Videos

(Optimal Provision of Public Goods) Using at least two individual consumers, show how the market demand curve is derived from individual demand curves (a) for a private good and (b) for a public good. Once you have derived the market demand curve in each case, introduce a market supply curve and then show the optimal level of production.

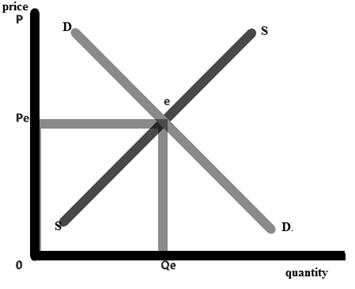

the market demand curve is to be derived from individual demand curves for a private goods and for a public good and then introduce the market supply curve and show the optimal level of production.

Concept Introduction:

A demand curve is a graph that shows the change in quantity demanded of a good or service with respect to its price. With change in price the demand also change and it carries an inverse relationship with the price. Market demand refers to the demand of a good in a particular market that adds up to a sum of different individual demands.

Explanation of Solution

Individual demand curves adds up to make a market demand curve for a good. It is a broader term that defines demand of a particular good at a much larger scale.

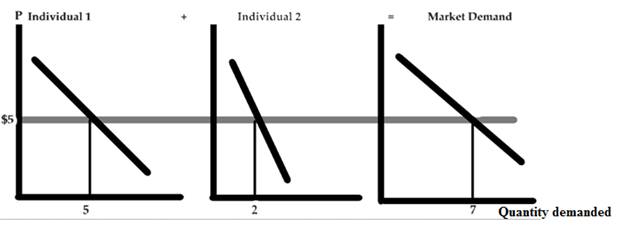

a. For a private good: Private good refers to the good that needs to be purchased from the private individual and its consumption by one individual prevents it to be consumed from the other individuals.

In the above figure there are three curves, where curve 1 is the individual demand curve for a good at price $5 and quantity 5 units. The second curve represents the individual demand curve for the same good at same price but the quantity is 2. The third curve is the market demand curve which is the summation of curve 1 of individual 1 and curve 2 of individual 2 at price $5 same as before. The market demand curve is the summation of curve 1 and curve 2 therefore the quantity for the same is 5 + 2 = 7 units.

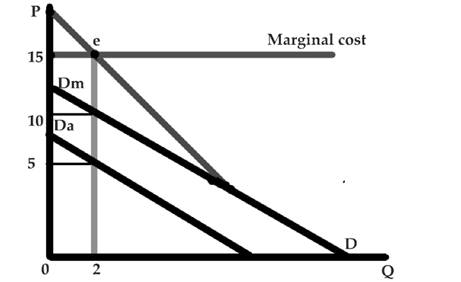

b. For public good: A public good is a good which is provided to all the members of the society without profit, it is provided by the government, individual or an organization. The consumption of such good doesn’t affect the consumption for others.

Public good once produced is available to all people and in identical amounts. Hence the demand for the public good is the vertical summation of each individuals demand. The marginal cost here equals the marginal benefits at e where the market demand curve and the marginal cost curve are at equilibrium. The red line on the graph represent the market demand curve and the blue line defines the marginal cost curve. Dm and Da are respectively the two individual demand curves which add up vertically with quantity being constant to make the market demand curve.

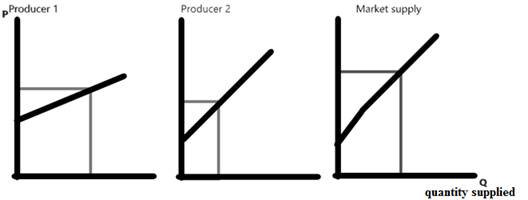

The market supply curve is an upward sloping curve which shows a positive relationship between the price and the quantity supplied. The summation of the individuals producers supply makes the market supply curve.

The optimal level of production is the point where the market demand is equal to that of the market supply and that level of intersection is called the market demand.

Want to see more full solutions like this?

Chapter 16 Solutions

ECON: MICRO4 (New, Engaging Titles from 4LTR Press)

- Explain why people fall prey to payday lenders, title pawn lenders, and “credit-approved” used car dealers.arrow_forwardPlease answer the following.arrow_forwardThe figure below shows the hypothetical domestic supply and demand for baseball caps in the country of Spain. Domestic Supply and Demand for Baseball Caps Price (€ per cap) 10 9 8 7 6 5 4 3 2 1 0 Spain Dd 10 20 30 40 50 60 70 80 90 100 Baseball caps (thousands per month) Suppose that the world price of baseball caps is €2 and there are no import restrictions on this product. Assume that Spanish consumers are indifferent between domestic and imported baseball caps. Instructions: Enter your answers as whole numbers. a. What quantity of baseball caps will domestic suppliers supply to domestic consumers? thousand b. What quantity of baseball caps will be imported? thousand Now suppose a tariff of €1 is levied against each imported baseball cap. c. After the tariff is implemented, what quantity of baseball caps will domestic suppliers supply to domestic consumers? thousand d. After the tariff is implemented, what quantity of baseball caps will be imported? thousandarrow_forward

- May I please have the solutions for the following assignment? as 2025arrow_forwardResponse to J.C. Ethics Statement Raising our products' global profile requires a firm commitment to doing the right thing by society and the environment. By switching to a more energy-efficient cloud architecture, BillRight Software, Inc. will reduce its carbon footprint while also ensuring the absolute security of all customer data. Fair labor standards, a diverse and inclusive workforce, and giving back to the communities where our employees live and work are some of our core values. Following local regulations, accepting cultural variances, and actively participating in community development projects are all ways our brand and product will uphold our ethical values globally (Corcoran, 2024; Kotler et al., 2023; Kotler & Keller, 2024; Solomon & Russell, 2024). How MKTG 525 Gets You Together with Classmates? Different points of view in dealing with classmates from many backgrounds exposes you to many points of view, ideas, and techniques. This variety enriches the learning…arrow_forward3. Case 2) Coal plants exit, and Solar generation enters the market Now, let's consider a scenario where the coal power plant (#1) shuts down and exits the market, and a solar generation facility is constructed. The capacity of the solar generation facility is the same as the coal power plant that went out of business. The generation capacities of this market are shown below, along with their MC. Table 3: Power Plant Capacity and Marginal Cost: Case 2 Plant # Energy Source Capacity (MW) MC (S/MWh) 2 Oil 100 90 3 Natural Gas 500 50 4 Nuclear 600 0 5 Solar 300 5 Note that the solar plant (#5) can generate electricity only from 7 AM until 5PM. During these hours, the plant can generate up to its full capacity (300 MW) but cannot generate any when unavailable. (a) Draw a supply curve for each hourly market (4AM, 10 AM, 2PM, 6PM). (b) Find the market clearing prices and calculate how much electricity each power plant generates in the hourly market (4AM, 10AM, 2PM, and 6PM). (c) Find the…arrow_forward

- Respond to L.R. To analyze consumer spending, you must review the macroeconomic indicators of Personal Consumption Expenditures (PCE) and Retail Sales over the past year. Selected Macroeconomic indicators Personal Consumption Expenditures (PCE) measure the value of household goods and services consumed and are a key indicator of consumer spending. - Retail Sales: This tracks the total receipts of retail stores and provides insight into consumer demand and spending trends. - Patterns over the past year: Personal Consumption Expenditures (PCE) Over the past year, PCE has steadily increased, reflecting consumer confidence and willingness to spend. The growth rate has been moderate, driven by wage growth, low unemployment rates, and government stimulus measures. However, inflationary pressures have also impacted real purchasing power, leading to a mixed outlook. - Retail sales have also experienced fluctuations but have generally trended upwards. After a…arrow_forward4. Case 3) Electricity demand increases due to increased EV adoption We will continue using the Case 2 supply curve (with the solar plant in operation) for this analysis. Suppose that electricity consumption from electric vehicles (EV) increases significantly. Consequently, electricity demand in the wholesale market increases at every hour. The new demand levels are shown in Table 5 below. The market operator has backup power plants (using natural gas) ready, with a total capacity of 300 MW and a MC of $100/MWh. Table 5: Hourly Demand (selected hours) Hour Demand (MWh) 4 AM 800 10 AM 1000 ... 2 PM 1100 ... 6 PM 1300 (a) Find the market clearing prices and calculate how much electricity each power plant generates in the hourly market (4AM, 10AM, 2PM, and 6PM). Is there a specific hourly market in which the market operator will need to dispatch backup generation? (b) Compare the Case 2 scenario with the Case 3 scenario in terms of CO2 emissions and average electricity price. Based on…arrow_forward2. Case 1) NG price decreases Now, suppose that the price of natural gas decreased substantially, causing the marginal cost of the NG power plant to decrease to MC = $35/MWh. The demand is the same as in Case 0. (a) Draw a new supply curve that reflects the MC change of the NG power plant. (b) Find the market clearing prices and calculate how much electricity each power plant generates in the hourly market (4AM, 10AM, 2PM, and 6PM). (c) What happened to the coal power plant? (d) Do you think the market outcomes (like average price) and the total CO2 emissions have improved under this Case 1 scenario (use the emissions data provided in the lecture slides)?arrow_forward

- 1. Case 0) Baseline case Table 1: Power Plant Capacity and Marginal Cost: Case 0 Plant # Energy Source Capacity (MW) MC (S/MWh) 1 Coal 300 45 2 Oil 100 90 3 4 Natural Gas Nuclear 500 50 600 0 (a) Calculate the capacity mix of this market by energy source. (b) Draw a supply curve of this wholesale generation market. Table 2 below shows the demand levels for selected hours of a representative day. We will consider only these four hourly markets for our analysis. Note that the 6 PM demand is the highest demand level of the day. Table 2: Hourly Demand (selected hours) Hour Demand (MWh) 4 AM 500 10 AM 700 2 PM 800 6 PM 1000 (c) Find the market clearing prices and calculate how much electricity each power plant generates in the hourly market (4AM, 10AM, 2PM, and 6PM). (d) Find the average price of electricity (by taking a simple average of hourly prices; [P(4am) + P(10AM) + P(2PM) + P(6PM)]/4).arrow_forwardDon't used Ai solutionarrow_forwardHow human recource allocated in an economic?arrow_forward

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours...EconomicsISBN:9781337091985Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Microeconomics (MindTap Course List)EconomicsISBN:9781305971493Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Microeconomics (MindTap Course List)EconomicsISBN:9781305971493Author:N. Gregory MankiwPublisher:Cengage Learning