Subpart (a):

Calculate the marginal cost, average total cost , variable cost and total cost.

Subpart (a):

Explanation of Solution

Table -1 shows the value of the

Table -1

| Quantity | Average variable cost |

| 1 | 1 |

| 2 | 2 |

| 3 | 3 |

| 4 | 4 |

| 5 | 5 |

| 6 | 6 |

The variable cost can be calculated by using the following formula:

Substitute the respective values in Equation (1) to calculate the variable cost.

Thus, the variable cost is $1.

Table -2 shows the value of the variable cost obtained by using Equation (1).

Table -2

| Quantity | Average variable cost | Variable cost |

| 1 | 1 | 1 |

| 2 | 2 | 4 |

| 3 | 3 | 9 |

| 4 | 4 | 16 |

| 5 | 5 | 25 |

| 6 | 6 | 36 |

The total cost can be calculated by using the following formula:

Substitute the respective values in Equation (2) to calculate the total cost.

Thus, the total cost is $17.

Table -3 shows the value of the total cost obtained by using Equation (2).

Table – 3

| Quantity | Average variable cost | Variable cost | Total cost |

| 1 | 1 | 1 | 17 |

| 2 | 2 | 4 | 20 |

| 3 | 3 | 9 | 25 |

| 4 | 4 | 16 | 32 |

| 5 | 5 | 25 | 41 |

| 6 | 6 | 36 | 52 |

The marginal cost can be calculated by using the following formula:

Substitute the respective values in Equation (3) to calculate the marginal cost.

Thus, the marginal cost is $3.

Table -4 shows the value of the marginal cost obtained by using Equation (3).

Table -4

| Quantity | Average variable cost | Variable cost | Total cost | Marginal cost |

| 1 | 1 | 1 | 17 | – |

| 2 | 2 | 4 | 20 | 3 |

| 3 | 3 | 9 | 25 | 5 |

| 4 | 4 | 16 | 32 | 7 |

| 5 | 5 | 25 | 41 | 9 |

| 6 | 6 | 36 | 52 | 11 |

The average total cost can be calculated by using the following formula:

Substitute the respective values in Equation (4) to calculate the average total cost.

Thus, the average total cost is $17.

Table -5 shows the value of the average total cost obtained by using Equation (4).

Table -5

| Quantity | Average variable cost | Variable cost | Total cost | Marginal cost | Average total cost |

| 1 | 1 | 1 | 17 | – | 17 |

| 2 | 2 | 4 | 20 | 3 | 10 |

| 3 | 3 | 9 | 25 | 5 | 8.33 |

| 4 | 4 | 16 | 32 | 7 | 8 |

| 5 | 5 | 25 | 41 | 9 | 8.20 |

| 6 | 6 | 36 | 52 | 11 | 8.67 |

Concept introduction:

Marginal cost: Marginal cost refers to the additional cost incurred from producing one more additional unit of output.

Average total cost: The average total cost is the total cost per unit of the output produced by a firm.

Average variable cost: Average variable cost refers to the variable cost per unit.

Average total cost: Average total cost refers to the total cost per unit.

Subpart (b):

Total supply in the market.

Subpart (b):

Explanation of Solution

Suppose the

Concept introduction:

Supply: Supply refers to the total value of the goods and services that are available for the purchase at a particular

Subpart (c):

Long run profit.

Subpart (c):

Explanation of Solution

In the long-run, a firm can enter or exit the market. In this transition, when a firm enters the market, price will still fall at the minimum average total cost. Since the market price is $10, which is higher than the minimum of the average total cost of $8. So, the new firm’s entry will result in a decrease in the price level. When the price decreases, the quantity demand will increase. Also, the quantity of the supply decreases because the newly entered firm will continue to produce only when the price equals the average total cost. So, beyond that equilibrium state the firm will produce zero

Concept introduction:

Long run: Thelong run refers to the time, which changes the production variable to adjust to the market situation.

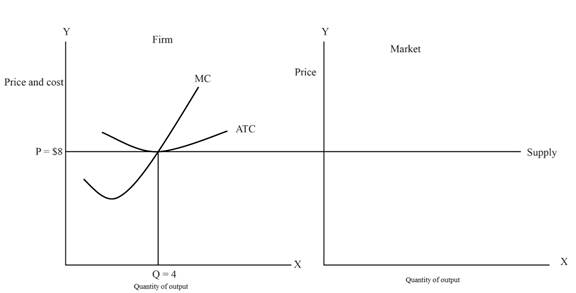

Subpart (d):

Long run supply.

Subpart (d):

Explanation of Solution

Figure – 1 shows the long-run supply curve for the market.

From the above figure, the x-axis represents the quantity of output and the y-axis represents the price and cost.

Concept introduction:

Supply: Supply refers to the total value of the goods and services that are available for the purchase at a particular price in a given period of time.

Want to see more full solutions like this?

Chapter 14 Solutions

ECNS 201 PRINTOUT

- Please give with explanationarrow_forwardnot use ai pleasearrow_forwardand u (C1, C2) = 1/2 = f) Derive analytically and show graphically the solution under other util- ity functions such as u (C1, C2) ac₁+bc2 where a, b > 0, u (C1, C2) = ac₁+bc1/2 acbc2 (assume that the agent is sufficiently rich to avoid the corner solution). What of these utility functions reflects best your own preferences (or indicate other utility function that represent your pref- erences).arrow_forward

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning

Essentials of Economics (MindTap Course List)EconomicsISBN:9781337091992Author:N. Gregory MankiwPublisher:Cengage Learning Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Exploring EconomicsEconomicsISBN:9781544336329Author:Robert L. SextonPublisher:SAGE Publications, Inc

Exploring EconomicsEconomicsISBN:9781544336329Author:Robert L. SextonPublisher:SAGE Publications, Inc