(a)

To Discuss:

A 30-year maturity bond making annual coupon payments with a coupon rate of 12% has duration of 11.54 years and convexity of 192.4. The bond currently sells at a yield to maturity of 8%.

To use a financial calculator or spreadsheet to find the price of the bond if its yield to maturity falls to 7%.

Introduction:

When specified payments are made by the issuer to the holder for a given period of time due to an obligation created by a security,then that security is known as Bond.The amount the holder will receive on maturity along with the coupon rate which is also known as the interest rate of the bond is known as the face value of the bond.The discount rate due to which the present payments from the bond become equal to its price i.e. it is the average

The time taken by the bond to change based on the interest rate changes is displayed by Convexity. Duration measures approximately a

Answer to Problem 26PS

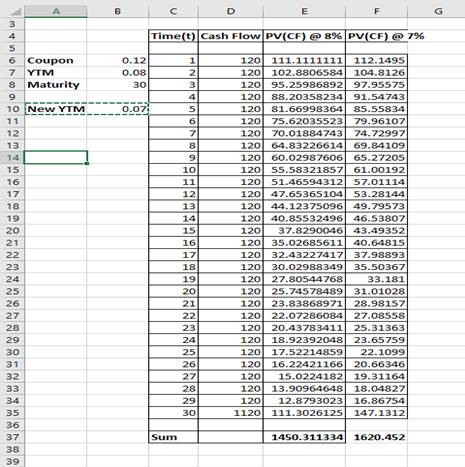

Price of Bond using a financial calculator if yield to maturity falls to 7% is 1620.45.

Explanation of Solution

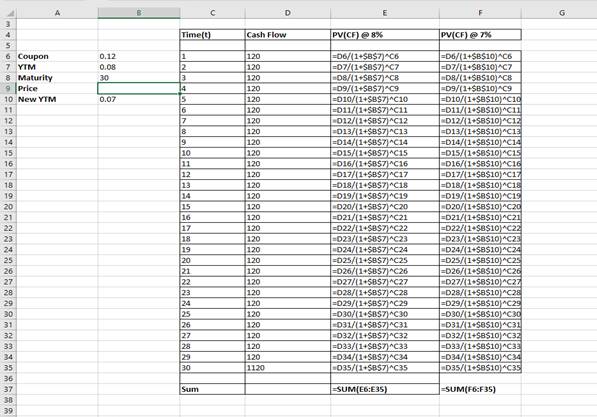

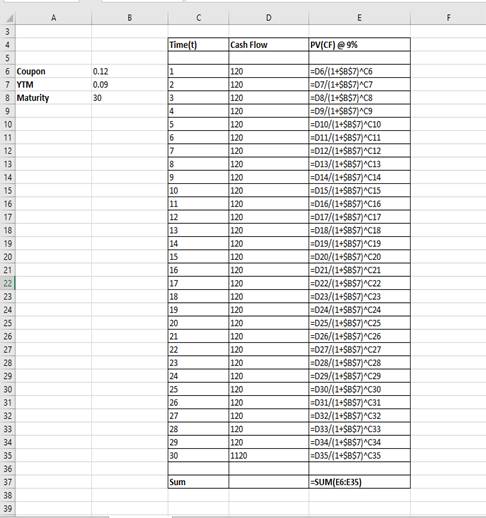

Price of the bond when the yield to maturity is 8% using a financial calculator can be calculated as below:

So, the price of the bond with 8% yield is 1450.31.

So, the price of the bond with 7% yield is 1620.45.

(b)

To Discuss:

A 30-year maturity bond making annual coupon payments with a coupon rate of 12% has duration of 11.54 years and convexity of 192.4The bond currently sells at a yield to maturity of 8%.

To predict the price using the duration rule.

Introduction:

When specified payments are made by the issuer to the holder for a given period of time due to an obligation created by a security, then that security is known as Bond. The amount the holder will receive on maturity along with the coupon rate which is also known as the interest rate of the bond is known as the face value of the bond. The discount rate due to which the present payments from the bond become equal to its price i.e. it is the average rate of return which a holder can expect from a bond, is known as Yield to Maturity.

The time taken by the bond to change based on the interest rate changes are displayed by Convexity.

Duration measures approximately a bond's price sensitivity to interest rates changes.

Answer to Problem 26PS

Price of Bond using the duration rule if yield to maturity falls to 7% is 1605.28.

Explanation of Solution

The price of the bond with 8% yield is 1450.31.

Price of the Bond using the duration rule, if yield to maturity falls to 7%:

Predicted Price change =

=

=154.97

Predicted new price=1450.31+154.97=1605.28

(c)

To Discuss:

A 30-year maturity bond making annual coupon payments with a coupon rate of 12% has duration of 11.54 years and convexity of 192.4.The bond currently sells at a yield to maturity of 8%.

To predict the price using the duration with convexity rule.

Introduction:

When specified payments are made by the issuer to the holder for a given period of time due to an obligation created by a security,then that security is known as Bond.The amount the holder will receive on maturity along with the coupon rate which is also known as the interest rate of the bond is known as the face value of the bond.The discount rate due to which the present payments from the bond become equal to its price i.e. it is the average rate of return which a holder can expect from a bond,is known as Yield to Maturity.

The time taken by the bond to change based on the interest rate changes is displayed by Convexity. Duration measures approximately a bond's price sensitivity to interest rates changes.

Answer to Problem 26PS

Price of Bond using the duration with convexity rule if yield to maturity falls to 7% is 1619.23.

Explanation of Solution

So, the price of the bond with 8% yield is 1450.31.

Price of the Bond using Duration-with-Convexity Rule, if yield to maturity falls to 7%:

Predicted price change =

=

=168.92

Predicted new price=1450.31+168.92=1619.23

(d)

To Discuss:

A 30-year maturity bond making annual coupon payments with a coupon rate of 12% has duration of 11.54 years and convexity of 192.4. The bond currently sells at a yield to maturity of 8%.

To determine the percent error for each rule and to conclude about the accuracy of the two rules.

Introduction:

When specified payments are made by the issuer to the holder for a given period of time due to an obligation created by a security,then that security is known as Bond.The amount the holder will receive on maturity along with the coupon rate which is also known as the interest rate of the bond is known as the face value of the bond.The discount rate due to which the present payments from the bond become equal to its price i.e. it is the average rate of return which a holder can expect from a bond,is known as Yield to Maturity.

The time taken by the bond to change based on the interest rate changes is displayed by Convexity. Duration measures approximately a bond's price sensitivity to interest rates changes.

Answer to Problem 26PS

The percentage error of duration rule is -.98% and percentage error of duration with convexity rule is -.075%.

Conclusion: The duration-with-convexity rule provides more accurate approximations tothe true change in price.

Explanation of Solution

Percent error for duration rule =

= -0.0094

= -0.94%

Percent error for duration with convexity rule=

= -0.00075

= -0.075%

The duration-with-convexity rule provides more accurate approximations to

the true change in price.

Conclusion: The percentage error using convexity with duration is less than one-tenth the error using only duration to estimate the price change.

(e)

To Discuss:

A 30-year maturity bond making annual coupon payments with a coupon rate of 12% has duration of 11.54 years and convexity of 192.4The bond currently sells at a yield to maturity of 8%.

To repeat the analysis if the bond's yield to maturity increases to 9% and to determine whether the conclusions about the accuracy of the two rules with parts (a)-(d) were consistent.

Introduction:

When specified payments are made by the issuer to the holder for a given period of time due to an obligation created by a security,then that security is known as Bond.The amount the holder will receive on maturity along with the coupon rate which is also known as the interest rate of the bond is known as the face value of the bond.The discount rate due to which the present payments from the bond become equal to its price i.e. it is the average rate of return which a holder can expect from a bond,is known as Yield to Maturity.

The time taken by the bond to change based on the interest rate changes is displayed by Convexity. Duration measures approximately a bond's price sensitivity to interest rates changes.

Answer to Problem 26PS

The conclusions about the accuracy of the two rules with parts (a)-(d) were consistent on repeating the analysis if the bond's yield to maturity increases to 9%.

Explanation of Solution

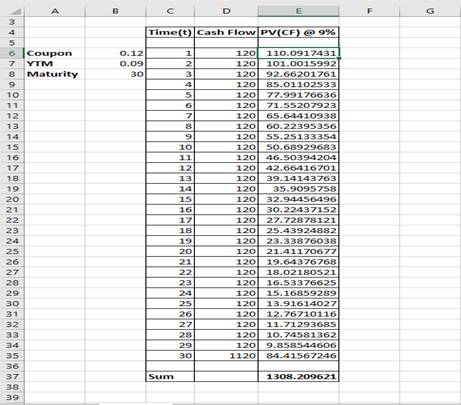

So, the price of the bond with 9% yield is 1308.21.

Price of the Bond using the duration rule, if yield to maturity rises to 9%:

Predicted Price change =

=

=-154.97

Predicted new price=1450.31-154.97

=1295.34

Percent error=

= -0.0098

= -0.98%

Price of the Bond using Duration-with-Convexity Rule, if yield to maturity rises to 9%:

Predicted price change =

=

= -141.02

Predicted new price=1450.31-141.02=1309.29

Percent error=

=0.00083

=0.083%

The percentage error using convexity with duration is less than one-tenth the error using only duration to estimate the price change.

The previous conclusion about the duration with convexity rule being more accurate is consistent with parts (a) - (d) if the bond's yield to maturity rises to 9%.

Want to see more full solutions like this?

Chapter 11 Solutions

Connect 1-Semester Access Card for Essentials of Investments

- What are AIrbnb's Legal Foundations? What are Airbnb's Business Ethics? What are Airbnb's Corporate Social Responsibility?arrow_forwardDiscuss in detail the differences between the Primary Markets versus the Secondary Markets, The Money Market versus the Capital Market AND the Spot Market versus the Futures Market. Additionally, discuss the various Interest Rate Determinants listed in your textbook (such as default-risk premium.....).arrow_forwardHow can the book value still serve as a useful metric for investors despite the dominance of market value?arrow_forward

- How do you think companies can practically ensure that stakeholder interests are genuinely considered, while still prioritizing the financial goal of maximizing shareholder equity? Do you think there’s a way to measure and track this balance effectively?arrow_forward$5,000 received each year for five years on the first day of each year if your investments pay 6 percent compounded annually. $5,000 received each quarter for five years on the first day of each quarter if your investments pay 6 percent compounded quarterly. Can you show me either by hand or using a financial calculator please.arrow_forwardCan you solve these questions on a financial calculator: $5,000 received each year for five years on the last day of each year if your investments pay 6 percent compounded annually. $5,000 received each quarter for five years on the last day of each quarter if your investments pay 6 percent compounded quarterly.arrow_forward

- Now suppose Elijah offers a discount on subsequent rooms for each house, such that he charges $40 for his frist room, $35 for his second, and $25 for each room thereafter. Assume 30% of his clients have only one room cleaned, 25% have two rooms cleaned, 30% have three rooms cleaned, and the remaining 15% have four rooms cleaned. How many houses will he have to clean before breaking even? If taxes are 25% of profits, how many rooms will he have to clean before making $15,000 profit? Answer the question by making a CVP worksheet similar to the depreciation sheets. Make sure it works well, uses cell references and functions/formulas when appropriate, and looks nice.arrow_forward1. Answer the following and cite references. • what is the whole overview of Green Markets (Regional or Sectoral Stock Markets)? • what is the green energy equities, green bonds, and green financing and how is this related in Green Markets (Regional or Sectoral Stock Markets)? Give a detailed explanation of each of them.arrow_forwardCould you help explain “How an exploratory case study could be goodness of work that is pleasing to the Lord?”arrow_forward

- What are the case study types and could you help explain and make an applicable example.What are the 4 primary case study designs/structures (formats)?arrow_forwardThe Fortune Company is considering a new investment. Financial projections for the investment are tabulated below. The corporate tax rate is 24 percent. Assume all sales revenue is received in cash, all operating costs and income taxes are paid in cash, and all cash flows occur at the end of the year. All net working capital is recovered at the end of the project. Year 0 Year 1 Year 2 Year 3 Year 4 Investment $ 28,000 Sales revenue $ 14,500 $ 15,000 $ 15,500 $ 12,500 Operating costs 3,100 3,200 3,300 2,500 Depreciation 7,000 7,000 7,000 7,000 Net working capital spending 340 390 440 340 ?arrow_forwardWhat are the six types of alternative case study compositional structures (formats)used for research purposes, such as: 1. Linear-Analytical, 2. Comparative, 3. Chronological, 4. Theory Building, 5. Suspense and 6. Unsequenced. Please explainarrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education