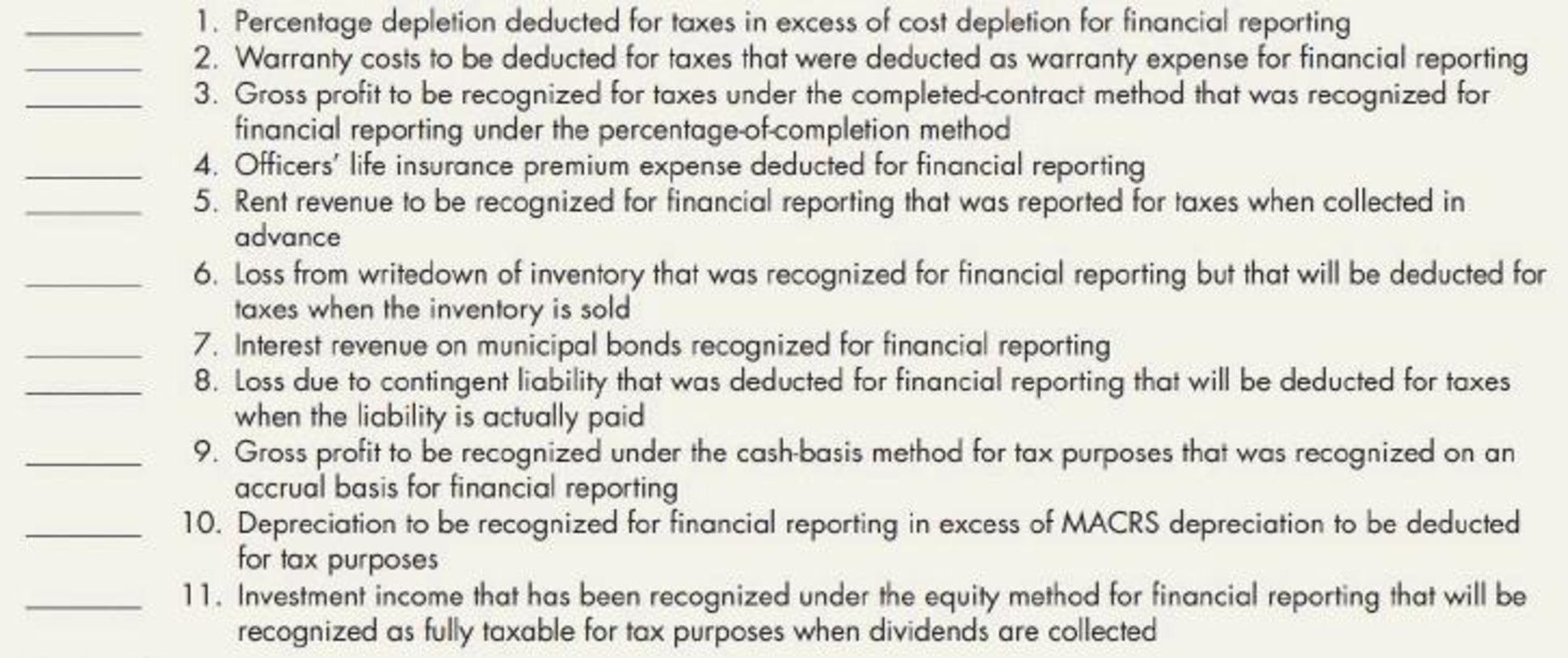

Temporary and Permanent Differences In the current year, you are calculating a diversified company’s deferred taxes. Based on an analysis of the company’s current taxable income and pretax financial income, you have identified the following items that create differences between the two amounts and that may result in differences between the company’s future taxable income and its nature pretax financial income: Required: For each difference, indicate whether it is a temporary difference ( T ) or a permanent difference ( P ) by placing the appropriate letter on the line provided. If the difference is a temporary difference, also indicate for the current year whether it will result in a future taxable amount ( FT ) or a future deductible amount ( FD ).

Temporary and Permanent Differences In the current year, you are calculating a diversified company’s deferred taxes. Based on an analysis of the company’s current taxable income and pretax financial income, you have identified the following items that create differences between the two amounts and that may result in differences between the company’s future taxable income and its nature pretax financial income: Required: For each difference, indicate whether it is a temporary difference ( T ) or a permanent difference ( P ) by placing the appropriate letter on the line provided. If the difference is a temporary difference, also indicate for the current year whether it will result in a future taxable amount ( FT ) or a future deductible amount ( FD ).

Temporary and Permanent Differences In the current year, you are calculating a diversified company’s deferred taxes. Based on an analysis of the company’s current taxable income and pretax financial income, you have identified the following items that create differences between the two amounts and that may result in differences between the company’s future taxable income and its nature pretax financial income:

Required:

For each difference, indicate whether it is a temporary difference (T) or a permanent difference (P) by placing the appropriate letter on the line provided. If the difference is a temporary difference, also indicate for the current year whether it will result in a future taxable amount (FT) or a future deductible amount (FD).

Definition Definition Estimated future tax made while preparing accounts. Deferred tax is estimated based on past and present transactions from financial statements. It is not the actual tax that needs to be paid or is refundable from the revenue authority; it is an accounting entry. It is necessary to account for deferred tax due to difference between accounting profits and taxable profits.

Coronado Fire, Inc. manufactures steel cylinders and nozzles for two models of fire extinguishers: (1) a home fire extinguisher and (2) a

commercial fire extinguisher. The home model is a high-volume (54,000 units), half-gallon cylinder that holds 2 1/2 pounds of multi-

purpose dry chemical at 480 PSI. The commercial model is a low-volume (10,200 units), two-gallon cylinder that holds 10 pounds of

multi-purpose dry chemical at 390 PSI. Both products require 1.5 hours of direct labor for completion. Therefore, total annual direct

labor hours are 96,300 or [1.5 hours x (54,000+ 10,200)]. Estimated annual manufacturing overhead is $1,566,090. Thus, the

predetermined overhead rate is $16.26 or ($1,566,090 ÷ 96,300) per direct labor hour. The direct materials cost per unit is $18.50 for

the home model and $26.50 for the commercial model. The direct labor cost is $19 per unit for both the home and the commercial

models.

The company's managers identified six activity cost pools and related…

The completed Payroll Register for the February and March biweekly pay periods is provided, assuming benefits went into effect as anticipated.

Required:

Using the payroll registers, complete the General Journal entries as follows:

February 10 Journalize the employee pay.

February 10 Journalize the employer payroll tax for the February 10 pay period. Use 5.4 percent SUTA and 0.6 percent FUTA. No employees will exceed the FUTA or SUTA wage base.

February 14 Issue the employee pay.

February 24 Journalize the employee pay.

February 24 Journalize the employer payroll tax for the February 24 pay period. Use 5.4 percent SUTA and 0.6 percent FUTA. No employee will exceed the FUTA or SUTA wage base.

February 28 Issue the employee pay.

February 28 Issue payment for the payroll liabilities.

March 10 Journalize the employee pay.

March 10 Journalize the employer payroll tax for the March 10 pay period. Use 5.4 percent SUTA and 0.6 percent FUTA. No employees will exceed the FUTA or SUTA wage base.…

Please given step by step explanation general accounting question

Operations Management: Processes and Supply Chains (12th Edition) (What's New in Operations Management)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT