4. A decision-maker with initial wealth w faces a probability of incurring a loss. If the loss occurs, with probability p the amount of the loss is ₁ and with probability 1-p the amount of the loss is £2, where ₁ > ₂ > 0. The decision-maker can buy insurance against both losses at a price of q dollars per unit. If she purchases a units of insurance, she receives a dollars if either loss occurs, even if z is greater than the amount of the loss. There is no limit to the amount of insurance she can purchase. (a) First suppose that the decision-maker is a risk averse expected utility maximizer with von Neumann-Morgenstern utility u(y) over quantities of wealth y. i. () Write down the first-order condition characterizing the optimal choice of a when it is interior. Solution: The first-order condition is (1-q)πpu' (w-l₁ + (1 − q)x)+(1−q)π(1−p)u' (w − l₂ + (1 — q)x) = q (1-7)u' (w-qx). ii. (, Is the highest price q at which the decision-maker fully insures against the larger loss ₁ greater than, equal to, or less than ? Prove your answer. Solution: At q = n, the above FOC simplifies to pu' (wl₁ + (1-q)x)+ (1 − p)u' (w−l₂ + (1 − q)x) = u'(w — qx). If x= ₁, the left-hand side of this equation is smaller than the right-hand side. Since u' is decreasing, we must have x < ₁ for this equation to hold as decreasing x causes the left-hand side to increase and the right-hand side to decrease. (This argument implicitly assumes that p1; if p = 1 then this is essentially a standard insurance problem and r = l₁ is optimal when q = n.)

4. A decision-maker with initial wealth w faces a probability of incurring a loss. If the loss occurs, with probability p the amount of the loss is ₁ and with probability 1-p the amount of the loss is £2, where ₁ > ₂ > 0. The decision-maker can buy insurance against both losses at a price of q dollars per unit. If she purchases a units of insurance, she receives a dollars if either loss occurs, even if z is greater than the amount of the loss. There is no limit to the amount of insurance she can purchase. (a) First suppose that the decision-maker is a risk averse expected utility maximizer with von Neumann-Morgenstern utility u(y) over quantities of wealth y. i. () Write down the first-order condition characterizing the optimal choice of a when it is interior. Solution: The first-order condition is (1-q)πpu' (w-l₁ + (1 − q)x)+(1−q)π(1−p)u' (w − l₂ + (1 — q)x) = q (1-7)u' (w-qx). ii. (, Is the highest price q at which the decision-maker fully insures against the larger loss ₁ greater than, equal to, or less than ? Prove your answer. Solution: At q = n, the above FOC simplifies to pu' (wl₁ + (1-q)x)+ (1 − p)u' (w−l₂ + (1 − q)x) = u'(w — qx). If x= ₁, the left-hand side of this equation is smaller than the right-hand side. Since u' is decreasing, we must have x < ₁ for this equation to hold as decreasing x causes the left-hand side to increase and the right-hand side to decrease. (This argument implicitly assumes that p1; if p = 1 then this is essentially a standard insurance problem and r = l₁ is optimal when q = n.)

Oh no! Our experts couldn't answer your question.

Don't worry! We won't leave you hanging. Plus, we're giving you back one question for the inconvenience.

Submit your question and receive a step-by-step explanation from our experts in as fast as 30 minutes.

You have no more questions left.

Message from our expert:

Our experts are unable to provide you with a solution at this time. Try rewording your question, and make sure to submit one question at a time. We've credited a question to your account.

Your Question:

how to derive the First Order Condition fomula?

how to solve? the other parts

why the q=πNow by simplyfying the above FOC At the q=πNow by simplyfying the above FOC

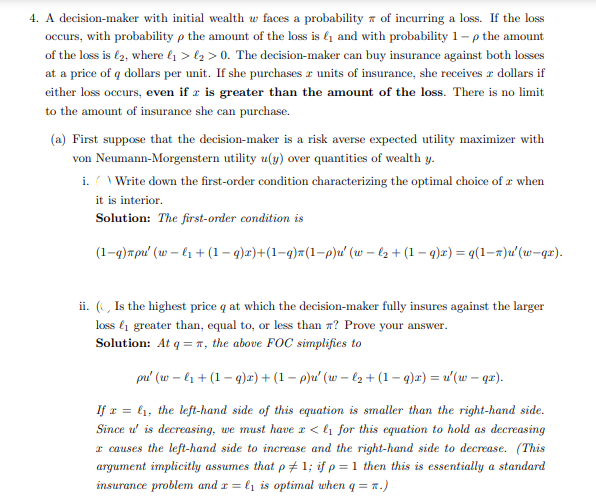

Transcribed Image Text:4. A decision-maker with initial wealth w faces a probability of incurring a loss. If the loss

occurs, with probability p the amount of the loss is ₁ and with probability 1-p the amount

of the loss is £2, where ₁ > ₂ > 0. The decision-maker can buy insurance against both losses

at a price of q dollars per unit. If she purchases a units of insurance, she receives a dollars if

either loss occurs, even if z is greater than the amount of the loss. There is no limit

to the amount of insurance she can purchase.

(a) First suppose that the decision-maker is a risk averse expected utility maximizer with

von Neumann-Morgenstern utility u(y) over quantities of wealth y.

i. () Write down the first-order condition characterizing the optimal choice of a when

it is interior.

Solution: The first-order condition is

(1-q)πpu' (w-l₁ + (1 − q)x)+(1−q)π(1−p)u' (w − l₂ + (1 — q)x) = q (1-7)u' (w-qx).

ii. (, Is the highest price q at which the decision-maker fully insures against the larger

loss ₁ greater than, equal to, or less than ? Prove your answer.

Solution: At q = n, the above FOC simplifies to

pu' (wl₁ + (1-q)x)+ (1 − p)u' (w−l₂ + (1 − q)x) = u'(w — qx).

If x= ₁, the left-hand side of this equation is smaller than the right-hand side.

Since u' is decreasing, we must have x < ₁ for this equation to hold as decreasing

x causes the left-hand side to increase and the right-hand side to decrease. (This

argument implicitly assumes that p1; if p = 1 then this is essentially a standard

insurance problem and r = l₁ is optimal when q = n.)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Recommended textbooks for you

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours…

Economics

ISBN:

9781337091985

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Essentials of Economics (MindTap Course List)

Economics

ISBN:

9781337091992

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning

Brief Principles of Macroeconomics (MindTap Cours…

Economics

ISBN:

9781337091985

Author:

N. Gregory Mankiw

Publisher:

Cengage Learning