Videos

Analyzing a Quality Cost Report LO1—8

Mercury, Inc., produces cell phones at its plant in Texas. In recent years, the company’s market share has been eroded by stiff competition from overseas. Price and product quality are the two key areas in which companies compete in this market.

A year ago, the company’s cell phones had been ranked low in product quality in a consumer survey. Shocked by this result, Jorge Gomez, Mercury’s president, initiated an intense effort to improve product quality. Gomez set up a task force to implement a formal quality improvement program. Included on this task force were representatives from the Engineering. Marketing. Customer Service. Production, and Accounting departments. The broad representation was needed because Gomez believed that this was a companywide program and that all employees should share the responsibility for its success.

After the first meeting of the task force, Holly Elsoe, manager of the Marketing Department, asked John Tran, production manager, what he thought of the proposed program. Tran replied. "I have reservations. Quality is too abstract to be attaching costs to it and then to be holding you and me responsible for cost improvements. I like to work with goals that I can see and count! I’m nervous about having my annual bonus based on a decrease in quality costs; there are too many variables that we have no control over.”

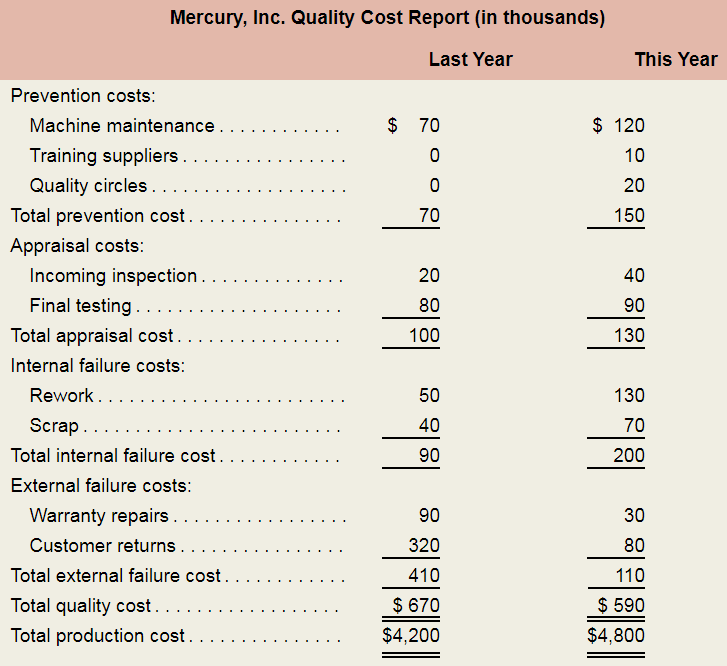

Mercury’s quality improvement program has now been in operation for one year. The company’s most recent quality cost report is shown below.

As they were reviewing the report, Elsoe asked Tran what he now thought of the quality improvement program. Tran replied. “I’m relieved that the new quality improvement program hasn’t hurt our bonuses, but the program has increased the workload in the Production Department. It is true that customer returns are way down, but the cell phones that were returned by customers to retail outlets were rarely sent back to us for rework.”

Required:

- Expand the company’s quality cost report by showing the costs in both years as percentages of both total production cost and total quality cost. Carry all computations to one decimal place. By analyzing the report, determine if Mercury, Inc.’s quality improvement program has been successful. List specific evidence to support your answer.

- Do you expect the improvement program as it progresses to continue to increase the workload in the Production Department?

- Jorge Gomez believed that the quality improvement program was essential and that Mercury. Inc., could no longer afford to ignore the importance of product quality. Discuss how Mercury? Inc., could measure the cost of nor implementing the quality improvement program. (CMA, adapted)

Want to see the full answer?

Check out a sample textbook solution

Chapter 1A Solutions

MANAGERIAL ACCOUNTING F/MGRS.

- Nobel Corp. uses a predetermined overhead rate based on direct labor cost to apply manufacturing overhead to jobs. For the year ended December 31, Nobel's estimated manufacturing overhead was $800,000, based on an estimated volume of 40,000 direct labor hours, at a direct labor rate of $8.00 per hour. Actual manufacturing overhead amounted to $850,000, with an actual direct labor cost of $360,000. For the year, what was manufacturing overhead?arrow_forwardWhat is it's PE ratio on these financial accounting question?arrow_forwardGeneral Accountingarrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,