Financial Accounting

14th Edition

ISBN: 9781305088436

Author: Carl Warren, Jim Reeve, Jonathan Duchac

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 2, Problem 23E

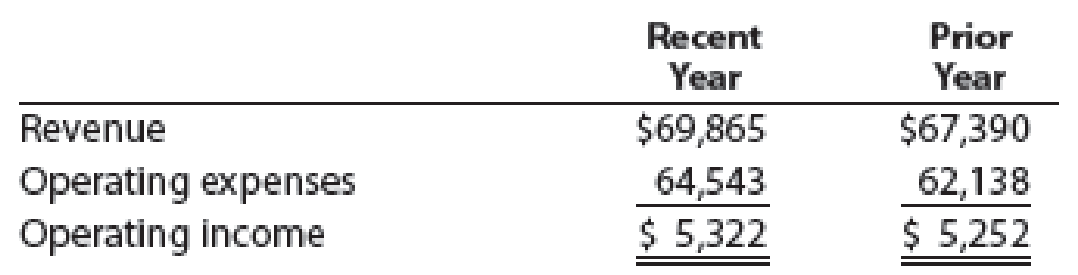

The following data (in millions) are taken from the financial statements of Target Corporation:

- a. For Target Corporation, determine the amount of change in millions and the percent of change (round to one decimal place) from the prior year to the recent year for:

1. Revenue

2. Operating expenses

3. Operating income

- b. What conclusions can you draw from your analysis of the revenue and the total operating expenses?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

I am trying to find the accurate solution to this financial accounting problem with appropriate explanations.

Can you show me the correct approach to solve this financial accounting problem using suitable standards?

Can you help me with General accounting question?

Chapter 2 Solutions

Financial Accounting

Ch. 2 - What is the difference between an account and a...Ch. 2 - Prob. 2DQCh. 2 - Prob. 3DQCh. 2 - eCatalog Services Company performed services in...Ch. 2 - If the two totals of a trial balance are equal,...Ch. 2 - Assume that a trial balance is prepared with an...Ch. 2 - Assume that when a purchase of supplies of 2,650...Ch. 2 - Assume that Muscular Consulting erroneously...Ch. 2 - Assume that Sunshine Realty Co. borrowed 300,000...Ch. 2 - Checking accounts are a common form of deposits...

Ch. 2 - State for each account whether it is likely to...Ch. 2 - State for each account whether it is likely to...Ch. 2 - Prob. 2PEACh. 2 - Prob. 2PEBCh. 2 - Prepare a journal entry on March 16 for fees...Ch. 2 - Prepare a journal entry on August 13 for cash...Ch. 2 - Prepare a journal entry on December 23 for the...Ch. 2 - Prepare a journal entry on June 30 for the...Ch. 2 - Prob. 5PEACh. 2 - On August 1, the supplies account balance was...Ch. 2 - For each of the following errors, considered...Ch. 2 - For each of the following errors, considered...Ch. 2 - The following errors took place in journalizing...Ch. 2 - The following errors took place in journalizing...Ch. 2 - Prob. 8PEACh. 2 - Two income statements for Paragon Company follow:...Ch. 2 - The following accounts appeared in recent...Ch. 2 - Innerscape Interiors is owned and operated by...Ch. 2 - LeadCo School is a newly organized business that...Ch. 2 - The following table summarizes the rules of debit...Ch. 2 - During the month, Gates Labs Co. has a substantial...Ch. 2 - Identify each of the following accounts of Kaiser...Ch. 2 - Jardine Consulting Co. has the following accounts...Ch. 2 - On January 7, 2016, Captec Company purchased 4,175...Ch. 2 - The following selected transactions were completed...Ch. 2 - During the month, Warwick Co. received 515,000 in...Ch. 2 - a. During February, 186,500 was paid to creditors...Ch. 2 - As of January 1, Terrace Waters, Capital had a...Ch. 2 - Wyoming Tours Co. is a travel agency. The nine...Ch. 2 - Based upon the T accounts in Exercise 2-13,...Ch. 2 - Based upon the data presented in Exercise 2-13,...Ch. 2 - The accounts in the ledger of Hickory Furniture...Ch. 2 - Indicate which of the following errors, each...Ch. 2 - The following preliminary unadjusted trial balance...Ch. 2 - The following errors occurred in posting from a...Ch. 2 - Identify the errors in the following trial...Ch. 2 - The following errors took place in journalizing...Ch. 2 - The following errors took place in journalizing...Ch. 2 - The following data (in millions) are taken from...Ch. 2 - Prob. 24ECh. 2 - Kimberly Manis, an architect, opened an office on...Ch. 2 - On August 1, 2016, Bill Hudson established...Ch. 2 - On November 1, 2016, Patty Cosgrove established an...Ch. 2 - Elite Realty acts as an agent in buying, selling,...Ch. 2 - The Colby Group has the following unadjusted trial...Ch. 2 - Ken Jones, an architect, opened an office on April...Ch. 2 - On August 1, 2016, Rafael Masey established Planet...Ch. 2 - On October 1, 2016, Jay Pryor established an...Ch. 2 - Prob. 4PBCh. 2 - Tech Support Services has the following unadjusted...Ch. 2 - The transactions completed by PS Music during June...Ch. 2 - At the end of the current month, Gil Frank...Ch. 2 - Prob. 2CPCh. 2 - The following discussion took place between Tony...Ch. 2 - Prob. 5CP

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Please explain the solution to this general accounting problem with accurate explanations.arrow_forwardI am searching for the accurate solution to this financial accounting problem with the right approach.arrow_forwardPlease explain the correct approach for solving this general accounting question.arrow_forward

- Zebrix Ltd. has an inventory period of 55 days, an accounts receivable period of 10 days, and an accounts payable period of 6 days. The company's annual sales are $208,400. How many times per year does the company turn over its accounts receivable?arrow_forwardLika company issues 2,000 shares of $10 par value common stock for $25 per share. What amount should be credited to the Common Stock account and to the Additional Paid-in Capital account?arrow_forwardCan you help me solve this general accounting question using the correct accounting procedures?arrow_forward

- Can you solve this general accounting question with accurate accounting calculations?arrow_forwardPlease provide the correct answer to this general accounting problem using accurate calculations.arrow_forwardI need help solving this general accounting question with the proper methodology.arrow_forward

- I need help finding the accurate solution to this general accounting problem with valid methods.arrow_forwardPlease provide the answer to this financial accounting question using the right approach.arrow_forwardCan you explain this general accounting question using accurate calculation methods?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Financial Accounting

Accounting

ISBN:9781337272124

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

College Accounting (Book Only): A Career Approach

Accounting

ISBN:9781337280570

Author:Scott, Cathy J.

Publisher:South-Western College Pub

Financial Accounting

Accounting

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:9781305961883

Author:Carl Warren

Publisher:Cengage Learning

How To Analyze an Income Statement; Author: Daniel Pronk;https://www.youtube.com/watch?v=uVHGgSXtQmE;License: Standard Youtube License