Judgment Case 16–9 Analyzing the effect of deferred tax liabilities on firm risk; Macy’s, Inc. • LO16–8 Real World Financials The following is a portion of the balance sheets of Macy’s, Inc . for the years ended January 30, 2016 and January 31, 2015: Macy’s debt to equity ratio for the year ended January 30, 2016, was 3.84, calculated as ($20,576 – 4,253) ÷ 4,253. Some analysts argue that long-term deferred tax liabilities should be excluded from liabilities when computing the debt to equity ratio. Required: 1. What is the rationale for the argument that long-term deferred tax liabilities should be excluded from liabilities when computing the debt to equity ratio? 2. What would be the effect on Macy’s debt to equity ratio of excluding deferred tax liabilities from its calculation? What would be the percentage change? 3. What might be the rationale for not excluding long-term deferred tax liabilities from liabilities when computing the debt to equity ratio?

Judgment Case 16–9 Analyzing the effect of deferred tax liabilities on firm risk; Macy’s, Inc. • LO16–8 Real World Financials The following is a portion of the balance sheets of Macy’s, Inc . for the years ended January 30, 2016 and January 31, 2015: Macy’s debt to equity ratio for the year ended January 30, 2016, was 3.84, calculated as ($20,576 – 4,253) ÷ 4,253. Some analysts argue that long-term deferred tax liabilities should be excluded from liabilities when computing the debt to equity ratio. Required: 1. What is the rationale for the argument that long-term deferred tax liabilities should be excluded from liabilities when computing the debt to equity ratio? 2. What would be the effect on Macy’s debt to equity ratio of excluding deferred tax liabilities from its calculation? What would be the percentage change? 3. What might be the rationale for not excluding long-term deferred tax liabilities from liabilities when computing the debt to equity ratio?

Solution Summary: The author explains the reason behind the exclusion of deferred tax liabilities from calculation of debt equity ratio.

Analyzing the effect of deferred tax liabilities on firm risk; Macy’s, Inc.

• LO16–8

Real World Financials

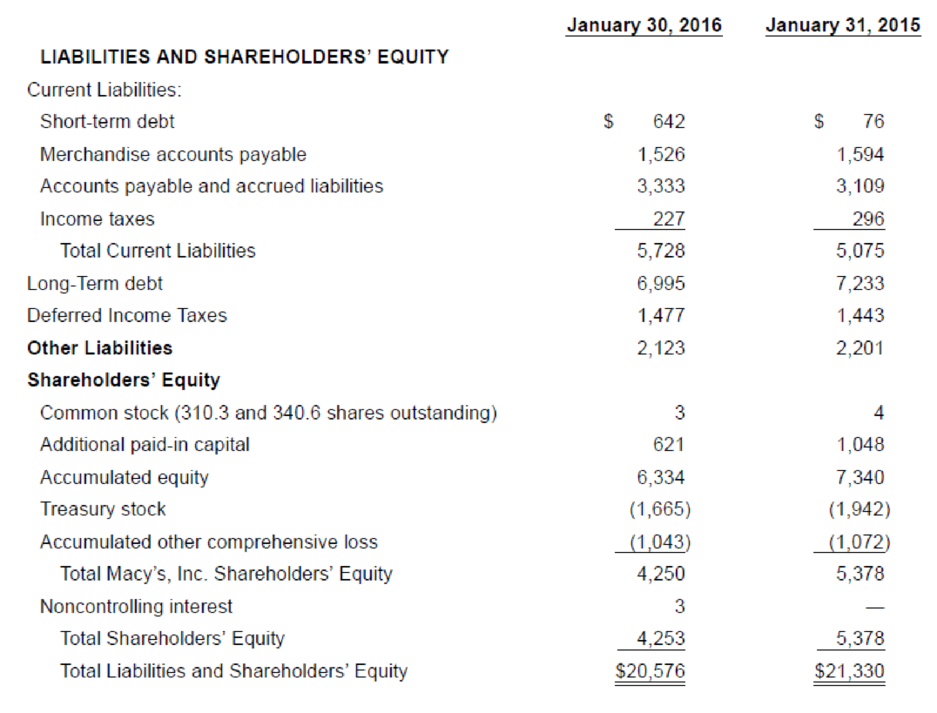

The following is a portion of the balance sheets of Macy’s, Inc. for the years ended January 30, 2016 and January 31, 2015:

Macy’s debt to equity ratio for the year ended January 30, 2016, was 3.84, calculated as ($20,576 – 4,253) ÷ 4,253. Some analysts argue that long-term deferred tax liabilities should be excluded from liabilities when computing the debt to equity ratio.

Required:

1. What is the rationale for the argument that long-term deferred tax liabilities should be excluded from liabilities when computing the debt to equity ratio?

2. What would be the effect on Macy’s debt to equity ratio of excluding deferred tax liabilities from its calculation? What would be the percentage change?

3. What might be the rationale for not excluding long-term deferred tax liabilities from liabilities when computing the debt to equity ratio?

Definition Definition Items on the balance sheet that are created when the tax paid is less than the tax considered on the income statement. A deferred tax liability is recorded on the liability side of the balance sheet and is thus a tax burden. It increases the taxes owed in the future.

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning