Videos

(A)

Adequate Information:

The

To calculate:

The fraction of the portfolio, fraction in equity and the stock portfolio if falls by 3%.

Introduction:

Portfolio involves financial asset grouping viz. currencies, commodities, bonds, stocks and cash equivalents. It also comprises of fund counterparts such as closed funds, exchange traded funds and mutual funds. Non-publicly tradable securities such as private, art and real estate investment are also part of portfolios.

Explanation of Solution

Fractions of portfolio invested in T-bills and equity can be calculated based on the Black-Scholes

model. The value of

to T-bills and equity can be known for value of

Formula for

Substitute values to calculate

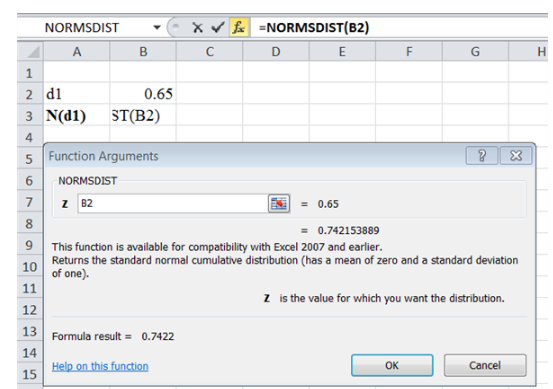

Calculate the Black-Scholes hedge ratio

"NORMSDIST" function are as follows:

- First, go to the Menu bar of Excel and select 'Formulas' option

- Select Insert Function '(fx)

- Then select a category as Financial

- Then select "NORMSDIST" and click OK

- Then the Function Argument window will open. Now, input the given data in the required field

- Click OK

- The formula will display the final answer as 0.7422

Therefore,

Calculate the put delte as follows:

Hence, place 25.785 of the portfolio in T-bills and 74.22%

Hence, place 25.785 of the portfolio in T-bills and 74.22%

(B)

Adequate information:

To calculate:

Fractions of portfolio divided into bills and equity If stock prices fall by 3% on the first day of trading. It means

Introduction:

Portfolio involves financial asset grouping viz. currencies, commodities, bonds, stocks and cash equivalents. It also comprises of fund counterparts such as closed funds, exchange traded funds and mutual funds. Non-publicly tradable securities such as private, art and real estate investment are also part of portfolios.

Explanation of Solution

Fractions of portfolio invested in T-bills and equity can be calculated based on the Black-Scoles model. The value of

Substitute values to calculate

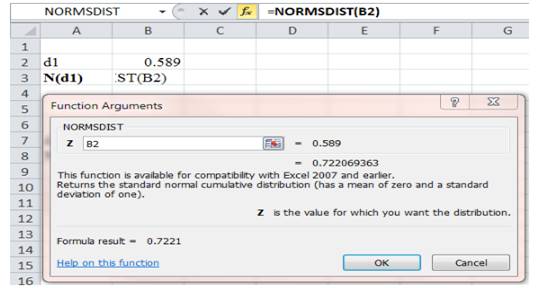

Calculate the Black-Scholes hedge ratio

Hence,

Calculate the put delta as follows:

Hence, place 27.79% of the portfolio in T-bills and 72.21%

Want to see more full solutions like this?

Chapter 16 Solutions

ESSENTIALS OF INVESTMENTS SELECT CHAPT

- Use the right formula and rounding correctly I have asked this question four times and all the answers have been incorrect.arrow_forwardWhat is the origin of Biblical ethics and how researchers can demonstrate Biblical ethics? How researchers can demonstrate Biblical ethics when conducting a literaturereview? How researchers can demonstrate Biblical ethics when communicating with aresearch team or university committee?arrow_forwardEquipment is worth $339,976. It is expected to produce regular cash flows of $50,424 per year for 18 years and a special cash flow of $75,500 in 18 years. The cost of capital is X percent per year and the first regular cash flow will be produced today. What is X? Input instructions: Input your answer as the number that appears before the percentage sign. For example, enter 9.86 for 9.86% (do not enter 0986 or 9.86%). Round your answer to at least 2 decimal places. percentarrow_forward

- You want to buy equipment that is available from 2 companies. The price of the equipment is the same for both companies. Silver Leisure would let you make quarterly payments of $3,530 for 7 years at an interest rate of 2.14 percent per quarter. Your first payment to Silver Leisure would be today. Pond Leisure would let you make X monthly payments of $18,631 at an interest rate of 1.19 percent per month. Your first payment to Pond Leisure would be in 1 month. What is X? Input instructions: Round your answer to at least 2 decimal places.arrow_forwardYou plan to retire in 4 years with $659,371. You plan to withdraw $100,000 per year for 12 years. The expected return is X percent per year and the first regular withdrawal is expected in 4 years. What is X? Input instructions: Input your answer as the number that appears before the percentage sign. For example, enter 9.86 for 9.86% (do not enter .0986 or 9.86%). Round your answer to at least 2 decimal places. percentarrow_forwardYou want to buy equipment that is available from 2 companies. The price of the equipment is the same for both companies. Gray Media would let you make quarterly payments of $1,430 for 7 years at an interest rate of 1.59 percent per quarter. Your first payment to Gray Media would be today. River Media would let you make monthly payments of $X for 8 years at an interest rate of 1.46 percent per month. Your first payment to River Media would be in 1 month. What is X? Input instructions: Round your answer to the nearest dollar.arrow_forward

- You plan to retire in 8 years with $X. You plan to withdraw $114,200 per year for 21 years. The expected return is 17.92 percent per year and the first regular withdrawal is expected in 9 years. What is X? Input instructions: Round your answer to the nearest dollar. SAarrow_forward69 You plan to retire in 3 years with $911,880. You plan to withdraw $X per year for 18 years. The expected return is 18.56 percent per year and the first regular withdrawal is expected in 3 years. What is X? Input instructions: Round your answer to the nearest dollar.arrow_forwardYou plan to retire in 7 years with $X. You plan to withdraw $54,100 per year for 15 years. The expected return is 13.19 percent per year and the first regular withdrawal is expected in 7 years. What is X? Input instructions: Round your answer to the nearest dollar.arrow_forward

- You want to buy equipment that is available from 2 companies. The price of the equipment is the same for both companies. Orange Furniture would let you make quarterly payments of $12,540 for 6 years at an interest rate of 1.26 percent per quarter. Your first payment to Orange Furniture would be in 3 months. River Furniture would let you make X monthly payments of $41,035 at an interest rate of 0.73 percent per month. Your first payment to River Furniture would be today. What is X? Input instructions: Round your answer to at least 2 decimal places.arrow_forwardLet y(t) represent your retirement account balance, in dollars, after t years. Each year the account earns 7% interest, and you deposit 8% of your annual income. Your current annual income is $34000, but it is growing at a continuous rate of 2% per year. Write the differential equation modeling this situation. dy dtarrow_forwardYou want to buy equipment that is available from 2 companies. The price of the equipment is the same for both companies. Silver Research would let you make quarterly payments of $9,130 for 3 years at an interest rate of 3.27 percent per quarter. Your first payment to Silver Research would be today. Island Research would let you make monthly payments of $3,068 for 3 years at an interest rate of X percent per month. Your first payment to Island Research would be in 1 month. What is X? Input instructions: Input your answer as the number that appears before the percentage sign. For example, enter 9.86 for 9.86% (do not enter .0986 or 9.86%). Round your answer to at least 2 decimal places. percentarrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education