapter 2 Solutions

Bundle: Corporate Financial Accounting, Loose-leaf Version, 14th + LMS Integrated for CengageNOWv2, 1 term Printed Access Card

- The following facts perta lessee. non-cancelable lease agreement between Splish Brothers Leasing Company and Sunland Company Commencement date May 1, 2025 Annual lease payment due at the beginning of each year, beginning with May 1, 2025 $20.456.70 Bargain purchase option price at end of lease term $4,000 Lease term 5 years Economic life of leased equipment 10 years Lessor's cost $65,000 Fair value of asset at May 1, 2025 $98,000.20 Lessor's implicit rate 4% Lessee's incremental borrowing rate 4% The collectibility of the lease payments by Splish Brothers is probable. Prepare the journal entries to reflect the…arrow_forwardKarane Enterprises, a calendar-year manufacturer based in College Station, Texas, began business in 2023. In the process of setting up the business, Karane has acquired various types of assets. Below is a list of assets acquired during 2023: Asset Cost Date Placed in Service Office furniture $ 400,000 02/03 Machinery 1,810,000 07/22 Used delivery truck*Note: 90,000 08/17 *Note:Not considered a luxury automobile. During 2023, Karane was very successful (and had no §179 limitations) and decided to acquire more assets in 2024 to increase its production capacity. These are the assets acquired during 2024: Asset Cost Date Placed in Service Computers and information system $ 450,000 03/31 Luxury auto*Note: 92,500 05/26 Assembly equipment 1,200,000 08/15 Storage building 800,000 11/13 *Note:Used 100 percent for business purposes. Karane generated taxable income in 2024 of $1,795,000 for purposes of computing the §179 expense limitation. (Use MACRS Table 1, Table…arrow_forwardPearl Leasing Company agrees to lease equipment to Martinez Corporation on January 1, 2025. The following information relates to the lease agreement. 1. The term of the lease is 7 years with no renewal option, and the machinery has an estimated economic life of 9 years. 2. The cost of the machinery is $541,000, and the fair value of the asset on January 1, 2025, is $760,000. 3. Z At the end of the lease term, the asset reverts to the lessor and has a guaranteed residual value of $45,000, Maz estimates that the expected residual value at the end of the lease term will be $45,000. Martinez amortizes its leased equipment on a straight-line basis. 4. The lease agreement requires equal annual rental payments, beginning on January 1, 2025. 5. The collectibility of the lease payments is probable. 6. Pearl desires a 10% rate of return on its investments. Martinez's incremental borrowing rate is 11%, and the lessor's implicit rate is unknown. (Assume the accounting period ends on December 31.)…arrow_forward

- Financial accountingarrow_forwardButler Tech, Inc., is expanding into India. The company must decide where to locate and how to finance the expansion. Requirement Identify the financial statement where these decision makers can find the following information about Butler Tech, Inc. In some cases, more than one statement will report the needed data. Question content area bottom Part 1 Part 2 a. Revenue Income statement b. Common stock Balance sheet c. Current liabilities Balance sheet d. Long-term debt Balance sheet e. Dividends Statement of retained earnings and Statement of cash flows f. Ending cash balance Balance sheet and Statement of cash flows g. Adjustments to reconcile net income to net cash provided by operations Statement of cash flows h. Cash spent to acquire the building i. Income tax expense j. Ending balance of retained earnings k. Selling,…arrow_forwardWhat is the depreciation expense in 2015 ??arrow_forward

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning- Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning