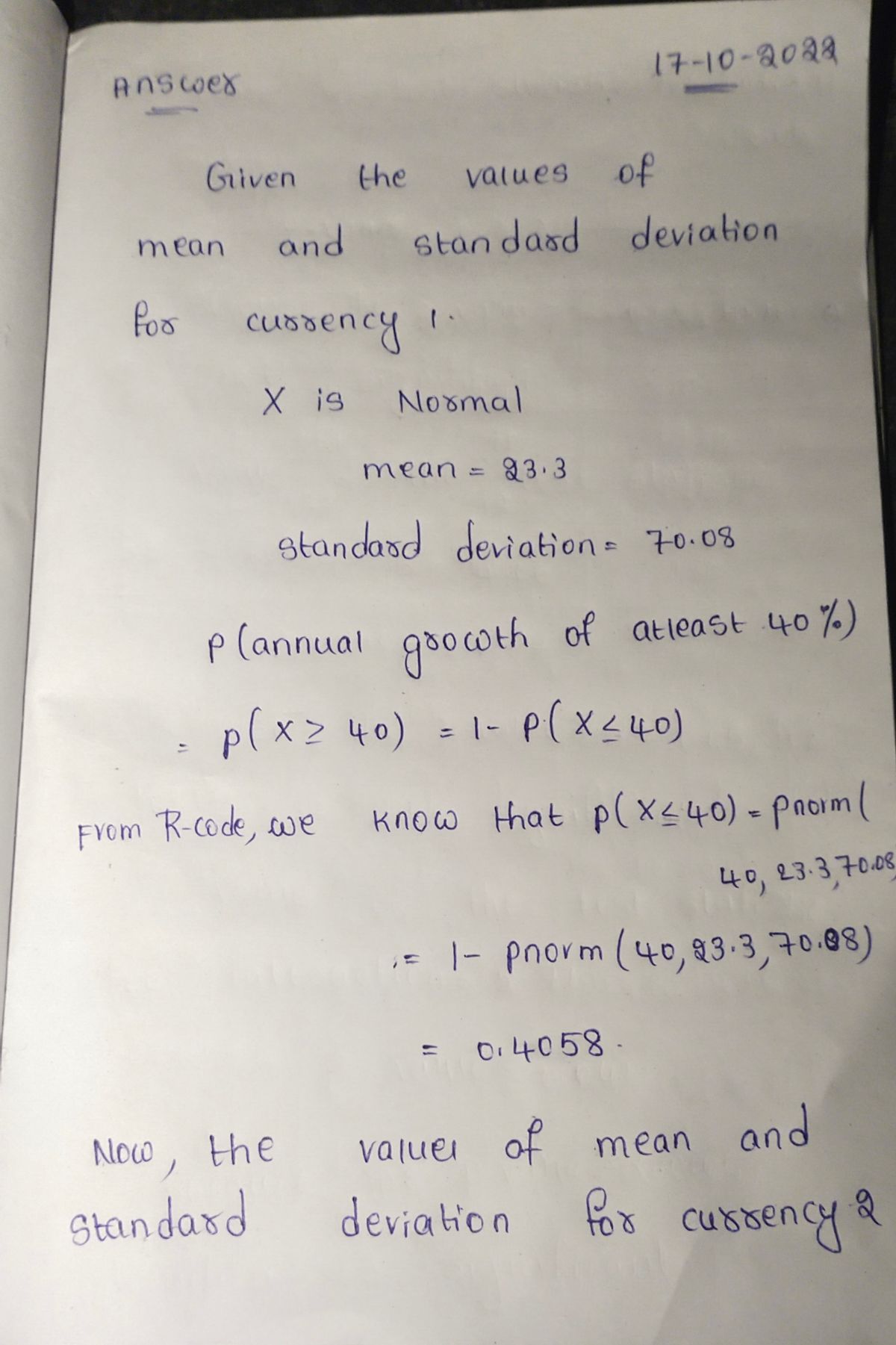

5. Changes in the value of two particular cryptocurrencies are modelled as Normal distributions. From year to year, the first cryptocurrency changes in value with mean 23.30% and standard deviation 70.08%. From year to year, the second cryptocurrency changes in value with 1 mean 46.40% and standard deviation 149.69%. An investor is hoping for an annual growth in value of at least 40%. Which currency is most likely to give an annual growth of at least 40%?

5. Changes in the value of two particular cryptocurrencies are modelled as Normal distributions. From year to year, the first cryptocurrency changes in value with mean 23.30% and standard deviation 70.08%. From year to year, the second cryptocurrency changes in value with 1 mean 46.40% and standard deviation 149.69%. An investor is hoping for an annual growth in value of at least 40%. Which currency is most likely to give an annual growth of at least 40%?

A First Course in Probability (10th Edition)

10th Edition

ISBN:9780134753119

Author:Sheldon Ross

Publisher:Sheldon Ross

Chapter1: Combinatorial Analysis

Section: Chapter Questions

Problem 1.1P: a. How many different 7-place license plates are possible if the first 2 places are for letters and...

Related questions

Question

Transcribed Image Text:5. Changes in the value of two particular cryptocurrencies are modelled

as Normal distributions. From year to year, the first cryptocurrency

changes in value with mean 23.30% and standard deviation 70.08%.

From year to year, the second cryptocurrency changes in value with

1

mean 46.40% and standard deviation 149.69%. An investor is hoping

for an annual growth in value of at least 40%. Which currency is most

likely to give an annual growth of at least 40%?

Expert Solution

Step 1

Step by step

Solved in 2 steps with 2 images

Recommended textbooks for you

A First Course in Probability (10th Edition)

Probability

ISBN:

9780134753119

Author:

Sheldon Ross

Publisher:

PEARSON

A First Course in Probability (10th Edition)

Probability

ISBN:

9780134753119

Author:

Sheldon Ross

Publisher:

PEARSON