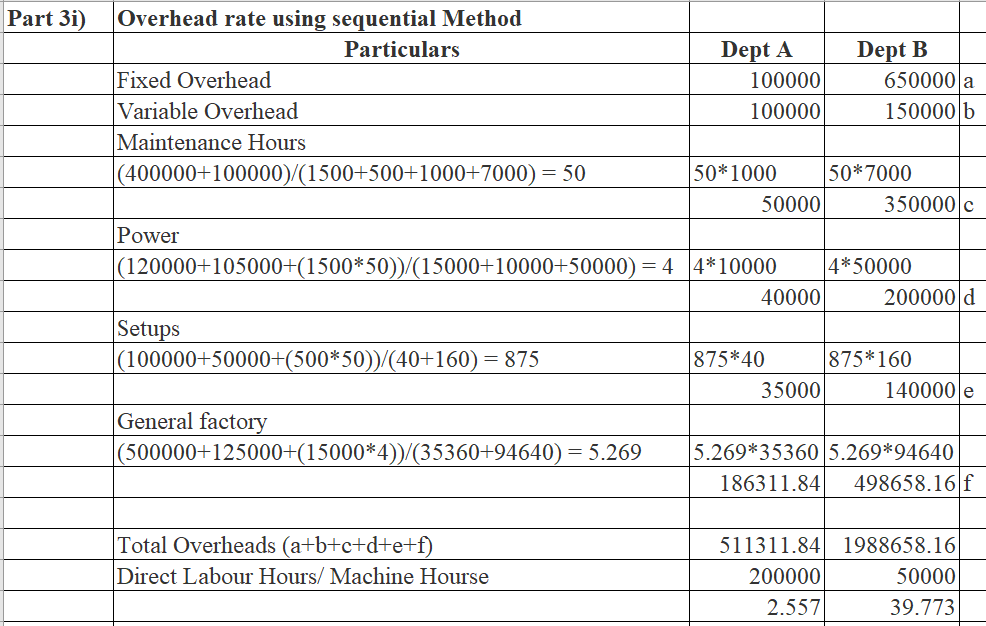

Recently, the sales and marketing manager for Pasifika Company, Mr. Reece Rooney couldn’t understand the result of two bids that the firm has submitted. According to the company’s policy, a 50 percent mark-up is added to the full manufacturing cost when calculating the bid. One particular job (Job A01) had been rejected by a prospective customer since the proposed bid was $4 per unit higher than the winning bid. However, a customer has accepted a second job (Job B01) and was pleased with the favorable bid. This customer revealed that Pasifika’s price was $44 per unit lower than the next-lowest bid. Reece knew that the implementation of the cost leadership strategy has resulted in Pasifika’s competitive advantage, therefore he assumed that the issue must be related to cost allocation procedures. When Reece further investigated the matter, he found that Pasifika used a pre-determined plantwide overhead rate based on direct labor hours. The budgeted data used to calculate this rate follows: Department A Department B Total Fixed Overhead $300,000 $1,400,000 $ 1,700,000 Variable Overhead $1 per DLH $5 per MH Direct labor hours 200000 50000 250000 Machine hours 20000 120000 140000 Additional information on the two jobs are as follows: Job A01 Department A Department B Total Direct labor hours 5000 1000 6000 Machine hours 200 500 700 Prime costs $100,000 $20,000 $120,000 Units produced 14400 14400 14400 Job B01 Department A Department B Total Direct labor hours 400 600 1000 Machine hours 200 3000 3200 Prime costs $10,000 $40,000 $50,000 Units produced 1500 1500 1500 In his attempt to investigate the costing of the two jobs, Mr. Rooney discovered that the overhead costs in the two departments are different. In particular, the overhead costs of Department B were higher than Department A since it uses more equipment and therefore has higher maintenance, higher power consumption, higher depreciation, and higher setup costs. Additionally, he did some reading on overhead cost allocation methods and found that allocating support department cost appropriately can result to increase accuracy of the product cost. Hence he collected the following information on four support departments as follows: Maintenance Power Setups General Factory Dept.A Dept. B Fixed overhead $400,000 $120,000 $100,000 $500,000 $100,000 $650,000.0 Variable overhead $100,000.0 $105,000.0 $50,000.0 $125,000.0 $100,000.0 $150,000.0 Maintenance hours - $ 1,500 $ 500 - $ 1,000 $ 7,000 Kilowatt-hours $ 4,500 - - 15000 10000 $ 50,000 Direct labor hours $ 10,000 $ 12,000 $ 6,000 $ 8,000 $ 200,000 $ 50,000 Number of setups - - - - 40 $ 160 Square feet $ 25,000 $ 40,000 $ 5,000 $ 15,000 $ 35,360 $ 94,640 The following allocation bases (cost drivers) seemed reasonable: Support Department Allocation Base Maintenance Maintenance hours Power Kilowatt-hours Setups Number of setups General Factory Square feet REQUIRED Advise Mr. Rooney on potential strategies he would implement to compete effectively on cost leadership strategy. Calculate the unit bids for the two jobs using a plantwide OH rate based on direct labour hours. (i) Using the sequential (step-down) method, calculate the departmental overhead rates using direct labor hours for Department A and machine hours for Department B. (ii) What would the unit bids for Job A01and Job A02 have been if these overhead rates had been in effect? (Round-off the allocation ratios to 3 decimal places before you allocate the support department costs 4. Discuss any recommendations you would give to Rooney regarding the method of allocating overhead cost. sub-parts to be 3. & 4. to be solved.

Recently, the sales and marketing manager for Pasifika Company, Mr. Reece Rooney couldn’t understand the result of two bids that the firm has submitted. According to the company’s policy, a 50 percent mark-up is added to the full

However, a customer has accepted a second job (Job B01) and was pleased with the favorable bid. This customer revealed that Pasifika’s price was $44 per unit lower than the next-lowest bid. Reece knew that the implementation of the cost leadership strategy has resulted in Pasifika’s competitive advantage, therefore he assumed that the issue must be related to cost allocation procedures. When Reece further investigated the matter, he found that Pasifika used a pre-determined plantwide overhead rate based on direct labor hours. The budgeted data used to calculate this rate follows:

|

|

Department A |

Department B |

Total |

|

Fixed Overhead |

$300,000 |

$1,400,000 |

$ 1,700,000 |

|

Variable Overhead |

$1 per DLH |

$5 per MH |

|

|

Direct labor hours |

200000 |

50000 |

250000 |

|

Machine hours |

20000 |

120000 |

140000 |

Additional information on the two jobs are as follows:

|

Job A01 |

Department A |

Department B |

Total |

|

Direct labor hours |

5000 |

1000 |

6000 |

|

Machine hours |

200 |

500 |

700 |

|

Prime costs |

$100,000 |

$20,000 |

$120,000 |

|

Units produced |

14400 |

14400 |

14400 |

|

Job B01 |

Department A |

Department B |

Total |

|

Direct labor hours |

400 |

600 |

1000 |

|

Machine hours |

200 |

3000 |

3200 |

|

Prime costs |

$10,000 |

$40,000 |

$50,000 |

|

Units produced |

1500 |

1500 |

1500 |

In his attempt to investigate the costing of the two jobs, Mr. Rooney discovered that the overhead costs in the two departments are different. In particular, the overhead costs of Department B were higher than Department A since it uses more equipment and therefore has higher maintenance, higher power consumption, higher

|

|

Maintenance |

Power |

Setups |

General Factory |

Dept.A |

Dept. B |

|

Fixed overhead |

$400,000 |

$120,000 |

$100,000 |

$500,000 |

$100,000 |

$650,000.0 |

|

Variable overhead |

$100,000.0 |

$105,000.0 |

$50,000.0 |

$125,000.0 |

$100,000.0 |

$150,000.0 |

|

Maintenance hours |

- |

$ 1,500 |

$ 500 |

- |

$ 1,000 |

$ 7,000 |

|

Kilowatt-hours |

$ 4,500 |

- |

- |

15000 |

10000 |

$ 50,000 |

|

Direct labor hours |

$ 10,000 |

$ 12,000 |

$ 6,000 |

$ 8,000 |

$ 200,000 |

$ 50,000 |

|

Number of setups |

- |

- |

- |

- |

40 |

$ 160 |

|

Square feet |

$ 25,000 |

$ 40,000 |

$ 5,000 |

$ 15,000 |

$ 35,360 |

$ 94,640 |

The following allocation bases (cost drivers) seemed reasonable:

Support Department Allocation Base

Maintenance Maintenance hours

Power Kilowatt-hours

Setups Number of setups

General Factory Square feet

REQUIRED

- Advise Mr. Rooney on potential strategies he would implement to compete effectively on cost leadership strategy.

- Calculate the unit bids for the two jobs using a plantwide OH rate based on direct labour hours.

- (i) Using the sequential (step-down) method, calculate the departmental overhead rates using direct labor hours for Department A and machine hours for Department B.

(ii) What would the unit bids for Job A01and Job A02 have been if these overhead rates had been in effect? (Round-off the allocation ratios to 3 decimal places before you allocate the support department costs

4. Discuss any recommendations you would give to Rooney regarding the method of allocating overhead cost.

sub-parts to be 3. & 4. to be solved.

Step by step

Solved in 2 steps with 3 images