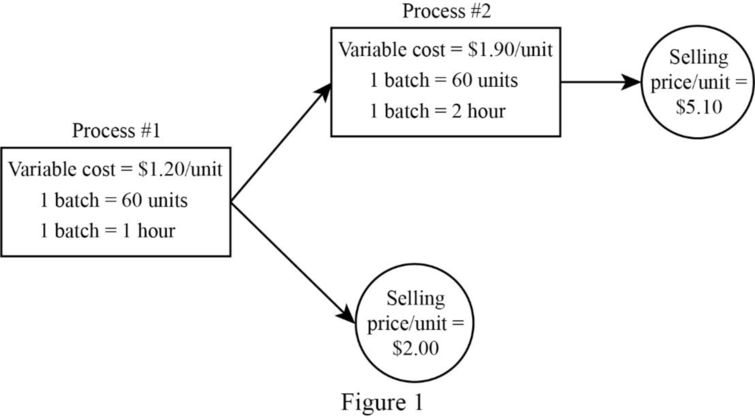

1.

Develop a schematic diagram of the two-stage production process.

1.

Explanation of Solution

Develop a schematic diagram of the two-stage production process:

Figure (1)

Note: In this case, the manufacturing

2.

Indicate whether the output price $5.10 will affect the all the sales:

2.

Explanation of Solution

In this case, the number of processing hours (Scarce resource) is limited, so the short-term objective would be to maximize the contribution margin per hour of processing time. Contribution margin per hour for output from Process 1 and Process 2 are as follows:

| Particulars | Process 1 | Process 2 |

| Net selling price per unit (a) | $ 2 | $ 5.10 |

| Less: Cost of goods sold | ||

| Direct material cost per unit | $ 1.00 | $ 1.50 |

| Direct labor cost per unit | $ 0.20 | $ 0.40 |

| Transferred in costs from process 1 | $ 0.00 | $ 1.20 |

| Total variable cost per unit (b) | $ 1.20 | $ 3.10 |

| Contribution margin per unit | $ 0.80 | $ 2.00 |

| Number of hours per unit (d) | ||

| 0.0167 | ||

| 0.0500 | ||

| Contribution margin per unit | $ 47.90 | $ 40.00 |

Table (1)

From the above calculation, it is clear that Contribution margin per unit of Process 1 output is more profitable than output from Process 2. Therefore, the short-run operating income would be maximized if all available hours were used to produce Process #1 output.

3.

Compute the lowest acceptable selling price per unit for the output from Process 2 to make this output as profitable as the output from Process 1.

3.

Explanation of Solution

Compute the lowest acceptable selling price per unit for the output from Process 2 to make this output as profitable as the output from Process 1:

| Particulars | Process 1 | Process 2 |

| Current selling price per unit | $5.10 per unit | |

| The required increase in profitability per processing hour | $ 8 | |

| Multiply by: One unit of output from Process 2 requires | 0.05 hours | |

| Increase in selling price | $0.40 | |

| Minimum selling price the output from Process 2 | $5.50 per unit |

Table (2)

4.

Compute the following, by Assuming that 50% of the total overhead costs are variable:

4.

Explanation of Solution

Compute the given by Assuming that 50% of the total overhead costs are variable:

| Particulars | Process 1 | Process 2 |

| Net selling price per unit (a) | $ 2 | $ 5.10 |

| Less: Cost of goods sold | ||

| Direct material cost per unit | $ 1.00 | $ 1.50 |

| Direct labor cost per unit | $ 0.20 | $ 0.40 |

| Variable overhead @50% | $0.30 | $0.60 |

| Transferred in costs from process 1 | $ 0.00 | $ 1.50 |

| Total variable cost per unit (b) | $ 1.50 | $4.00 |

| Contribution margin per unit | $ 0.50 | $1.10 |

| Number of hours per unit (d) | ||

| 0.0167 | ||

| 0.0500 | ||

| Contribution margin per unit | $29.94 | $22.00 |

Table (3)

From the above calculation, it is clear that the conclusion reached above in Requirement 2 still holds.

5.

Calculate the contribution margin per processing hour using the sensitivity analysis for both Process 1 output and Process 2 output under the given assumptions regarding the percentage of variable overhead costs: 0%, 25%, 50%, and 100%. Perform these calculations for Process 2 output both for a selling price of $5.10 per unit and a selling price of $5.50 per unit.

State the general conclusion that could be drawn on the basis of this sensitivity analysis.

5.

Explanation of Solution

| Contribution margin or processing hour | ||||||

| % VOH | ||||||

| P1 | P2 | Δ | P1 | P2 | Δ | |

| 0% | $48.00 | $40.00 | $4.00 | $48.00 | $58.00 | $10.00 |

| 25% | $39.00 | $31.00 | $8.00 | $39.00 | $49.00 | $10.00 |

| 50% | $30.00 | $22.00 | $8.00 | $30.00 | $40.00 | $10.00 |

| 100% | $12.00 | $4.00 | $8.00 | $12.00 | $22.00 | $10.00 |

Table (4)

In this case, the sensitivity analysis aids to explain the result obtained in Requirement 4, and when Process #2 output uses three times as much processing time per unit, when compared to Process #1. This is independent of selling prices and the composition of variable overhead. Moreover, the amount of variable overhead charged per unit of Process #2 output is always three times as much variable overhead charged per unit of output from Process #1.

Since these ratios are “constant across selling prices per unit for output from Process #2 and also constant across levels of variable overhead, the difference in contribution margin per hour between Process #1 and Process #2 output, at each assumed selling price per unit for Process #2 output, will be constant and independent of the proportion of total overhead that is variable”.

Want to see more full solutions like this?

Chapter 11 Solutions

Cost Management: A Strategic Emphasis

- Hello tutor please given General accounting question answer do fast and properly explain all answerarrow_forwardQuintana Corporation projected current year sales of 42,000 units at a unit sale price of $32.50. Actual current year sales were 39,500 units at $33.75 per unit. Actual variable costs, budgeted at $22.75 per unit, totaled $21.90 per unit. Budgeted fixed costs totaled $375,000, while actual fixed costs amounted to $392,000. What is the sales volume variance for total revenue? I want answerarrow_forwardWhat is hemingway corporation taxable income?arrow_forward

- Please given correct answer for General accounting question I need step by step explanationarrow_forwardArmour vacation cabin was destroyed by a wildfire. He had purchased the cabin 14 months ago for $625,000. He received $890,000 from his insurance company to replace the cabin. If he fails to rebuild the cabin or acquire a replacement property in the required time, how much gain must he recognize on this conversion? A. $375,000 B. $160,000 C. $265,000 D. $0 E. None of the above helparrow_forwardI am looking for the correct answer to this financial accounting question with appropriate explanations.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education