Videos

(Optimal Provision of Public Goods) Using at least two individual consumers, show how the market

the market demand curve is to be derived from individual demand curves for a private goods and for a public good and then introduce the market supply curve and show the optimal level of production.

Concept Introduction:

A demand curve is a graph that shows the change in quantity demanded of a good or service with respect to its price. With change in price the demand also change and it carries an inverse relationship with the price. Market demand refers to the demand of a good in a particular market that adds up to a sum of different individual demands.

Explanation of Solution

Individual demand curves adds up to make a market demand curve for a good. It is a broader term that defines demand of a particular good at a much larger scale.

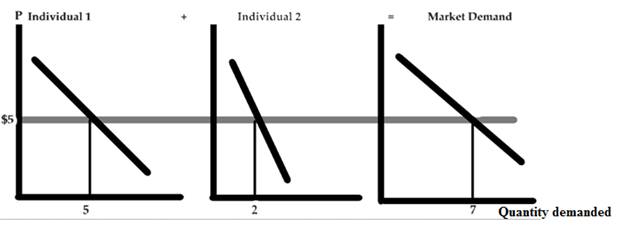

a. For a private good: Private good refers to the good that needs to be purchased from the private individual and its consumption by one individual prevents it to be consumed from the other individuals.

In the above figure there are three curves, where curve 1 is the individual demand curve for a good at price $5 and quantity 5 units. The second curve represents the individual demand curve for the same good at same price but the quantity is 2. The third curve is the market demand curve which is the summation of curve 1 of individual 1 and curve 2 of individual 2 at price $5 same as before. The market demand curve is the summation of curve 1 and curve 2 therefore the quantity for the same is 5 + 2 = 7 units.

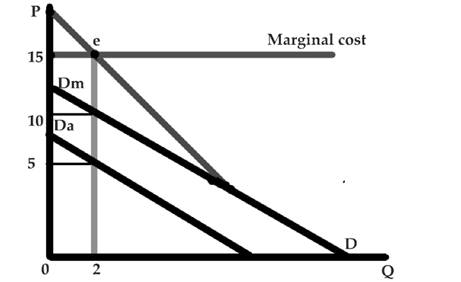

b. For public good: A public good is a good which is provided to all the members of the society without profit, it is provided by the government, individual or an organization. The consumption of such good doesn’t affect the consumption for others.

Public good once produced is available to all people and in identical amounts. Hence the demand for the public good is the vertical summation of each individuals demand. The marginal cost here equals the marginal benefits at e where the market demand curve and the marginal cost curve are at equilibrium. The red line on the graph represent the market demand curve and the blue line defines the marginal cost curve. Dm and Da are respectively the two individual demand curves which add up vertically with quantity being constant to make the market demand curve.

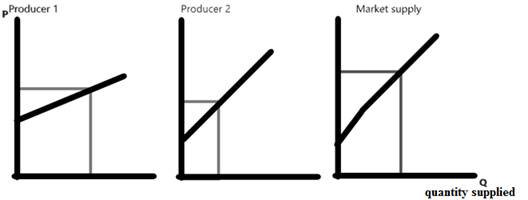

The market supply curve is an upward sloping curve which shows a positive relationship between the price and the quantity supplied. The summation of the individuals producers supply makes the market supply curve.

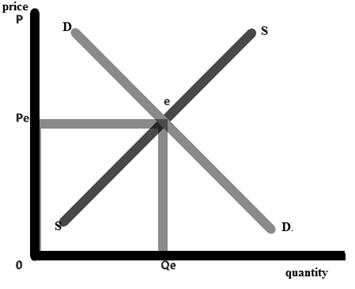

The optimal level of production is the point where the market demand is equal to that of the market supply and that level of intersection is called the market demand.

Want to see more full solutions like this?

Chapter 16 Solutions

Mindtap Economics, 1 Term (6 Months) Printed Access Card For Mceachern's Econ Micro 6

- This Wendy’s commercial confuses the notions of appreciation and consumer surplus. Recall that consumer surplus is the difference between what a consumer is willing to pay for a good and what they actually pay for it. According to standard economic theory, consumer surplus must always bearrow_forwardIn economics, the cost of producing a good: Question 6 options: is the maximum value of other goods that could have been produced using the same resources. equals the out-of-pocket costs incurred in producing the good. is the value of inputs used up in production. is the value of other goods that could have been produced using the same resources.arrow_forwardPlease correct answer and don't used hand raiting and don't used Ai solutionarrow_forward

- not use ai pleasearrow_forwardGates Doubles Down on Malaria Eradication The End Malaria Council, convened by Bill Gates and Ray Chambers, seeks to mobilize resources to prevent and treat malaria. The current level of financing is too low to end malaria. Bruno Moonen, deputy director for malaria at the Gates Foundation, says that more resources, more leadership, and new technologies are needed to eradicate malaria in the current generation. Is Bruno Moonen talking about production efficiency or allocative efficiency or both? Bruno Moonen is talking about _______. A. production efficiency but not allocative efficiency B. production efficiency and allocative efficiency C. allocative efficiency but not production efficiency D. neither production efficiency nor allocative efficiencyarrow_forwardWhat challenges do medical facilities face when trying to become more culturally competent? What kinds of assumptions do providers sometimes make about people from other cultures? What factors may cause providers to relate to patients in a biased manner? What can healthcare organizations do to ensure cultural competence among their employees?arrow_forward

- Brazil, Russia, India, China, and South Africa, also known as BRICS, are emerging countries poised to be dominant economic players in the 21st century. What are some of the political, legal and economic conditions that help or hinder economic expansion for these countries?arrow_forwardExplain what is Microeconomics? Why is it important for all of us to understand what are the drivers in microeconomics?arrow_forwardThe production function for a product is given by Q =100KL.if the price of capital is 120 dollars per day and the price of labor 30 dollars per day what is the minimum cost of producing 1000 units of output ?arrow_forward

- خصائص TVAarrow_forwardplease show complete solution, step by step, thanksarrow_forwardTo determine the benefits of extending hours of operation for a food truck business, the couple should calculate additional revenue, break-even analysis, market demand, and raise prices. They should analyze competitors' prices and customer sensitivity to price changes, determine price elasticity, and test the strategy by implementing a slight price increase and monitoring sales closely. If costs exceed revenues, the couple should analyze their financials, evaluate their business model, explore new revenue streams, and consider long-term viability. They should analyze their financial statements to identify high costs and areas for reduction, evaluate their business model based on market demand, and explore new revenue streams like catering, special events, or partnerships with local businesses. Long-term viability is a key consideration, as if the business still operates at a loss after making adjustments, it may be necessary to consider shutting down. Staying in business should be…arrow_forward

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Microeconomics (MindTap Course List)EconomicsISBN:9781305971493Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Microeconomics (MindTap Course List)EconomicsISBN:9781305971493Author:N. Gregory MankiwPublisher:Cengage Learning