Videos

(A)

To Compute:

If the desired put option were traded. How much would it cost to purchase?

Introduction:

The value of put option is calculated using the formula given below.

Explanation of Solution

a) Computation of value of put:

Here, the investor would hold a put position. The current price is $100. This price could either

increase or decrease by 10%

Factor by which stock increases is u

Factor by which stock decreases is d

Calculation of option value

The two possible stock prices are

since, the exercise price is $100, and the corresponding two possible put values are

Calculation of the hedge ratio (H)

The hedge ratio can be calculated by using the following formula:

Here,

The value of the call option in case of in-the-money scenario is

The value of the call option in case of out-of-the-money scenario is

Factor by which stock increases u.

Factor by which stock decreases is d.

Stock price in case stock price increases is

Stock price in case stock price decreases is

Substitute:

Hence, the hedge ratio is -.5

The portfolio combining of two puts and one share brings an assured payoff $ 110 making it a riskless portfolio.

Calculation of the present value of certain stock price of $110 with a one-year interest rate of 5%:

Hence, the present value of certain stock price of $110 with a one-year interest rate of 5% $104.76

Comparing the protective put strategy and present value of stock we get,

One stock and two put options

Solve for the value of put (P):

Hence, the value of put option is $2.38.

Hence, the value of put option is $2.38.

(B)

To Compute:

What would have been the cost of the protective put portfolio? Introduction: The cost of protective put portfolio that comes out is calculated based on the given formula below.

Explanation of Solution

(b) Computation of cost of protective put portfolio:

The cost of the protective put portfolio is the cost of one share plus the cost of one put. It

can be calculated by using the following formula:

Hence, the cost of protective put portfolio comes out to be $102.38.

Hence, the cost of protective put portfolio comes out to be $102.38.

(C)

To Compute:

What portfolio position in stock and T-bills ill ensure you a payoff equal to the payoff that would be provided by a protective put with X-$100? Show that the payoff to this portfolio and

the cost of establishing the portfolio match those of the desired protective put.

Introduction:

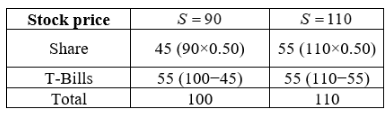

The strategy is calculated in the table to determine the pay-off using the below calculation.

Explanation of Solution

To ensure equal pay-off in stock and T-bills and protective put is as follows

The hedge ratio is 0.50. The investor will invest 0.50 in stocks which costs $50 and

remaining in T-bills to earn 5% interest.

The above strategy will give same pay-off as the protective put option.

The above strategy will give same pay-off as the protective put option.

Want to see more full solutions like this?

Chapter 16 Solutions

ESSEN.OF.INVESTMENTS+CONNECT

- Hilton Hotels Corporation has a convertible bond issue outstanding. Each bond, with a face value of $1,000, can be converted into common shares at a rate of 61.2983 shares of stock per $1,000 face value bond (the conversion rate), or $16.316 per share. Hilton’s common stock is trading (on the NYSE) at $15.90 per share and the bonds are trading at $975. a. Calculate the conversion value of each bond. (Round your answer to 2 decimal places. (e.g., 32.16)). (974.50 was wrong)arrow_forwardConsider an investor who, on January 1, 2022, purchases a TIPS bond with an original principal of $100,000, an 8 percent annual (or 4 percent semiannual) coupon rate, and 10 years to maturity. If the semiannual inflation rate during the first six months is 0.3 percent, calculate the principal amount used to determine the first coupon payment and the first coupon payment (paid on June 30, 2022). From your answer to part a, calculate the inflation-adjusted principal at the beginning of the second six months. Suppose that the semiannual inflation rate for the second six-month period is 1 percent. Calculate the inflation-adjusted principal at the end of the second six months (on December 31, 2022) and the coupon payment to the investor for the second six-month period.arrow_forwardA municipal bond you are considering as an investment currently pays a yield of 6.75 percent. Calculate the tax-equivalent yield if your marginal tax rate is 28 percent. Calculate the tax-equivalent yield if your marginal tax rate is 21 percent.arrow_forward

- Suppose three countries’ per capita Gross Domestic Products (GDPs) are £1000, £2000, and £3000. What is the average of each pair of countries’ GDPs per capita? (b) What is the difference between each of the individual observations and the overall average? What is the sum of these differences? (c) Suppose instead of three countries, we had a sample of 100 countries with the same sample average GDP per capita as the overall average for the three observations above, with the standard deviation of these 100 observations being £1000. Form the 95% confidence interval for the population mean. (d) What might explain differences in GDP across countries? Consider the following regression equation, where Earnings is measured in £/hour, and Experience is measured in years in a particular job, with standard errors in parentheses: Earnings \ = −0.25 (−0.5) + 0.2 (0.1) Experience, One of these numbers has been reported incorrectly - it shouldn’t be negative. Which one and why? (b)…arrow_forwardI need answer typing clear urjent no chatgpt used pls i will give 5 Upvotes.arrow_forwardYou want to buy equipment that is available from 2 companies. The price of the equipment is the same for both companies. Silver Research would let you make quarterly payments of $9,130 for 3 years at an interest rate of 3.27 percent per quarter. Your first payment to Silver Research would be today. Island Research would let you make monthly payments of $3,068 for 3 years at an interest rate of X percent per month. Your first payment to Island Research would be in 1 month. What is X? Input instructions: Input your answer as the number that appears before the percentage sign. For example, enter 9.86 for 9.86% (do not enter .0986 or 9.86%). Round your answer to at least 2 decimal places. percentarrow_forward

- Make sure you're using the right formula and rounding correctly I have asked this question four times and all the answers have been incorrect.arrow_forwardYou plan to retire in 3 years with $911,880. You plan to withdraw $X per year for 18 years. The expected return is 18.56 percent per year and the first regular withdrawal is expected in 3 years. What is X? Input instructions: Round your answer to the nearest dollar. $arrow_forwardPlease make sure you're using the right formula and rounding correctly I have asked this question four times and all the answers have been incorrect.arrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education