Videos

You have been assigned to analyze the risk characteristics of these stocks. Prepare a report that includes but is not limited to the following items.

- a. Compute

descriptive statistics for each stock and the S&P 500. Comment on your results. Which stocks are the most volatile? - b. Compute the value of beta for each stock. Which of these stocks would you expect to perform best in an up market? Which would you expect to hold their value best in a down market?

- c. Comment on how much of the return for the individual stocks is explained by the market.

a.

Find the descriptive statistics for each stock and the S&P 500.

Comment on result and find the most volatile stock.

Answer to Problem 1CP

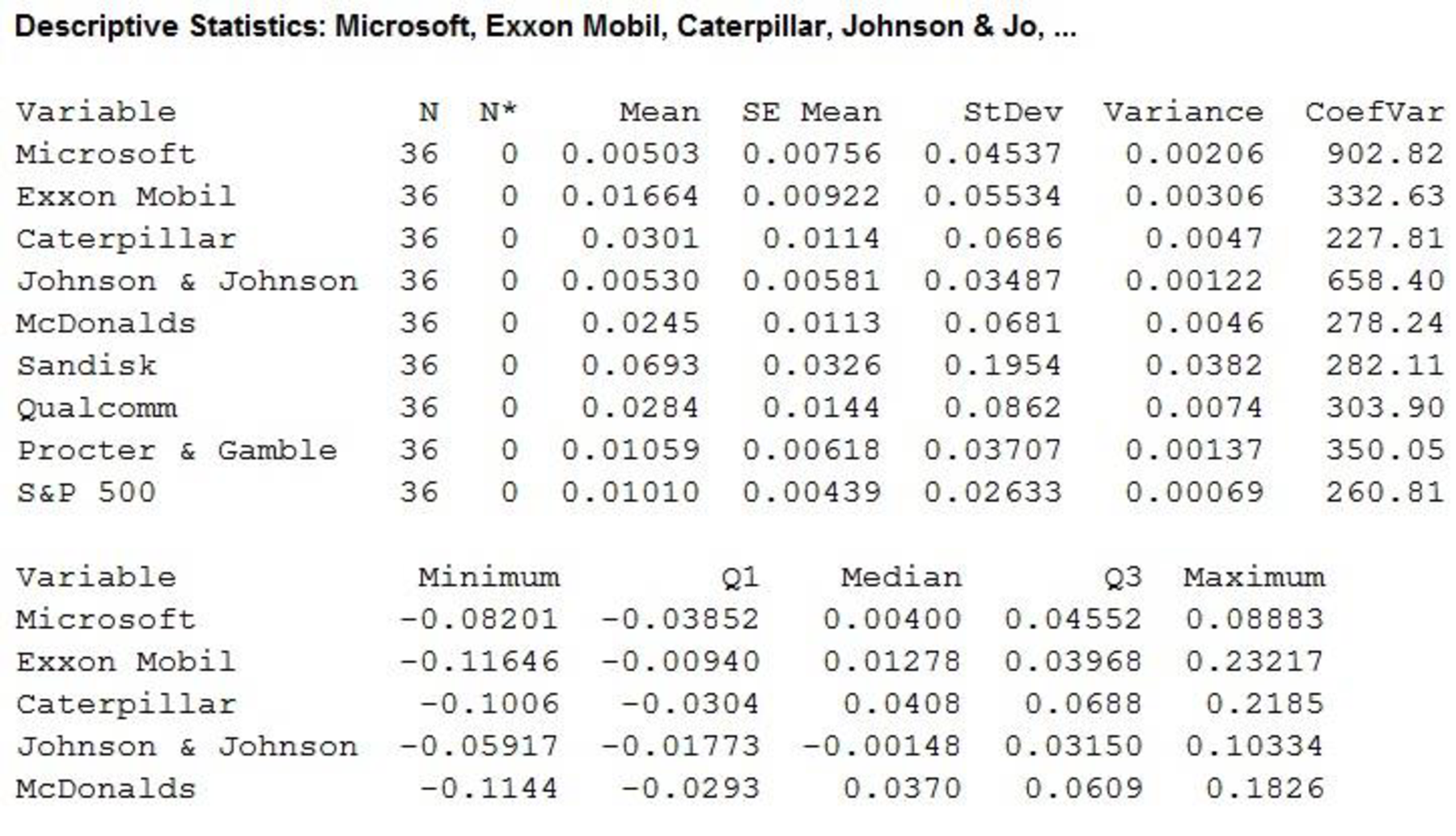

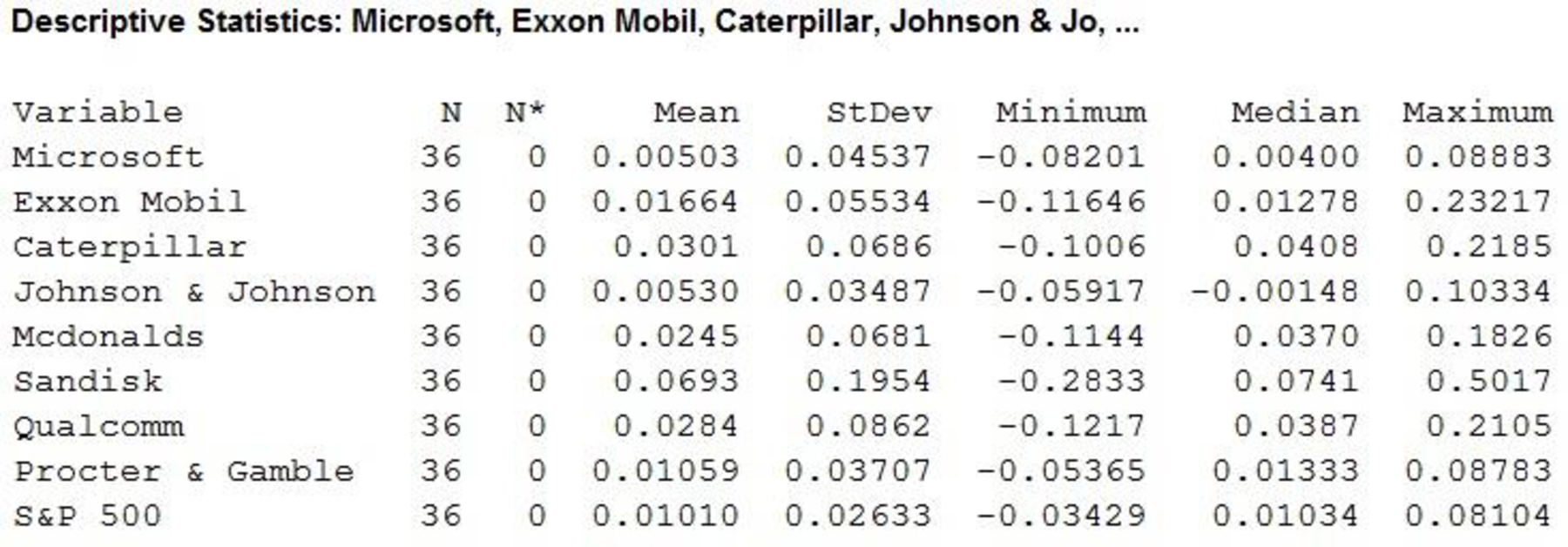

The descriptive statistics are obtained as given below:

The most volatile stock is for SanDisk Company.

Explanation of Solution

Calculation:

The data related to monthly return of stocks for eight companies with the market index S&P 500.

Descriptive Statistics:

Software procedure:

Step by step procedure to get descriptive statistics using MINITAB software is given below:

- Choose Stat > Basic Statistics > Display Descriptive Statistics.

- Under Variables, enter the columns ofMicrosoft, Exxon Mobil, Caterpillar, Johnson $ Johnson, McDonald’s, SanDisk, Qualcomm, Procter & Gamble and S&P 500.

- Click OK.

The output using MINITAB software is given as,

According to the output it is found that six companies, Exxon Mobil, Caterpillar, McDonald’s, SanDisk, Qualcomm and Procter & Gamblehad a higher mean monthly return than the S&P 500. Two companies Microsoft and Johnson & Johnson had the lower mean monthly returns.

Standard deviation can be treated as a measure of volatility for individual stock over several periods of time. The company SanDisk had the maximum standard deviation 0.1954. Thus, the volatility of SanDisk is high than other companies.

In addition, the stocks of Johnson & Johnson and Procter & Gamble had the standard deviation of 0.03487 and 0.03707, respectively. Thus, the volatility of Johnson & Johnson is lesser than other stocks.

However, the individual stocks are more volatile than the market as a whole.

b.

Find the values of beta for each stock.

Find the stocks that perform best in an up market.

Find the stocks that perform best in a down market.

Answer to Problem 1CP

The values of beta for each stock are given below:

| Company | Beta |

| Microsoft | 0.458 |

| Exxon Mobil | 0.731 |

| Caterpillar | 1.49 |

| Johnson & Johnson | 0.009 |

| McDonalds | 1.50 |

| SanDisk | 2.60 |

| Qualcomm | 1.41 |

| Procter & Gamble | 0.507 |

The stocks that perform best in an up market are Caterpillar, McDonalds, SanDisk and Qualcomm and the stocks that perform best in a down market are Microsoft, Exxon Mobil, Johnson & Johnson and Procter & Gamble.

Explanation of Solution

Calculation:

The value of beta for the stock market will always be 1.

If the betas are greater than 1 then that the stock is more volatile than the market and if betas are lesser than 1 indicated then the stock is less volatile than the market.

Regression:

Software procedure:

Step by step procedure to get regression equation using MINITAB software is given as,

- Choose Stat > Regression > Regression > Fit Regression Model.

- Under Responses, enter the column of Microsoft.

- Under Continuous predictors, enter the columns ofS&P 500.

- Click OK.

The output using MINITAB software is given as,

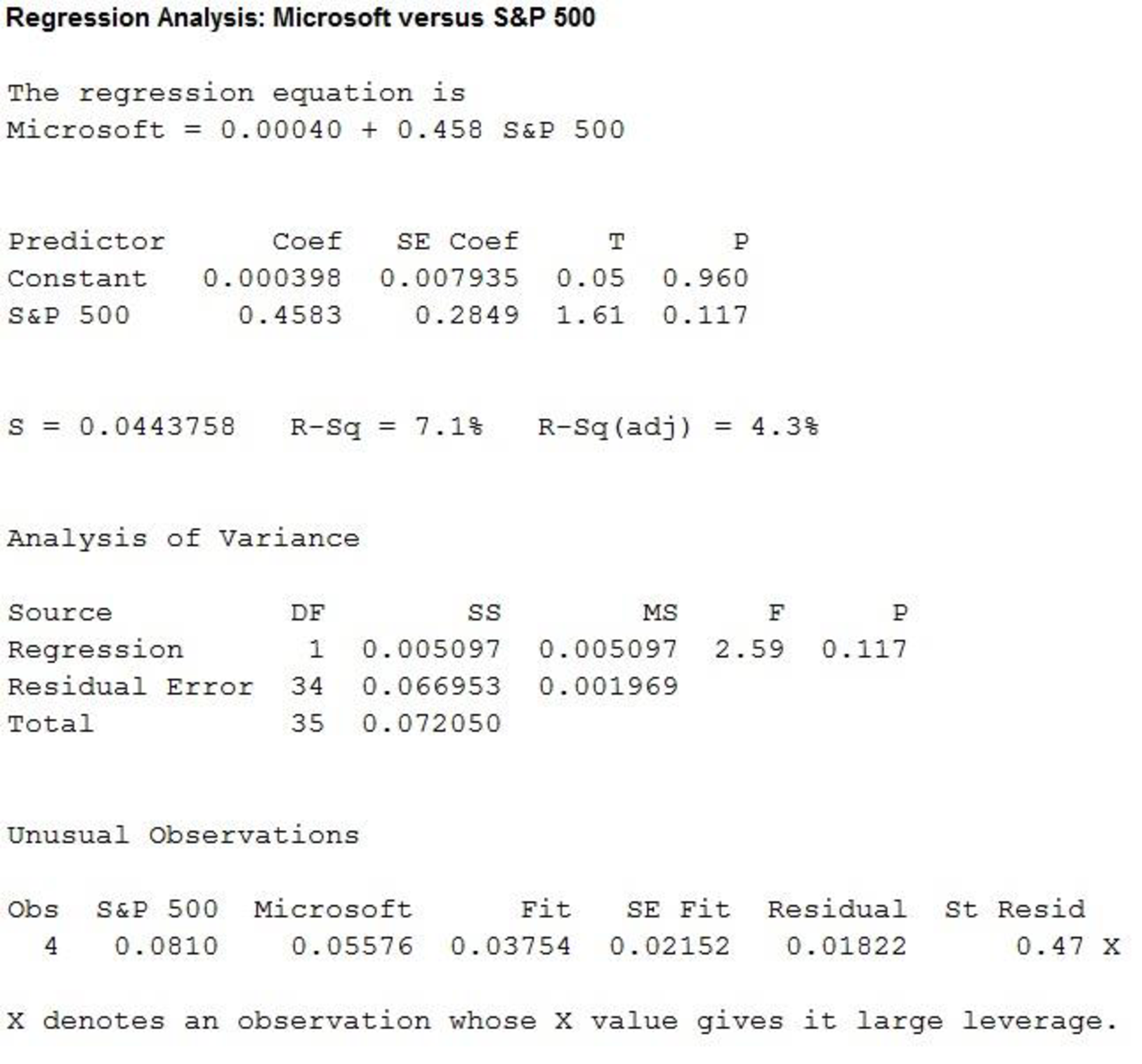

Thus, the estimated regression equation is

The slope of the regression equation is 0.458.

Regression:

Software procedure:

Step by step procedure to get regression equation using MINITAB software is given as,

- Choose Stat > Regression > Regression > Fit Regression Model.

- Under Responses, enter the column of Exxon Mobil.

- Under Continuous predictors, enter the columns ofS&P 500.

- Click OK.

The output using MINITAB software is given as,

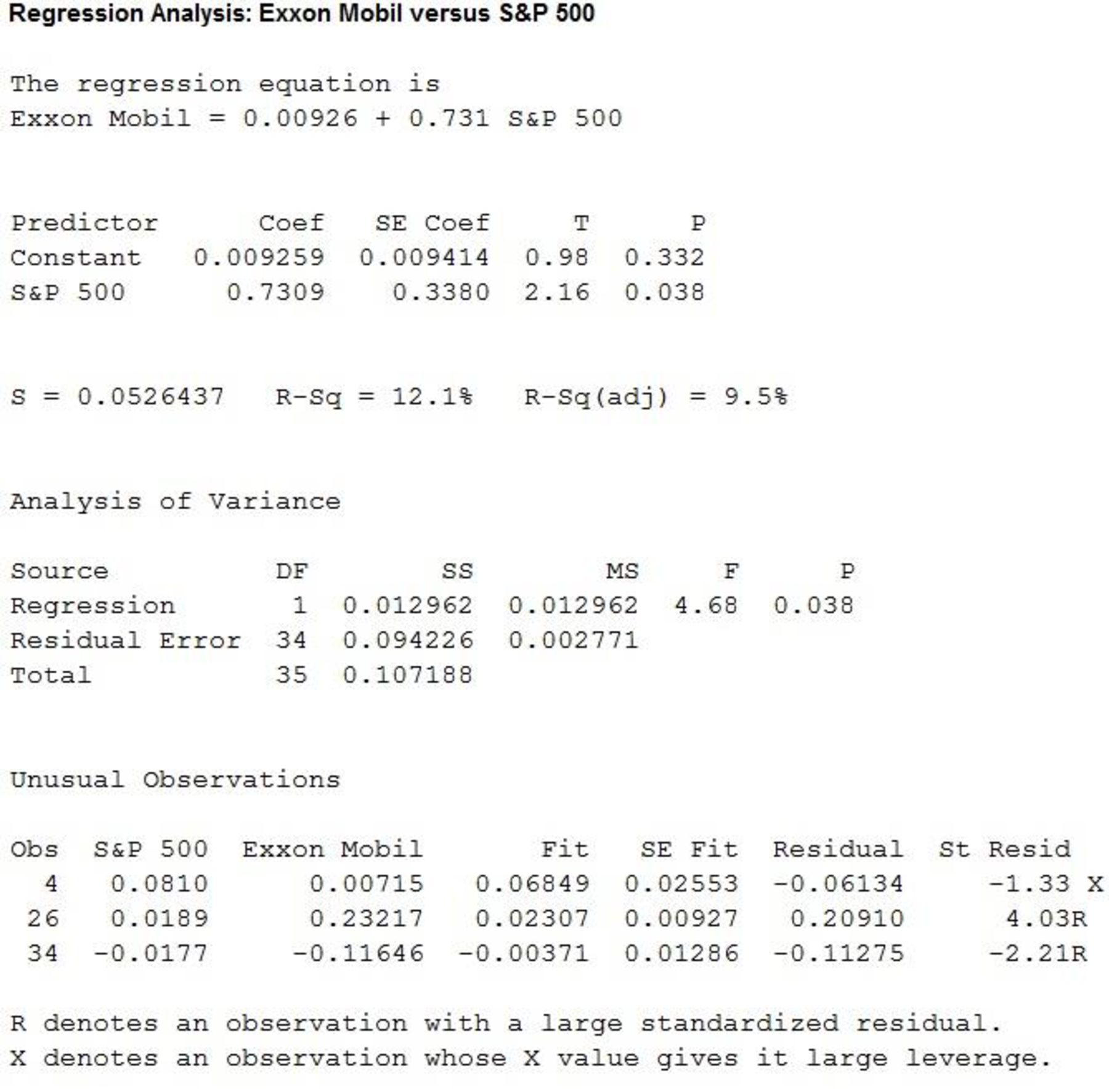

Thus, the estimated regression equation is

The slope of the regression equation is 0.731.

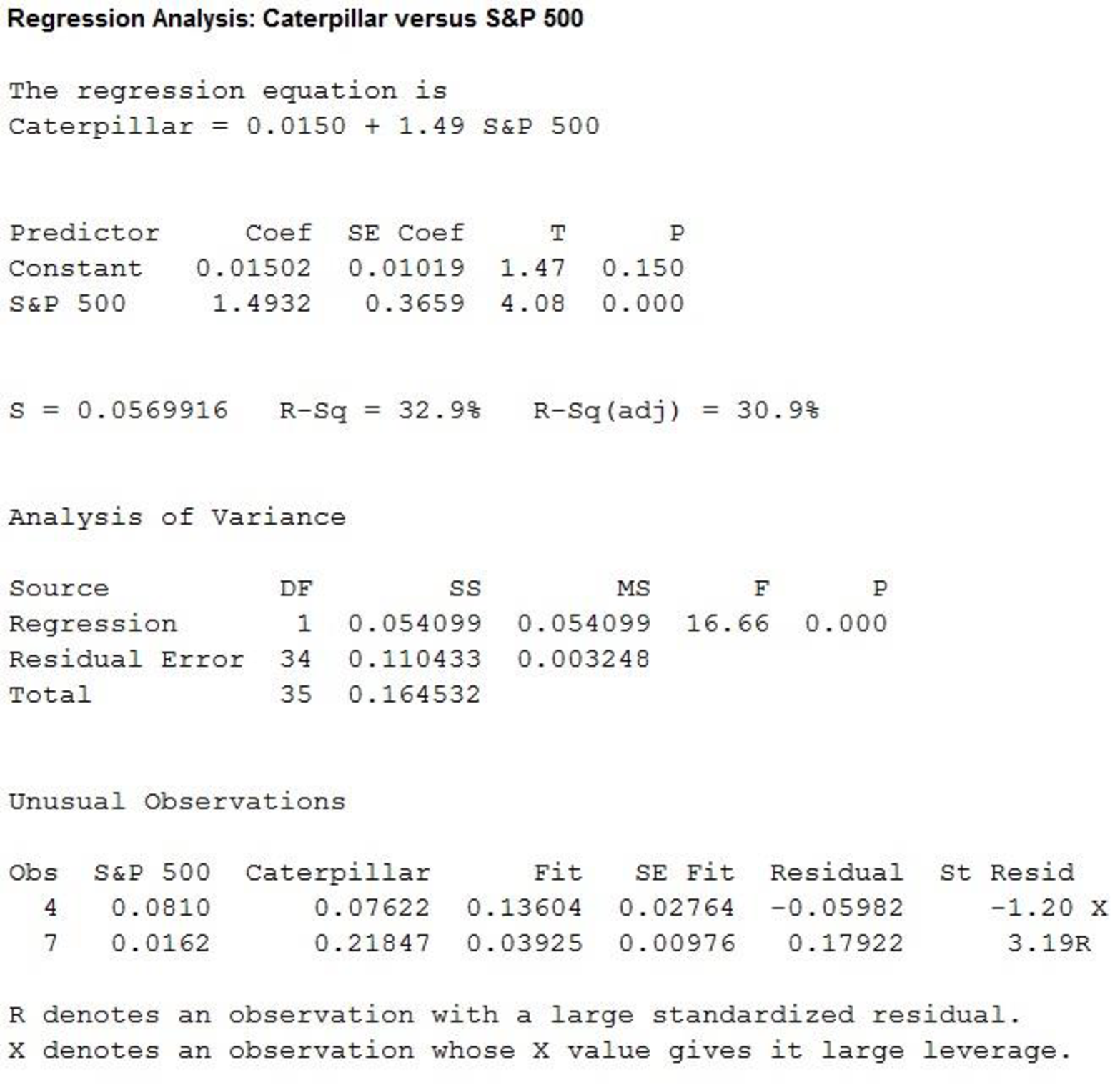

Regression:

Software procedure:

Step by step procedure to get regression equation using MINITAB software is given below:

- Choose Stat > Regression > Regression > Fit Regression Model.

- Under Responses, enter the column of Caterpillar.

- Under Continuous predictors, enter the columns of S&P 500.

- Click OK.

The output using MINITAB software is given as,

Thus, the estimated regression equation is

The slope of the regression equation is 1.49.

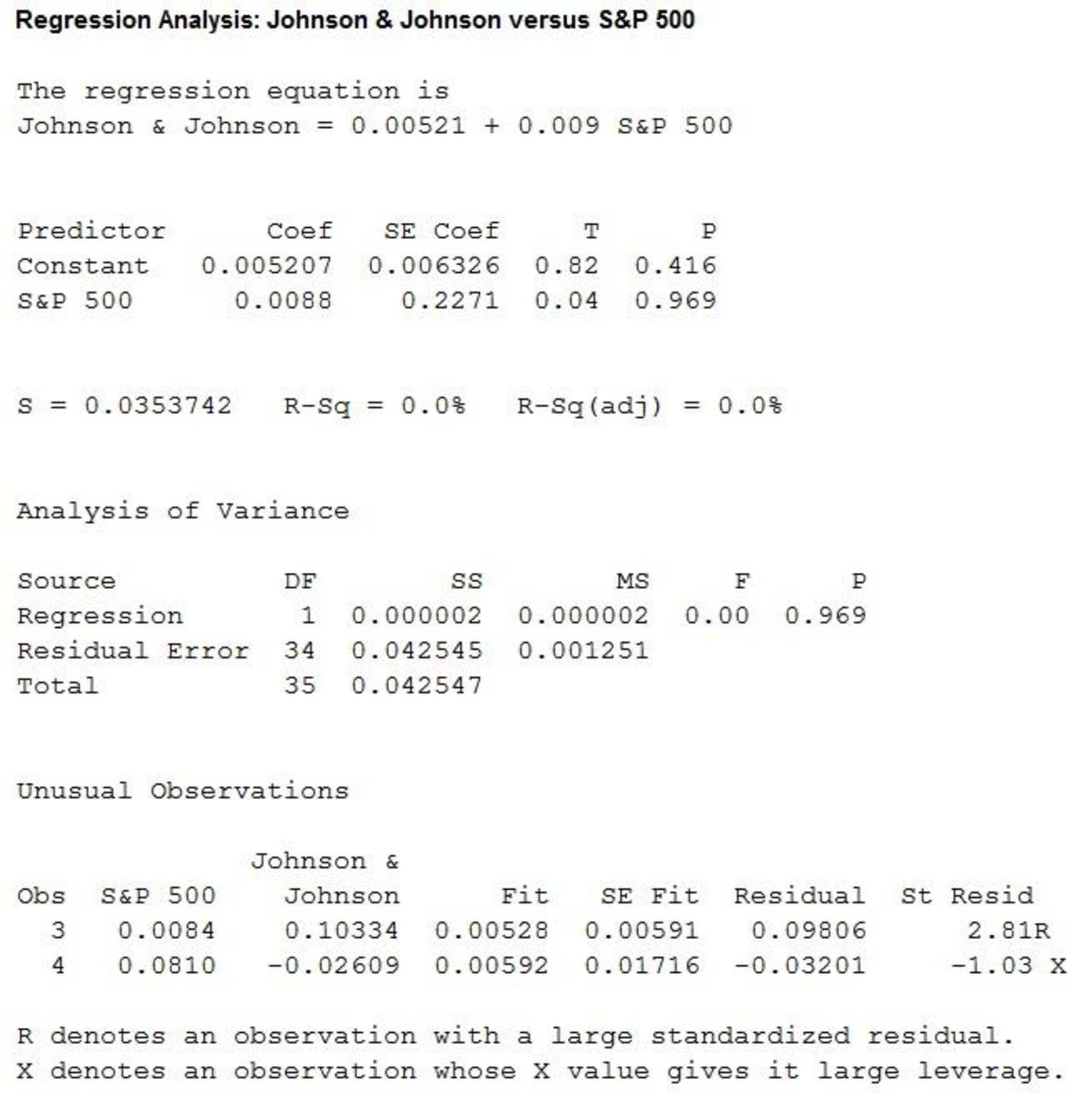

Regression:

Software procedure:

Step by step procedure to get regression equation using MINITAB software is given as,

- Choose Stat > Regression > Regression > Fit Regression Model.

- Under Responses, enter the column of Johnson & Johnson.

- Under Continuous predictors, enter the columns of S&P 500.

- Click OK.

The output using MINITAB software is given as,

Thus, the estimated regression equation is

The slope of the regression equation is 0.009.

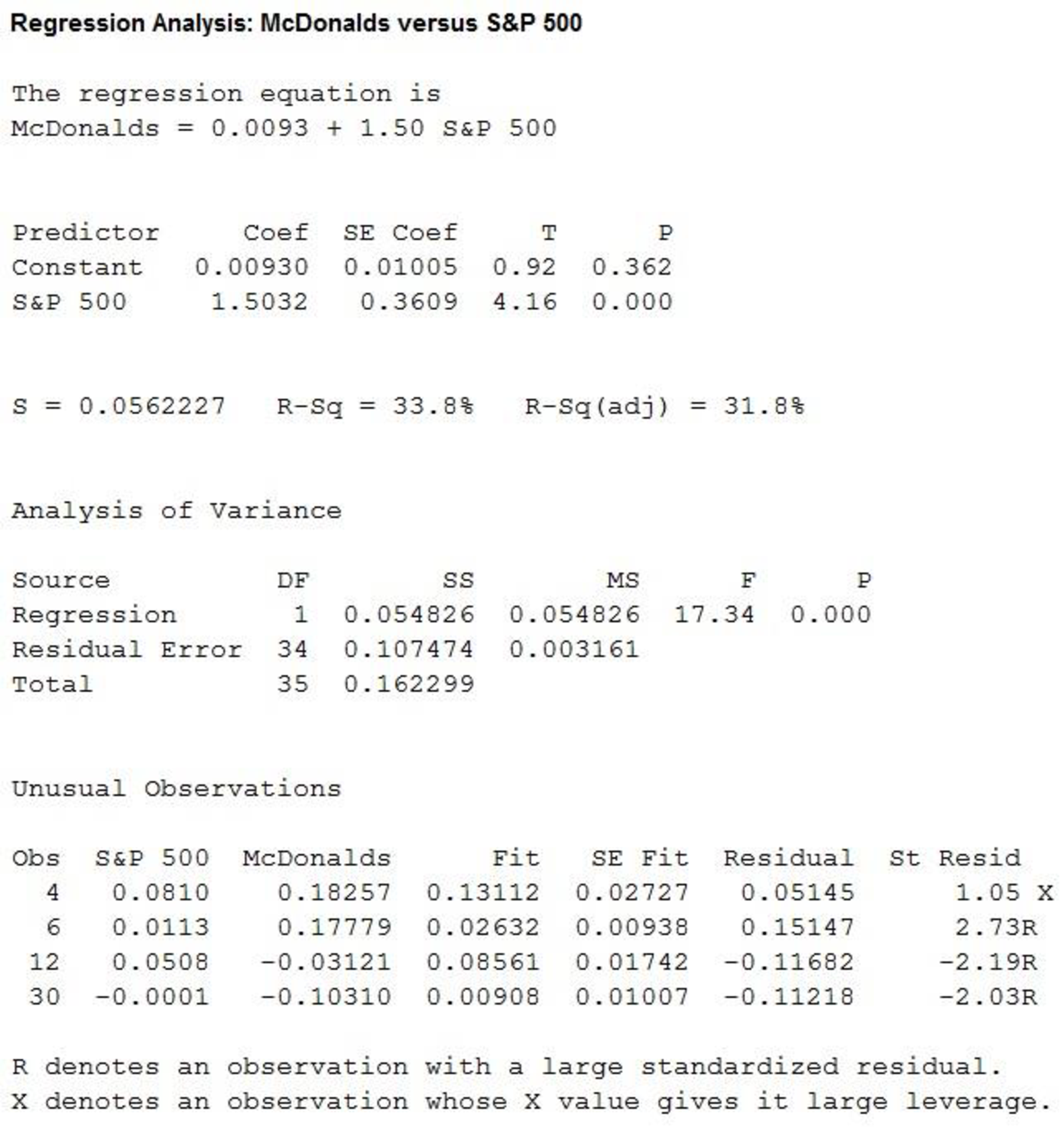

Regression:

Software procedure:

Step by step procedure to get regression equation using MINITAB software is given as,

- Choose Stat > Regression > Regression > Fit Regression Model.

- Under Responses, enter the column of McDonalds.

- Under Continuous predictors, enter the columns ofS&P 500.

- Click OK.

The output using MINITAB software is given as,

Thus, the estimated regression equation is

The slope of the regression equation is 1.50.

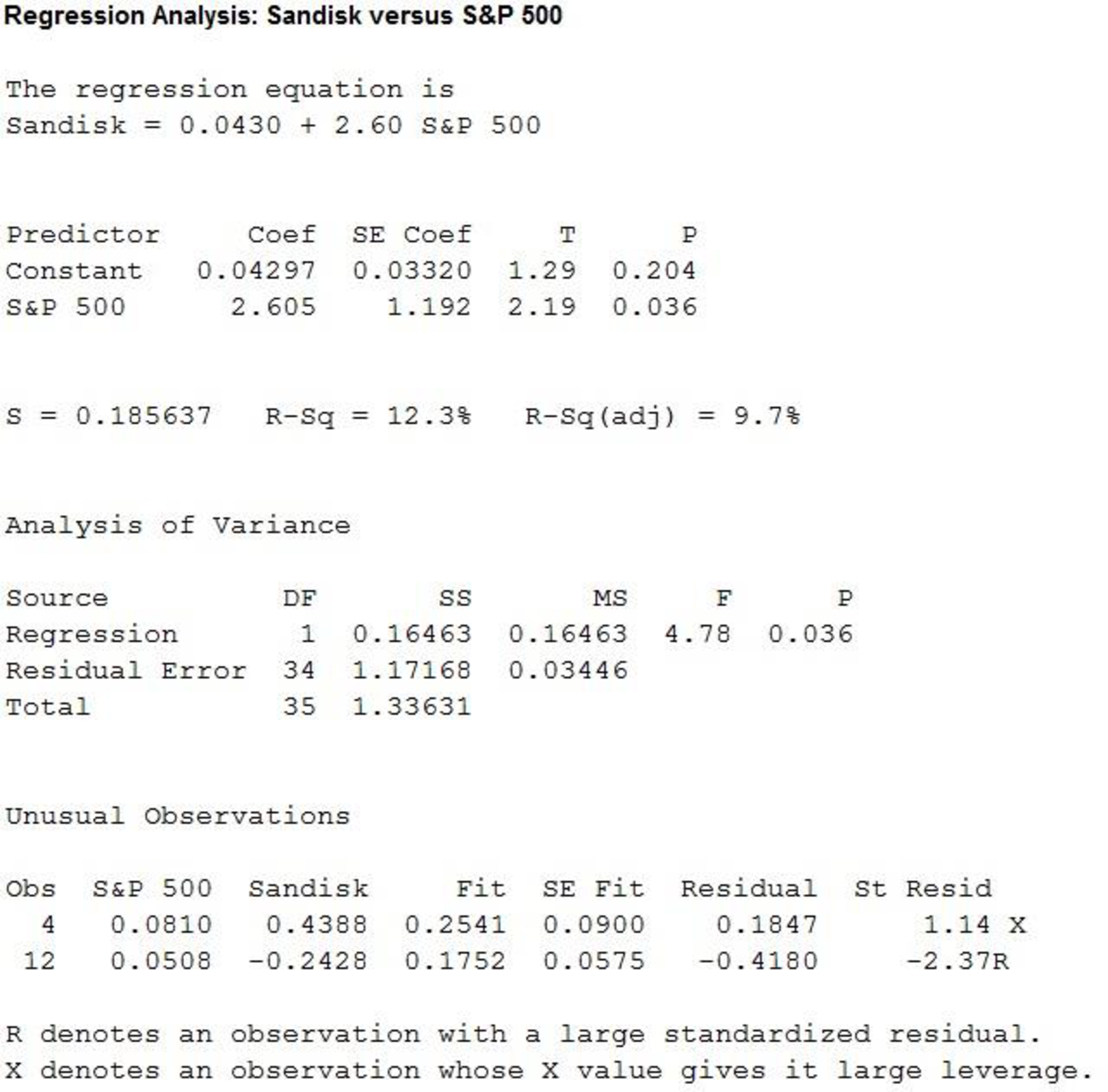

Regression:

Software procedure:

Step by step procedure to get regression equation using MINITAB software is given as,

- Choose Stat > Regression > Regression > Fit Regression Model.

- Under Responses, enter the column of SanDisk.

- Under Continuous predictors, enter the columns ofS&P 500.

- Click OK.

The output using MINITAB software is given as,

Thus, the estimated regression equation is

The slope of the regression equation is 2.60.

Regression:

Software procedure:

Step by step procedure to get regression equation using MINITAB software is given as,

- Choose Stat > Regression > Regression > Fit Regression Model.

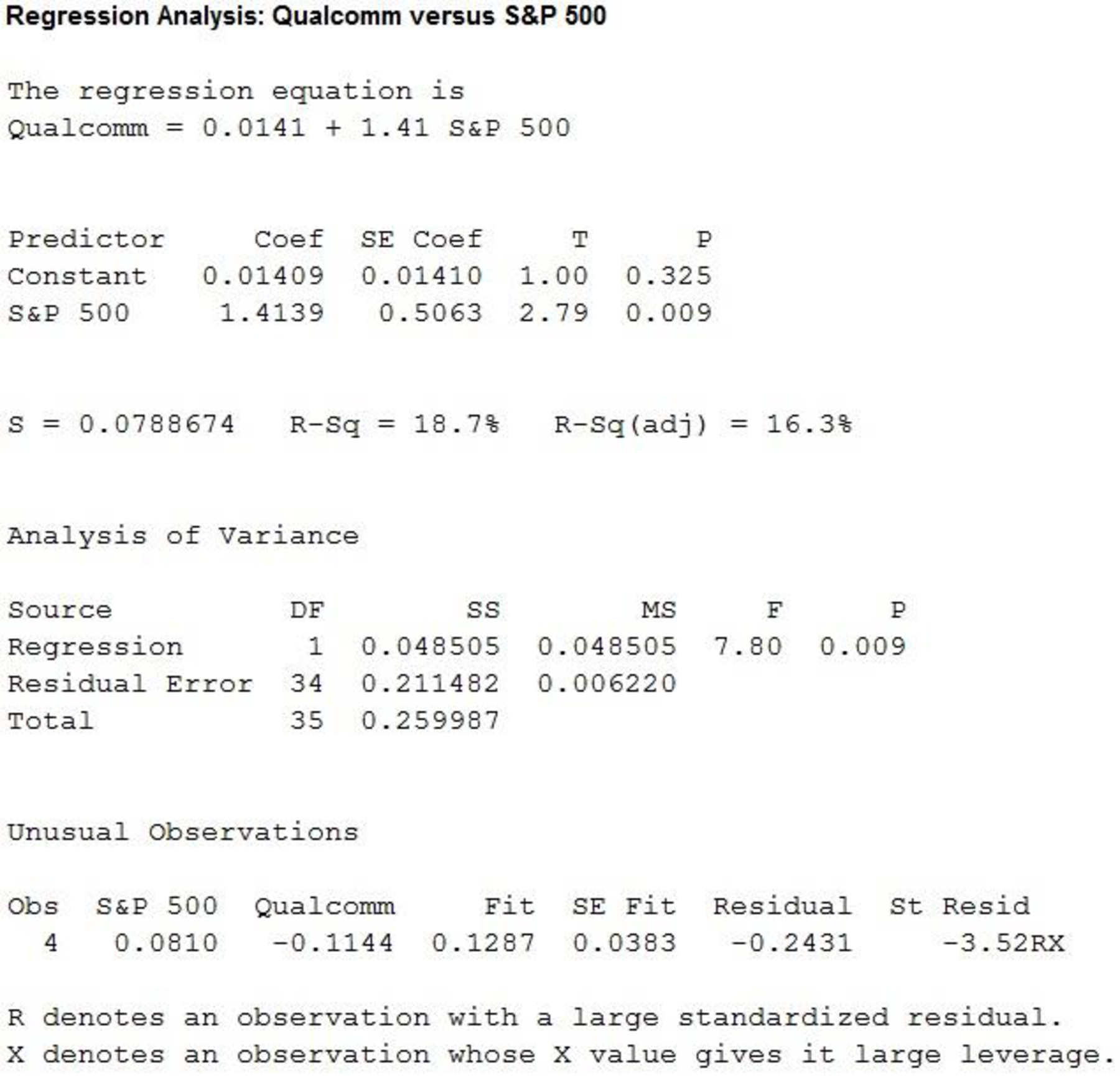

- Under Responses, enter the column of Qualcomm.

- Under Continuous predictors, enter the columns ofS&P 500.

- Click OK.

The output using MINITAB software is given as,

Thus, the estimated regression equation is

The slope of the regression equation is 1.41.

Regression:

Software procedure:

Step by step procedure to get regression equation using MINITAB software is given as,

- Choose Stat > Regression > Regression > Fit Regression Model.

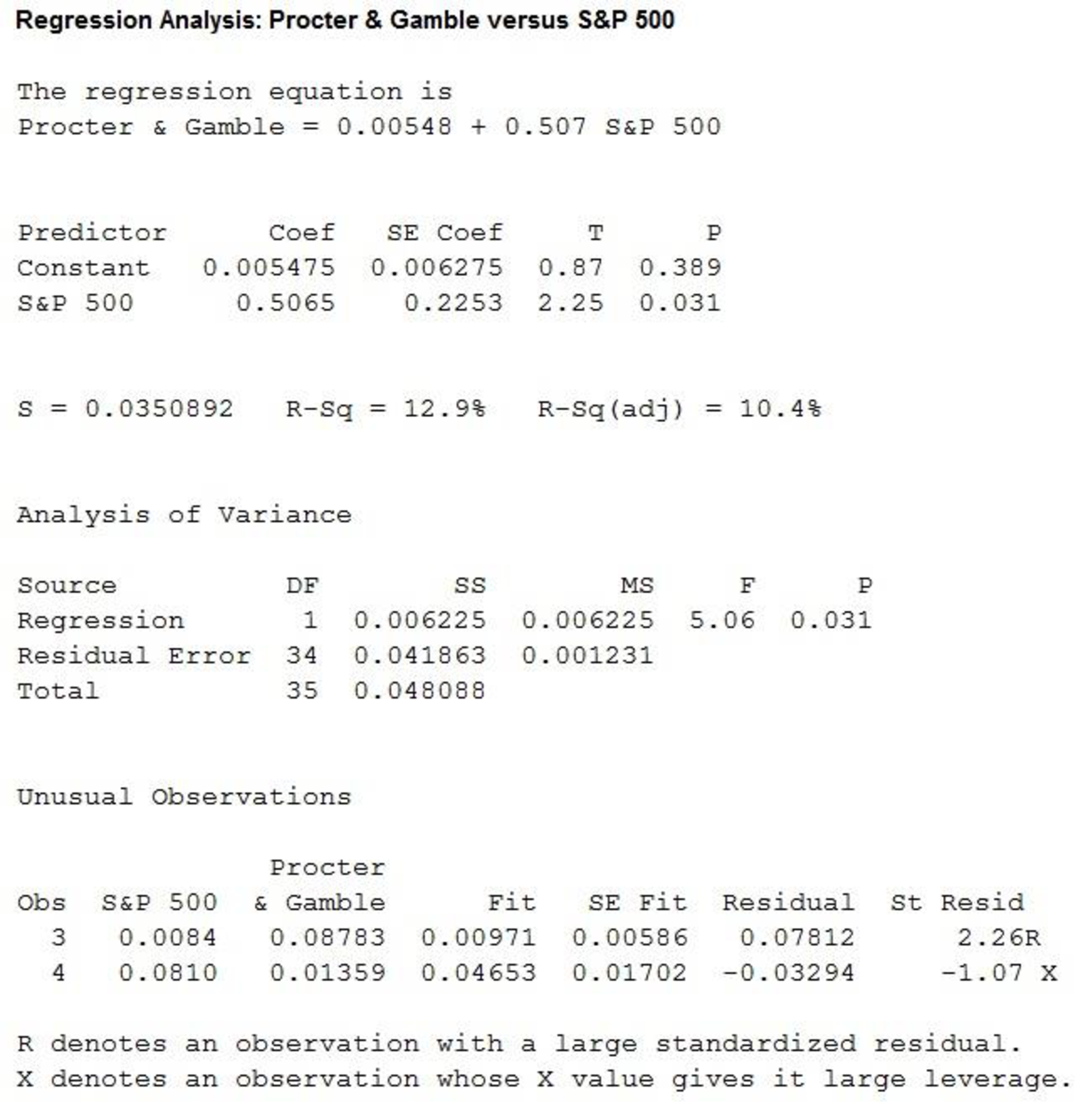

- Under Responses, enter the column of Procter & Gamble.

- Under Continuous predictors, enter the columns ofS&P 500.

- Click OK.

The output using MINITAB software is given as,

Hence, the estimated regression equation is

The slope of the regression equation is 0.507.

Thus, the values of beta for each stocks are,

| Company | Beta |

| Microsoft | 0.458 |

| Exxon Mobil | 0.731 |

| Caterpillar | 1.49 |

| Johnson & Johnson | 0.009 |

| McDonalds | 1.50 |

| SanDisk | 2.60 |

| Qualcomm | 1.41 |

| Procter & Gamble | 0.507 |

It is shown that the betas for Caterpillar, McDonalds, SanDisk and Qualcomm are greater than 1. Therefore these stocks are more volatile than the market.

Thus, the stocks that perform best in an up market are Caterpillar, McDonalds, SanDisk and Qualcomm.

It is shown that the betas for Microsoft, Exxon Mobil, Johnson & Johnson and Procter & Gamble are less than 1. Therefore these stocks are less volatile than the market.

Thus, the stocks that perform best in a down market are Microsoft, Exxon Mobil, Johnson & Johnson and Procter & Gamble.

c.

Comment on how much return for the individual stocks is explained by the market.

Explanation of Solution

Calculation:

The coefficient of determination (

Thus, the values of

| Company | |

| Microsoft | 7.1% |

| Exxon Mobil | 12.1% |

| Caterpillar | 32.9% |

| Johnson & Johnson | 0% |

| McDonalds | 33.8% |

| SanDisk | 12.3% |

| Qualcomm | 18.7% |

| Procter & Gamble | 12.9% |

Thus, the 7.1% variability in monthly return is explained by the variability of stock for Microsoft using the regression equation.

Thus, the 12.1% variability in monthly return is explained by the variability of stock for Exxon Mobil using the regression equation.

Thus, the 32.9% variability in monthly return is explained by the variability of stock for Caterpillar using the regression equation.

Thus, the 0.0% variability in monthly return is explained by the variability of stock for Johnson & Johnson using the regression equation.

Thus, the 33.8% variability in monthly return is explained by the variability of stock for McDonalds using the regression equation.

Thus, the 12.3% variability in monthly return is explained by the variability of stock for SanDisk using the regression equation.

Thus, the 18.7% variability in monthly return is explained by the variability of stock for Qualcomm using the regression equation.

Thus, the 12.9% variability in monthly return is explained by the variability of stock for Procter & Gamble using the regression equation.

Want to see more full solutions like this?

Chapter 14 Solutions

EBK STATISTICS FOR BUSINESS & ECONOMICS

- Activ Determine compass error using amplitude (Sun). Minimum number of times that activity should be performed: 3 (1 each phase) Sample calculation (Amplitude- Sun): On 07th May 2006 at Sunset, a vessel in position 10°00'N 010°00'W observed the Sun bearing 288° by compass. Find the compass error. LMT Sunset: LIT: (+) 00d 07d 18h 00h 13m 40m UTC Sunset: 07d 18h 53m (added- since longitude is westerly) Declination (07d 18h): N 016° 55.5' d (0.7): (+) 00.6' Declination Sun: N 016° 56.1' Sin Amplitude = Sin Declination/Cos Latitude = Sin 016°56.1'/ Cos 10°00' = 0.295780189 Amplitude=W17.2N (The prefix of amplitude is named easterly if body is rising, and westerly if body is setting. The suffix is named same as declination) True Bearing=287.2° Compass Bearing= 288.0° Compass Error = 0.8° Westarrow_forwardOnly sure experts solve it correct complete solutions okkarrow_forward13. In 2000, two organizations conducted surveys to ascertain the public's opinion on banning gay men from serving in leadership roles in the Boy Scouts.• A Pew poll asked respondents whether they agreed with "the recent decision by the Supreme Court" that "the Boy Scouts of America have a constitutional right to block gay men from becoming troop leaders."A Los Angeles Times poll asked respondents whether they agreed with the following statement: "A Boy Scout leader should be removed from his duties as a troop leader if he is found out to be gay, even if he is considered by the Scout organization to be a model Boy Scout leader."One of these polls found 36% agreement; the other found 56% agreement. Which of the following statements is true?A) The Pew poll found 36% agreement, and the Los Angeles Times poll found 56% agreement.B) The Pew poll includes a leading question, while the Los Angeles Times poll uses neutral wording.C) The Los Angeles Times Poll includes a leading question, while…arrow_forward

- Introduce yourself and describe a time when you used data in a personal or professional decision. This could be anything from analyzing sales data on the job to making an informed purchasing decision about a home or car. Describe to Susan how to take a sample of the student population that would not represent the population well. Describe to Susan how to take a sample of the student population that would represent the population well. Finally, describe the relationship of a sample to a population and classify your two samples as random, systematic, cluster, stratified, or convenience.arrow_forward1.2.17. (!) Let G,, be the graph whose vertices are the permutations of (1,..., n}, with two permutations a₁, ..., a,, and b₁, ..., b, adjacent if they differ by interchanging a pair of adjacent entries (G3 shown below). Prove that G,, is connected. 132 123 213 312 321 231arrow_forwardYou are planning an experiment to determine the effect of the brand of gasoline and the weight of a car on gas mileage measured in miles per gallon. You will use a single test car, adding weights so that its total weight is 3000, 3500, or 4000 pounds. The car will drive on a test track at each weight using each of Amoco, Marathon, and Speedway gasoline. Which is the best way to organize the study? Start with 3000 pounds and Amoco and run the car on the test track. Then do 3500 and 4000 pounds. Change to Marathon and go through the three weights in order. Then change to Speedway and do the three weights in order once more. Start with 3000 pounds and Amoco and run the car on the test track. Then change to Marathon and then to Speedway without changing the weight. Then add weights to get 3500 pounds and go through the three gasolines in the same order.Then change to 4000 pounds and do the three gasolines in order again. Choose a gasoline at random, and run the car with this gasoline at…arrow_forward

- AP1.2 A child is 40 inches tall, which places her at the 90th percentile of all children of similar age. The heights for children of this age form an approximately Normal distribution with a mean of 38 inches. Based on this information, what is the standard deviation of the heights of all children of this age? 0.20 inches (c) 0.65 inches (e) 1.56 inches 0.31 inches (d) 1.21 inchesarrow_forwardAP1.1 You look at real estate ads for houses in Sarasota, Florida. Many houses range from $200,000 to $400,000 in price. The few houses on the water, however, have prices up to $15 million. Which of the following statements best describes the distribution of home prices in Sarasota? The distribution is most likely skewed to the left, and the mean is greater than the median. The distribution is most likely skewed to the left, and the mean is less than the median. The distribution is roughly symmetric with a few high outliers, and the mean is approximately equal to the median. The distribution is most likely skewed to the right, and the mean is greater than the median. The distribution is most likely skewed to the right, and the mean is less than the median.arrow_forwardDuring busy political seasons, many opinion polls are conducted. In apresidential race, how do you think the participants in polls are generally selected?Discuss any issues regarding simple random, stratified, systematic, cluster, andconvenience sampling in these polls. What about other types of polls, besides political?arrow_forward

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill Big Ideas Math A Bridge To Success Algebra 1: Stu...AlgebraISBN:9781680331141Author:HOUGHTON MIFFLIN HARCOURTPublisher:Houghton Mifflin Harcourt

Big Ideas Math A Bridge To Success Algebra 1: Stu...AlgebraISBN:9781680331141Author:HOUGHTON MIFFLIN HARCOURTPublisher:Houghton Mifflin Harcourt Functions and Change: A Modeling Approach to Coll...AlgebraISBN:9781337111348Author:Bruce Crauder, Benny Evans, Alan NoellPublisher:Cengage Learning

Functions and Change: A Modeling Approach to Coll...AlgebraISBN:9781337111348Author:Bruce Crauder, Benny Evans, Alan NoellPublisher:Cengage Learning