Concept explainers

Videos

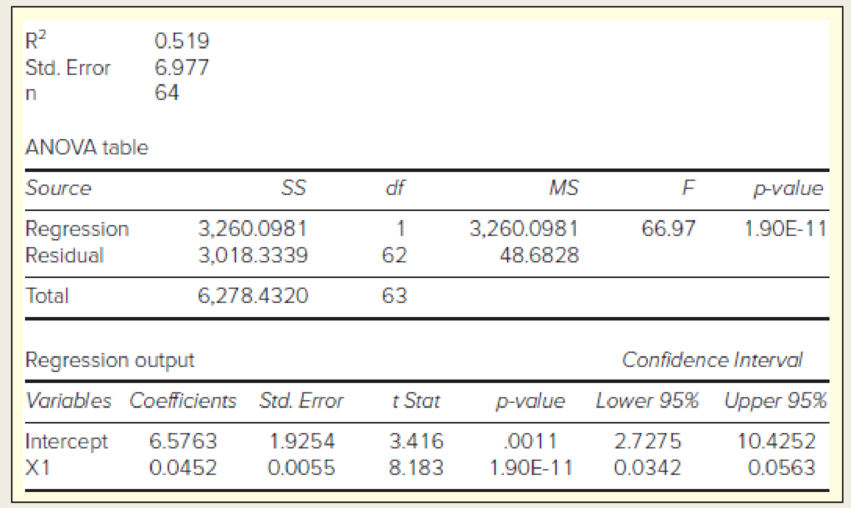

In the following regression, X = total assets ($ billions), Y = total revenue ($ billions), and n = 64 large banks. (a) Write the fitted regression equation. (b) State the degrees of freedom for a two-tailed test for zero slope, and use Appendix D to find the critical value at α = .05. (c) What is your conclusion about the slope? (d) Interpret the 95 percent confidence limits for the slope. (e) Verify that F= t2 for the slope. (f) In your own words, describe the fit of this regression.

a.

Write the fitted regression equation.

Answer to Problem 62CE

The regression equation is,

Explanation of Solution

Calculation:

An output of a regression is given. The X variable is the total assets and Y be the total revenue.

Regression:

Suppose

Where,

The total sum of squares is denoted as,

The regression sum of squares is denoted as,

The error sum of squares is denoted as,

From the regression the fitted line is denoted as,

From the output,

Hence, the regression equation is,

b.

Find the degrees of freedom for the two-tailed test for zero slope.

Find the critical value at 0.05 level of significanceusing Appendix D.

Answer to Problem 62CE

The degrees of freedom for the two-tailed test for zero slop is62.

The critical value at 0.05 level of significanceis 2.000.

Explanation of Solution

Calculation:

Critical value:

Here from the output, the sample size,

The degrees of freedom is,

For two tailed test, the critical value for t-test will be,

From the Appendix D: STUDENT’S t CRITICAL VALUES:

- • Since 62 is not in the table, so locate the value 60in the column of degrees of freedom.

- • Locate the 0.025 in level of significance.

- • The intersecting value that corresponds to the degrees of freedom 60 with level of significance 0.025 is 2.000.

Thus, the critical-valueusing Appendix D is 2.000.

c.

Make a conclusion about the slope.

Explanation of Solution

Let

Hypotheses:

Null hypothesis:

That is, the slope is zero.

Alternative hypothesis:

That is, the slope is not equal to zero.

Decision rule:

If

If

From the output, the t-statistics is 8.183 and from part (b), the critical value at 0.05 level of significanceis 2.000.

Conclusion:

Here the t-statistics is greater than the critical value at 0.05 level of significance.

That is,

Hence, by the decision rule reject the null hypothesis.

That is, the slope is significantly different from zero.

d.

Interpret the 95% confidence interval for the slope.

Explanation of Solution

The 95% confidence interval for the slope,

Where,

From the output, the 95% confidence interval of the slope is (0.0342, 0.0563).

Interpretation:

From the confidence interval it can be concluded that there is 95% confident that the slope will lie between 0.0342 and 0.0563.

e.

Verify

Explanation of Solution

Calculation:

From the output the F statistic is 66.97.

For the slope the t-statistic is 8.183.

Hence, it can be concluded that

f.

Describe the fit of the regression.

Explanation of Solution

Calculation:

From the output, the R-squared value is 0.519.

The coefficient of determination (

The

Want to see more full solutions like this?

Chapter 12 Solutions

Loose-leaf For Applied Statistics In Business And Economics

- In a company with 80 employees, 60 earn $10.00 per hour and 20 earn $13.00 per hour. a) Determine the average hourly wage. b) In part a), is the same answer obtained if the 60 employees have an average wage of $10.00 per hour? Prove your answer.arrow_forwardThe following ordered data list shows the data speeds for cell phones used by a telephone company at an airport: A. Calculate the Measures of Central Tendency from the ungrouped data list. B. Group the data in an appropriate frequency table. 0.8 1.4 1.8 1.9 3.2 3.6 4.5 4.5 4.6 6.2 6.5 7.7 7.9 9.9 10.2 10.3 10.9 11.1 11.1 11.6 11.8 12.0 13.1 13.5 13.7 14.1 14.2 14.7 15.0 15.1 15.5 15.8 16.0 17.5 18.2 20.2 21.1 21.5 22.2 22.4 23.1 24.5 25.7 28.5 34.6 38.5 43.0 55.6 71.3 77.8arrow_forwardBusinessarrow_forward

- https://www.hawkeslearning.com/Statistics/dbs2/datasets.htmlarrow_forwardNC Current Students - North Ce X | NC Canvas Login Links - North ( X Final Exam Comprehensive x Cengage Learning x WASTAT - Final Exam - STAT → C webassign.net/web/Student/Assignment-Responses/submit?dep=36055360&tags=autosave#question3659890_9 Part (b) Draw a scatter plot of the ordered pairs. N Life Expectancy Life Expectancy 80 70 600 50 40 30 20 10 Year of 1950 1970 1990 2010 Birth O Life Expectancy Part (c) 800 70 60 50 40 30 20 10 1950 1970 1990 W ALT 林 $ # 4 R J7 Year of 2010 Birth F6 4+ 80 70 60 50 40 30 20 10 Year of 1950 1970 1990 2010 Birth Life Expectancy Ox 800 70 60 50 40 30 20 10 Year of 1950 1970 1990 2010 Birth hp P.B. KA & 7 80 % 5 H A B F10 711 N M K 744 PRT SC ALT CTRLarrow_forwardHarvard University California Institute of Technology Massachusetts Institute of Technology Stanford University Princeton University University of Cambridge University of Oxford University of California, Berkeley Imperial College London Yale University University of California, Los Angeles University of Chicago Johns Hopkins University Cornell University ETH Zurich University of Michigan University of Toronto Columbia University University of Pennsylvania Carnegie Mellon University University of Hong Kong University College London University of Washington Duke University Northwestern University University of Tokyo Georgia Institute of Technology Pohang University of Science and Technology University of California, Santa Barbara University of British Columbia University of North Carolina at Chapel Hill University of California, San Diego University of Illinois at Urbana-Champaign National University of Singapore McGill…arrow_forward

- Name Harvard University California Institute of Technology Massachusetts Institute of Technology Stanford University Princeton University University of Cambridge University of Oxford University of California, Berkeley Imperial College London Yale University University of California, Los Angeles University of Chicago Johns Hopkins University Cornell University ETH Zurich University of Michigan University of Toronto Columbia University University of Pennsylvania Carnegie Mellon University University of Hong Kong University College London University of Washington Duke University Northwestern University University of Tokyo Georgia Institute of Technology Pohang University of Science and Technology University of California, Santa Barbara University of British Columbia University of North Carolina at Chapel Hill University of California, San Diego University of Illinois at Urbana-Champaign National University of Singapore…arrow_forwardA company found that the daily sales revenue of its flagship product follows a normal distribution with a mean of $4500 and a standard deviation of $450. The company defines a "high-sales day" that is, any day with sales exceeding $4800. please provide a step by step on how to get the answers in excel Q: What percentage of days can the company expect to have "high-sales days" or sales greater than $4800? Q: What is the sales revenue threshold for the bottom 10% of days? (please note that 10% refers to the probability/area under bell curve towards the lower tail of bell curve) Provide answers in the yellow cellsarrow_forwardFind the critical value for a left-tailed test using the F distribution with a 0.025, degrees of freedom in the numerator=12, and degrees of freedom in the denominator = 50. A portion of the table of critical values of the F-distribution is provided. Click the icon to view the partial table of critical values of the F-distribution. What is the critical value? (Round to two decimal places as needed.)arrow_forward

- A retail store manager claims that the average daily sales of the store are $1,500. You aim to test whether the actual average daily sales differ significantly from this claimed value. You can provide your answer by inserting a text box and the answer must include: Null hypothesis, Alternative hypothesis, Show answer (output table/summary table), and Conclusion based on the P value. Showing the calculation is a must. If calculation is missing,so please provide a step by step on the answers Numerical answers in the yellow cellsarrow_forwardShow all workarrow_forwardShow all workarrow_forward

Functions and Change: A Modeling Approach to Coll...AlgebraISBN:9781337111348Author:Bruce Crauder, Benny Evans, Alan NoellPublisher:Cengage Learning

Functions and Change: A Modeling Approach to Coll...AlgebraISBN:9781337111348Author:Bruce Crauder, Benny Evans, Alan NoellPublisher:Cengage Learning

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill

Glencoe Algebra 1, Student Edition, 9780079039897...AlgebraISBN:9780079039897Author:CarterPublisher:McGraw Hill Algebra and Trigonometry (MindTap Course List)AlgebraISBN:9781305071742Author:James Stewart, Lothar Redlin, Saleem WatsonPublisher:Cengage Learning

Algebra and Trigonometry (MindTap Course List)AlgebraISBN:9781305071742Author:James Stewart, Lothar Redlin, Saleem WatsonPublisher:Cengage Learning Algebra & Trigonometry with Analytic GeometryAlgebraISBN:9781133382119Author:SwokowskiPublisher:Cengage

Algebra & Trigonometry with Analytic GeometryAlgebraISBN:9781133382119Author:SwokowskiPublisher:Cengage College AlgebraAlgebraISBN:9781305115545Author:James Stewart, Lothar Redlin, Saleem WatsonPublisher:Cengage Learning

College AlgebraAlgebraISBN:9781305115545Author:James Stewart, Lothar Redlin, Saleem WatsonPublisher:Cengage Learning