Calculate income tax amounts under various circumstances • LO16–1, LO16–2 Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences: The enacted tax rate is 40%. Required: For each situation, determine the: a. Income tax payable currently b. Deferred tax asset —balance c. Deferred tax asset—change (dr) cr d. Deferred tax liability —balance e. Deferred tax liability—change (dr) cr f. Income tax expense

Calculate income tax amounts under various circumstances • LO16–1, LO16–2 Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences: The enacted tax rate is 40%. Required: For each situation, determine the: a. Income tax payable currently b. Deferred tax asset —balance c. Deferred tax asset—change (dr) cr d. Deferred tax liability —balance e. Deferred tax liability—change (dr) cr f. Income tax expense

Solution Summary: The author explains how deferred tax is computed on the basis of tax liability on income as per income statement and the income per tax return.

Calculate income tax amounts under various circumstances

• LO16–1, LO16–2

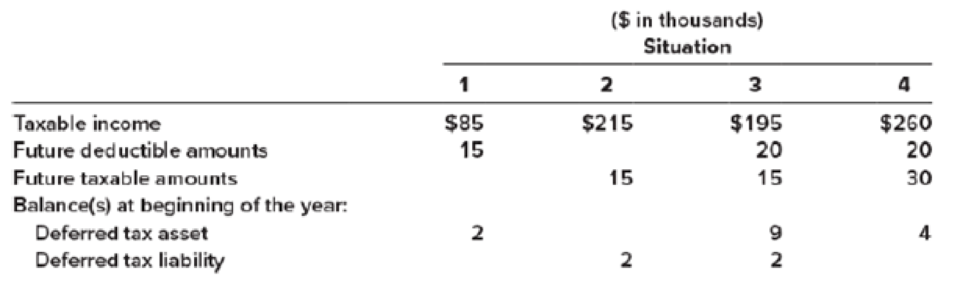

Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences:

The enacted tax rate is 40%.

Required:

For each situation, determine the:

a. Income tax payable currently

b. Deferred tax asset—balance

c. Deferred tax asset—change (dr) cr

d. Deferred tax liability—balance

e. Deferred tax liability—change (dr) cr

f. Income tax expense

Definition Definition Items on the balance sheet that are created when the tax paid is less than the tax considered on the income statement. A deferred tax liability is recorded on the liability side of the balance sheet and is thus a tax burden. It increases the taxes owed in the future.

Gitman: Principl Manageri Finance_15 (15th Edition) (What's New in Finance)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning