Concept explainers

Videos

Variance Computations with Missing Data

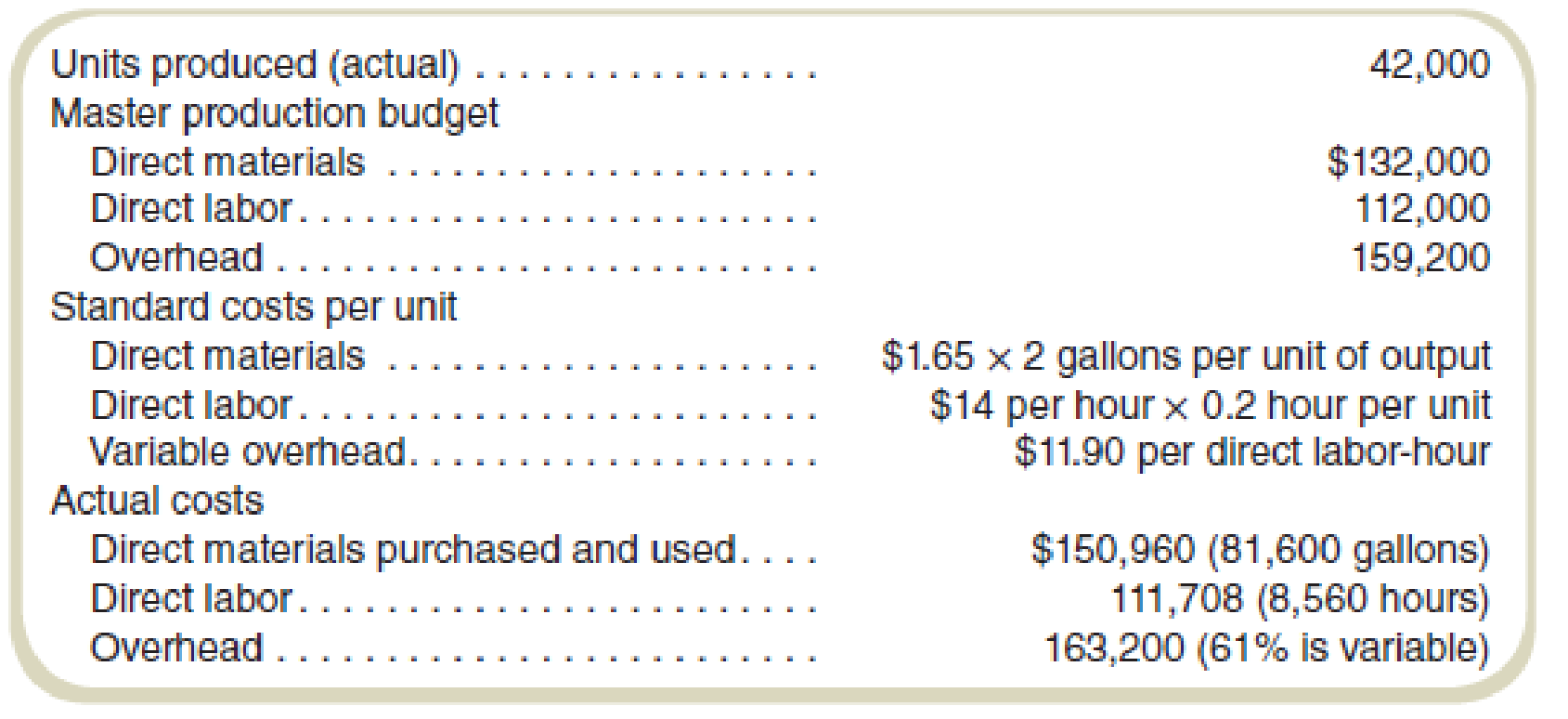

The following information is provided to assist you in evaluating the performance of the production operations of Studio Company:

Variable

Required

Prepare a report that shows all variable production cost price and efficiency variances and fixed production cost price and production volume variances.

Prepare a report showing variable production cost price and efficiency variances along with fixed production cost price and production volume variances.

Explanation of Solution

Price variance:

The price variance refers to the difference of the actual unit cost and standard unit cost of the product.

Efficiency variance:

The efficiency variance refers to the difference of the actual and budgeted quantities which have been purchased for a specific price.

Variable production cost will include direct material, direct labor, and variable overhead costs so price and efficiency variances will be computed for all three components. For fixed overhead cost variances with variable cost; price and production volume variances need to be calculated.

Compute the variable production cost variances:

For preparing variable product cost variance report, following missing components needs to be calculated first.

Standard Units Produced:

Actual direct material unit cost:

Actual labor cost per unit:

Standard total labor hours:

Actual variable overhead per actual labor hour:

The report showing variable production cost price and efficiency variances:

| Direct Material Variances | Amount |

| Price Variance | $16,320 |

| Efficiency Variance | $2,6400 |

| Total Variance | $18,960F |

| Direct Labor Variances | |

| Price Variance | $8,132 |

| Efficiency Variance | $7,840 |

| Total Variance | $2,92F |

| Variable Overhead Variance: | |

| Price Variance | $2,311 |

| Efficiency Variance | $6,664 |

| Total Variance | $4,353U |

Table: (1)

Compute the fixed overhead cost variance:

For calculating fixed production cost price and production volume variances, standard fixed overhead cost and fixed overhead applied to production need to be calculated.

Standard fixed overhead cost:

Applied fixed overhead to production:

The report showing fixed overhead cost variance with price and production volume variances:

| Fixed Overhead Variance | Amount |

| Price Variance | $ 1,280 |

| Production Volume Variance | $ 3,200 |

| Total Variance | $1,920F |

Table: (2)

Fixed overhead cost price variance is unfavorable being actual is more than the standard fixed overhead whereas production volume variance is favorable as applied fixed overhead to actual production is less than the budgeted.

Want to see more full solutions like this?

Chapter 16 Solutions

GEN COMBO FUNDAMENTALS OF COST ACCOUNTING; CONNECT 1S ACCESS CARD

- Fairfield Company's payroll costs for the most recent month are summarized here: Item Hourly labor unges Description 920 hours $27 per hour 190 hours for Job 101 340 hours for Job 102 Factory supervision Production engineer Factory Janitorial work Selling, general, and administrative salaries Total payroll costs Required: 390 hours for Job 103 Total Cost $ 5,130 9,180 10,530 $ 24,840 4,350 7,100 1,200 8,800 $ 46,298 1. & 2. Prepare the journal entries for payroll and to apply manufacturing overhead to production. The company applies manufacturing overhead to products at a predetermined rate of $54 per direct labor hour Note: If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. View transaction list Journal entry worksheet A B Record Fairfield Company's payroll costs to be paid at a later date. Note Enter debits before credits. S.No Date 1 Account Title Debit Creditarrow_forwardNo wrong answerarrow_forwardL.L. Bean operates two factories that produce its popular Bean boots (also known as "duck boots") in its home state of Maine. Since L.L. Bean prides itself on manufacturing its boots in Maine and not outsourcing, backorders for its boots can be high. In 2014, L.L. Bean sold about 450,000 pairs of the boots. At one point during 2014, it had a backorder level of about 100,000 pairs of boots. L.L. Bean can manufacture about 2,200 pairs of its duck boots each day with its factories running 24/7. In 2015, L.L. Bean expects to sell more than 500,000 pairs of its duck boots. As of late November 2015, the backorder quantity for Bean Boots was estimated to be about 50,000 pairs. Question: Now assume that 5% of the L.L. Bean boots are returned by customers for various reasons. L. Bean has a 100% refund policy for returns, no matter what the reason. What would the journal entry be to accrue L.L. Bean's sales returns for this one pair of boots?arrow_forward

- The following data were taken from the records of Splish Brothers Company for the fiscal year ended June 30, 2025. Raw Materials Inventory 7/1/24 $58,100 Accounts Receivable $28,000 Raw Materials Inventory 6/30/25 46,600 Factory Insurance 4,800 Finished Goods Inventory 7/1/24 Finished Goods Inventory 6/30/25 99,700 Factory Machinery Depreciation 17,100 21,900 Factory Utilities 29,400 Work in Process Inventory 7/1/24 21,200 Office Utilities Expense 9,350 Work in Process Inventory 6/30/25 29,400 Sales Revenue 560,500 Direct Labor 147,550 Sales Discounts 4,700 Indirect Labor 25,360 Factory Manager's Salary 63,400 Factory Property Taxes 9,910 Factory Repairs 2,500 Raw Materials Purchases 97,300 Cash 39,200 SPLISH BROTHERS COMPANY Income Statement (Partial) $arrow_forwardNo AIarrow_forwardL.L. Bean operates two factories that produce its popular Bean boots (also known as "duck boots") in its home state of Maine. Since L.L. Bean prides itself on manufacturing its boots in Maine and not outsourcing, backorders for its boots can be high. In 2014, L.L. Bean sold about 450,000 pairs of the boots. At one point during 2014, it had a backorder level of about 100,000 pairs of boots. L.L. Bean can manufacture about 2,200 pairs of its duck boots each day with its factories running 24/7.In 2015, L.L. Bean expects to sell more than 500,000 pairs of its duck boots. As of late November 2015, the backorder quantity for Bean Boots was estimated to be about 50,000 pairs. Question: Assume that a pair of 8" Bean Boots are ordered on December 3, 2015. The order price is $109. The sales tax rate in the state in which the boots are order is 7%. L.L. Bean ships the boots on January 29, 2016. Assume same-day shipping for the sake of simplicity. On what day would L.L. Bean recognize the…arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College