1.

Compute the contribution margin per unit and the breakeven point in units for the Flex 1000 panel, before and after the proposed reengineering project.

1.

Explanation of Solution

Compute the contribution margin per unit and the breakeven point in units for the Flex 1000 panel, before and after the proposed reengineering project.

| Particulars | Current | Proposed |

| Selling price per unit | $600.00 | $600.00 |

| Less: Variable costs per unit | ||

| Materials and purchased parts | 180.00 | 195.00 |

| Direct labor | 55.00 | 62.50 |

| Variable | 70.00 | 80.00 |

| Variable GSA per unit | 25.00 | 25.00 |

| Total variable cost per unit | $330.00 | $362.50 |

| Contribution margin per unit (CONTRIBUTION MARGIN) | $270.00 | $237.50 |

|

Total fixed costs per year: | ||

| Fixed manufacturing overhead per unit | $90 | $55 |

| Multiply: Number of units | 380,000 | 380,000 |

| Fixed manufacturing overhead | $34,200,000 | $20,900,000 |

| Fixed General Selling and Administrative costs | $2,050,000 | $2,050,000 |

| Total fixed costs per year (F) | $36,250,000 | $22,950,000 |

| Breakeven in units | 134,260 | 96,632 |

Table (1)

2.

Determine the indifference point in terms of number of sales units between the current manufacturing plan and the proposed plan of Company SF.

2.

Explanation of Solution

Determine the indifference point in terms of number of sales units between the current manufacturing plan and the proposed plan of Company SF.

The cost indifference point is Q. The cost function for the current plan and proposed plan are given below:

From the above calculation, the firm would prefer the low fixed cost strategy at the current level of 380,000 units.

3.

Describe the (a) strategy of Company SF and (b) whether Company SF should undertake the proposed reengineering plan.

3.

Explanation of Solution

(a) The strategy of Company SF can be explained as follows:

The strategy of Company SF is best described as differentiation as the firm has achieved success through the innovation in its product design. Moreover, the firm belongs to an industry where innovation and product design is a key factor for success. The technology used by Company SF is an important strategy that has been challenging for the firms operating in the same industry. Company SF should consider the existence of significant level of risk in the failure of meeting the customer’s expectation. Company SF has to design and implement a strategy that would enhance the innovation of the company in the market and also safeguard the possibility of losses from the failure of technology.

(b) whether the company should select the proposed re-engineering plan:

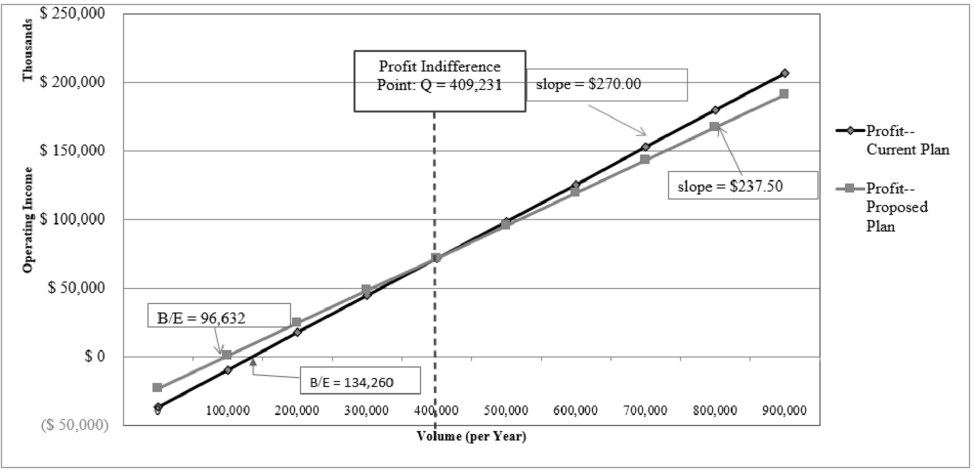

The calculations in requirement 2 to select the new plan, at the current level of 380,000 units because costs are lower for the new plan, and will continue to be lower for the new plan as long as volume stays below 409,231 units. The 409,231 point of indifference is computed using the information below.

| Particulars | Current | Proposed | Difference |

| Contribution Margin (CONTRIBUTION MARGIN) | $270.00 | $237.50 | $32.50 |

| Fixed Cost (F) | $36,250,000 | $22,950,000 | $13,300,000 |

| Indifference Point | 409,231 units | ||

Table (2)

Strategically, the new plan will be preferred because it is an appropriate response to the firm’s risk, as determined in requirement 1. The reduction in the operating leverage (

Therefore, a strategy that emphasizes less manufacturing and enhances the product design and development would be more reliable.

4.

Prepare a chart (single graph) representing the profit-volume equation for each of the two decision alternatives.

4.

Explanation of Solution

Prepare a chart (single graph) representing the profit-volume equation for each of the two decision alternatives.

Figure (1)

The chart has been prepared based on the table (1):

| Assumed Levels of Demand | Profit-Current | Profit-Proposed |

| 0 | ($ 36,250,000) | ($ 22,950,000) |

| 100,000 | ($ 9,250,000) | $ 800,000 |

| 200,000 | $ 17,750,000 | $ 24,550,000 |

| 300,000 | $ 44,750,000 | $ 48,300,000 |

| 400,000 | $ 71,750,000 | $ 72,050,000 |

| 500,000 | $ 98,750,000 | $ 95,800,000 |

| 600,000 | $ 125,750,000 | $ 119,550,000 |

| 700,000 | $ 152,750,000 | $ 143,300,000 |

| 800,000 | $ 179,750,000 | $ 167,050,000 |

| 900,000 | $ 206,750,000 | $ 190,800,000 |

Table (3)

Note: The data is computed by using the formula:

5.

Compute and interpret the degree of operating leverage (DOL) for each decision alternative.

5.

Explanation of Solution

Compute the degree of operating leverage (DOL) for each decision alternative.

| Degree of Operating Leverage | |||

| Volume Q | Current | Proposed | |

| 400,000 | 1.51 | 1.32 | |

| 600,000 | 1.29 | 1.19 | |

| DOL components (Current) | |||

| Volume Q | Contribution Margin | Operating income | DOL |

| 400,000 | $108,000,000 | $71,750,000 | 1.51 |

| 600,000 | $162,000,000 | $125,750,000 | 1.29 |

| DOL components (Proposed) | |||

| Volume Q | Contribution Margin | Operating income | |

| 400,000 | $95,000,000 | $72,050,000 | 1.32 |

| 600,000 | $142,500,000 | $119,550,000 | 1.19 |

. Table (4)

Operating leverage refers to the extent to which fixed costs characterize an organization’s cost structure. The greater the fixed costs, the greater the operating leverage and more profits are sensitive to changes in volume of sales.

Degree of Operating leverage (DOL) is the percentage change in operating profit per percentage change in sales. Thus, for the results above, a DOL of 1.51 means that from a volume level (Q) of 400,000 units per year, each percentage change in sales volume under the current production plan would reflect a 1.51% change in operating income. At this same level of Q, the DOL for the proposed plan is 1.32. Therefore, the existing manufacturing plan has more operating leverage, which in turn means that at any output level, Q, the DOL will be higher than the corresponding DOL under the proposed manufacturing plan.

The current plan would generate higher percentage reductions in operating income if sales volume declines as compared to the proposed plan, but greater percentage increases in operating income in response to increases in sales volume.

Want to see more full solutions like this?

Chapter 9 Solutions

Cost Management: A Strategic Emphasis

- Blossom Corporation issues 72000 shares of $50 par value preferred stock for cash at $60 per share. The entry to record the transaction will consist of a debit to Cash for $4320000 and a credit or credits to ○ Preferred Stock for $4320000 ○ Preferred Stock for $3600000 and Paid-in Capital in Excess of Par-Preferred Stock for $720000 ○ Preferred Stock for $3600000 and Retained Earnings for $720000 ○ Paid-in Capital from Preferred Stock for $4320000arrow_forwardThe current sections of Kingbird Inc's balance sheets at December 31, 2024 and 2025, are presented here. Kingbird's net income for 2025 was $107,100. Depreciation expense was $18,900. 2025 2024 Current assets Cash $73,500 $69,300 Accounts receivable 56,000 62,300 Inventory 117,600 120,400 Prepaid expenses 18,900 15,400 Total current assets $266,000 $267,400 Current liabilities Accrued expenses payable $10,500 $3,500 Accounts payable 59,500 64,400 Total current liabilities $70,000 $67,900 Prepare the operating activities section of the company's statement of cash flows for the year ended December 31, 2025, using the indirect method. (Show amounts that decrease cash flow with either a-sign eg.-15,000 or in parenthesis e.g. (15,000).) KINGBIRD INC. Statement of Cash Flows (Partial) - Indirect Method For the Year Ended December 31, 2025 Cash Flows from Operating Activities Net Income Adjustments to reconcile net income to Depreciation Expense 18900 6300 Decrease In Accounts Receivable…arrow_forwardWrong answer will get unhelpful ratearrow_forward

- Metlock Lawn Service Company reported a net loss of $15300 for the year ended December 31, 2025. During the year, accounts receivable decreased $25000, inventory increased $20000, accounts payable increased by $30600, and depreciation expense of $26400 was recorded. During 2025, operating activities provided net cash of $77000 O provided net cash of $46700. O used net cash of $46700. ○ used net cash of $9200.arrow_forwardPlease help me solve this financial accounting question using the right financial principles.arrow_forwardDon't use aiarrow_forward

- General accounting Problemarrow_forwardA company purchased for cash a machine with a list price of $85,000. The machine was shipped FOB shipping point at a cost of $6,500. Installation and test runs of the machine cost $4,500. The recorded acquisition cost of the machine is which amount? Need helparrow_forwardJersey Manufacturing applies manufacturing overhead to its cost objects based on 80% of direct material cost. If Job 22B had $64,000 of manufacturing overhead applied to it during June, what was the amount for direct materials assigned to Job 22B? Answerarrow_forward

- Net income is $145,000, accounts payable increased $12,000 during the year, inventory decreased $8,000, and accounts receivable increased $15,000 during the year. Under the indirect method, what is net cash provided by operations?arrow_forwardHelparrow_forwardThe following data is available for Ivanhoe Corporation at December 31, 2025: Common stock, par $10 (authorized 32500 shares) $292500 Treasury stock (at cost $15 per share) $1110 Based on the data, how many shares of common stock are outstanding? 32500 32426 29250 ○ 29176arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education